TL;DR summary:

- Proof of insurance confirms an active policy and must include specific details to prevent delays during mortgage closing in Texas. It involves accurate documentation such as certificates or declarations pages, with correct lender and property information to ensure compliance and smooth claims processing. Proactively maintaining current, precise insurance proof helps Texas homeowners and businesses avoid stress, reduce costs, and build a strong risk management foundation.

You’re three days from closing on your Lubbock home, and your lender emails you to say your proof of insurance is incomplete. The mortgagee clause lists the wrong lender name. Closing is postponed. This scenario happens more often than most Texas homeowners expect, and it usually comes as a complete shock. Having an active insurance policy is not the same as having proper proof of that policy. Understanding the difference, and what your documentation must actually contain, can save you serious time, money, and stress.

Table of Contents

-

- What is proof of insurance and why does it matter in Texas?

- Key elements required on a Texas proof of insurance document

- How proof of insurance impacts claims and ongoing risk management

- Practical steps for Texas homeowners and entrepreneurs to stay compliant and protected

- Why most Texans misunderstand “proof” — and how you can get ahead

- Stay protected: Next steps for your Texas home or business

Key Takeaways

| Point | Details |

|---|---|

| Definition matters | Proof of insurance isn’t just a policy—it’s essential, lender-verified documentation. |

| Mortgagee clause critical | Accurate mortgagee details on proof documents prevent costly processing and claims delays. |

| Claims depend on proof | Claims adjusters use current proof to verify coverage before approving payouts. |

| Texas-specific compliance | Texas risk management and audits require up-to-date, accurate proof with all required fields. |

| Proactive advantage | Staying ahead with organized proof of insurance smooths loans, claims, and regulatory processes. |

What is proof of insurance and why does it matter in Texas?

Proof of insurance is the official documentation that confirms an active insurance policy exists for a specific property, vehicle, or business. It is not just a receipt. It is a formal record that communicates the nature, scope, and limits of your coverage to third parties such as lenders, regulators, or business partners.

In Texas, this documentation takes several forms. The most common are:

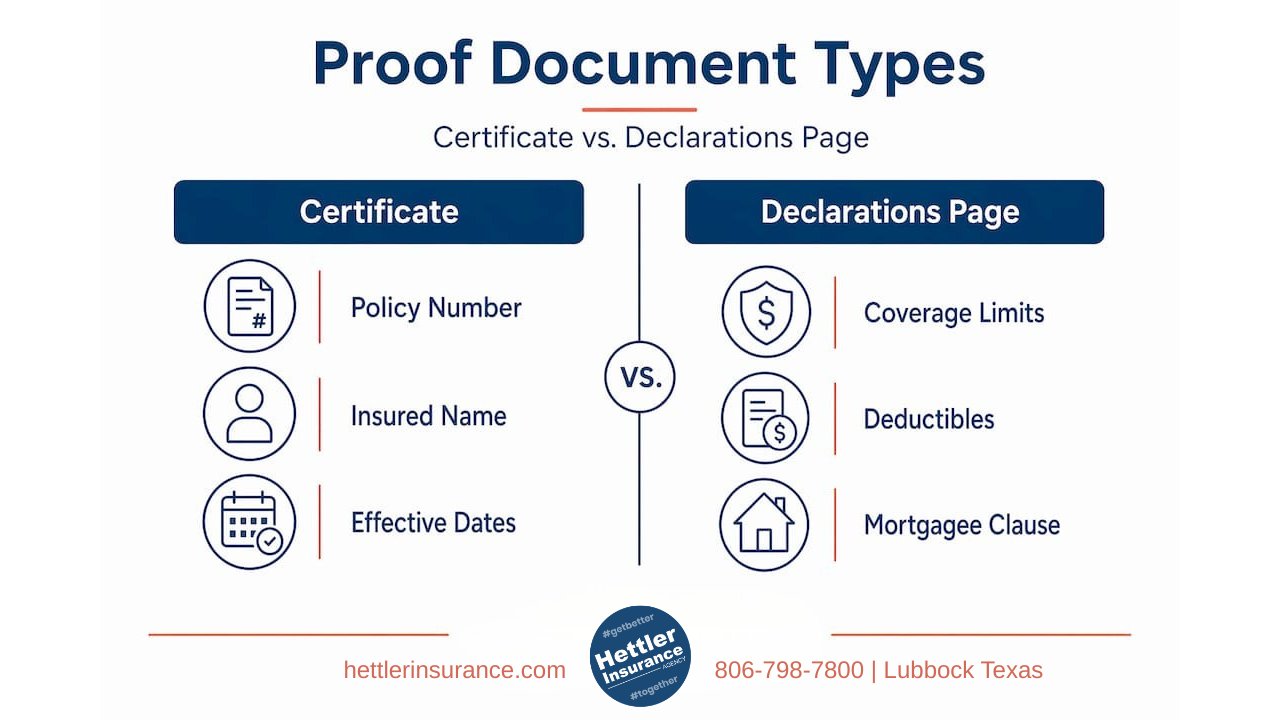

- Certificate of insurance (COI): A summary document that outlines essential policy details. Used frequently in commercial settings and real estate transactions.

- Declarations page (dec page): The first section of your actual policy that lists all key coverage details in one place.

- Digital ID card: Most commonly used for auto insurance. Accepted by Texas law enforcement under Texas Transportation Code but has limited application for mortgage or business compliance.

Texas lenders and mortgage companies require specific documentation before they will process or close on a property loan. According to Fannie Mae guidance on evidence of property insurance, proof is not optional for mortgage processing; a certificate of property insurance is a common option that summarizes the essential details lenders need.

“The certificate of property insurance is widely used because it brings together all the critical details a lender must confirm before releasing loan funds. If even one element is wrong or missing, the process stops.”

Texas-specific situations where proof matters include:

- Mortgage closings: Lenders verify active coverage before funds are released.

- Business contracts: Contractors, vendors, and property managers often require certificates of insurance before any work begins.

- Regulatory compliance: Certain Texas industries, including construction, real estate, and health services, face specific documentation requirements tied to licensing or operational approval.

Understanding your home insurance coverage needs is foundational before you ever generate a proof document. If the coverage itself is inadequate, no amount of clean documentation will protect you when a claim is filed.

For Texas homeowners, especially those navigating their first mortgage or selling a home in West Texas, reviewing homeowners insurance advice specific to your region is a valuable first step before requesting any proof documentation from your carrier.

Key elements required on a Texas proof of insurance document

Understanding the definition is just the start. Here is exactly what your insurance proof document must include to satisfy mortgage lenders or regulators in Texas.

A certificate of property insurance must contain specific fields. Missing or incorrect entries are the most common reason for processing delays. According to the Fannie Mae guidance on evidence of property insurance, getting the mortgagee clause wording correct prevents processing delays and should match your lender’s exact requirements.

Required fields for a valid Texas proof of insurance document:

-

- Policy number: Your unique identifier tied to the insured property or business.

- Named insured: The legal name of the property owner or business entity. Must match exactly what is on the mortgage or contract.

- Property address: The insured property’s street address, including city, state, and ZIP code.

- Coverage types and amounts: This includes dwelling coverage, liability limits, and any endorsements (additional coverage riders) that apply.

- Policy effective dates: The start and end dates of coverage. Lenders confirm that the policy is active through at least the first year of the loan.

- Mortgagee clause: The lender’s full legal name, address, and ISAOA/ATIMA designation (which means “Its Successors and/or Assigns as Their Interests May Appear,” protecting the lender’s interest in the property).

- Insurer’s name and NAIC number: Confirms the carrier is a licensed and recognized insurer.

Comparing certificate of insurance vs. declarations page

| Feature | Certificate of insurance | Declarations page |

|---|---|---|

| Length | One page summary | Multi-page policy section |

| Purpose | Third-party proof | Full policy overview |

| Accepted for mortgage | Yes, commonly | Yes, also accepted |

| Updated with endorsements | May require re-issue | Automatically reflects changes |

| Fastest to obtain | Yes | Depends on carrier |

.

Common mistakes that cause delays:

- Incorrect or abbreviated lender name in the mortgagee clause.

- Wrong property address (especially common after recent moves or newly built homes).

- Missing coverage amounts or policy limits.

- Expired policy dates that were not renewed before submission.

- Coverage listed without required endorsements, such as hail or flood riders.

Pro Tip: Always ask your lender for their exact mortgagee clause language in writing before you contact your insurer. Copy and paste that language into your request so there is zero room for error. This one step prevents the most common closing delays we see in West Texas transactions.

Review what types of mortgage insurance apply to your situation, because lenders may require specific coverage types in addition to standard homeowners protection. If you are also carrying a vehicle loan or any secondary financing, understanding gap insurance basics helps complete the picture of your total insurance documentation obligations.

How proof of insurance impacts claims and ongoing risk management

Once you know what should be on your proof of insurance, the next concern is how it can make or break the claims process and your ability to manage risk as a Texas policyholder.

When a claim occurs, whether from a hailstorm, fire, or liability incident, the first thing a claims adjuster does is verify current, valid proof of coverage. They are checking that the documentation on file matches the actual policy, the property description, and the limits in effect at the time of the loss.

According to Texas TDI guidance on homeowners coverage, insurance documentation connects to actual coverage and limits, not just to the existence of a policy. This distinction is critical. You may have paid your premium on time, but if your proof document does not reflect recent changes to your coverage, your claim can be delayed or reduced.

“A claim filed on an outdated or incorrectly documented policy forces adjusters to start from scratch verifying what coverage was actually in effect. That costs you time and can cost you money.”

What happens during a Texas insurance claim

- Incident occurs: A storm, fire, theft, or liability event triggers the claim process.

- Claim is filed: You contact your insurer and provide initial documentation, including your proof of coverage.

- Adjuster is assigned: The adjuster reviews your proof document against the actual policy terms.

- Property or loss is assessed: A field inspection or documentation review confirms the nature and extent of the loss.

- Coverage is confirmed: The adjuster verifies that the documented perils (the events covered by your policy) include the type of loss you experienced.

- Settlement is calculated: Payment is based on documented coverage limits and deductibles, not on what you assumed you had.

- Claim is resolved or disputed: If documentation gaps exist, the resolution process stalls.

Texas claim documentation: key coverage benchmarks

| Coverage type | Minimum recommended | What proof must show |

|---|---|---|

| Dwelling coverage | Replacement cost value | Coverage amount and basis |

| Personal property | 50-70% of dwelling value | Listed sublimits, if any |

| Liability | $100,000 minimum | Per occurrence limit |

| Wind and hail | Separate deductible common | Deductible percentage |

| Flood | Separate policy needed | Separate dec page |

.

Review your documentation related to insurance claims and deductibles so you understand how documented deductibles affect your actual payout. For business owners, understanding auto liability limits is equally important because commercial vehicle policies must be properly documented before a claim is accepted.

Pro Tip: Store both a digital copy and a printed copy of your current declarations page in an accessible location, such as a secure cloud folder and a physical file in your home or office. Review your coverage limits every year, especially after renovations, business growth, or major purchases.

Practical steps for Texas homeowners and entrepreneurs to stay compliant and protected

Armed with this understanding, here are the key moves you can make as a Texas property owner or business to avoid headaches and stay ahead of your documentation requirements.

According to Texas insurance regulatory standards, regulatory claims processes in Texas rely on current proof of insurance to validate covered perils and limits. Keeping your documentation current is not a one-time task. It is an ongoing responsibility.

Step-by-step system for staying compliant:

- Request proof immediately after binding coverage. When your policy goes into effect, ask your agent for both the declarations page and a certificate of insurance the same day. Do not wait for closing or a contract deadline.

- Verify every field against your current policy. Check the named insured, property address, coverage amounts, and mortgagee clause before submitting any documentation to a third party.

- Store documentation in multiple locations. Use a secure cloud storage folder (such as Google Drive or iCloud), your email inbox, and a physical file. Label files by year and policy type for fast retrieval.

- Update proof documentation after any policy change. If you add an endorsement, change coverage limits, or renew with a different carrier, request a new declarations page and certificate immediately.

- Conduct an annual review every year before renewal. Schedule a 30-minute review with your insurance agent each year to verify that your coverage still matches your current property value, business operations, and any new assets.

- Check for errors before submitting to a lender or regulator. Use a simple checklist: correct legal name, exact property address, accurate coverage amounts, current effective dates, and precise mortgagee language.

- Request updates in writing. When you ask your insurer to update documentation, do so via email so you have a time-stamped record of the request. Follow up within 24 hours if you do not receive a response.

For Texas-specific guidance on what your home policy should cover in practice, revisit the insurance tips for Texas homes that apply to your specific region. West Texas homeowners face unique risks from hail, wind, and dust storms that must be accurately reflected in your policy and your proof documents.

Small business owners in Midland, Odessa, Lubbock, and the surrounding areas should treat their certificate of insurance as a living document. When your business grows, your coverage and documentation should grow with it.

Why most Texans misunderstand “proof” — and how you can get ahead

Most Texas homeowners and business owners treat proof of insurance as a last-minute checkbox. Someone asks for it, you scramble to find it, you send whatever PDF is in your email, and you hope it works. That reactive approach is the primary reason closings stall, claims get delayed, and businesses fail audits.

Here is the perspective most insurance conversations miss: proof of insurance is not just paperwork. It is evidence of your financial position. When you walk into a mortgage closing with a perfectly documented, lender-verified certificate of insurance already in hand, you project competence. When you submit a clean, current certificate to a general contractor as a subcontractor, you win bids. When your claims documentation is accurate and accessible the moment a loss happens, your adjuster has no reason to slow down.

The Texans who use proof of insurance most strategically treat it the same way they treat their business financial statements. They keep it updated. They review it proactively. They know exactly what it says before anyone else asks.

There is also a negotiating dimension that very few policyholders consider. When you can demonstrate to a carrier that your documentation is always in order and your claims history is clean, you are a lower-risk client. That translates, over time, into better pricing and more responsive service relationships. An independent insurance agent who knows your history and your documentation can advocate for you in ways that a direct carrier portal simply cannot.

The real advantage belongs to the proactive policyholder who treats insurance adequacy in Texas as an ongoing strategy, not a one-time decision. Build the habit now. Review your documentation annually. Know what your proof says before your lender, your contractor, or your adjuster has to ask.

Stay protected: Next steps for your Texas home or business

If this article has surfaced gaps in your current documentation or coverage, now is the right time to act. Waiting until a lender flags an error or a claim is filed is always the more expensive approach.

At Hettler Insurance Agency, we have been helping Texas homeowners and small business owners navigate exactly these documentation requirements since 1992. As an independent agency with access to over 30 top-rated carriers, we do not just sell policies. We help you build and maintain the documentation that makes those policies work when you need them most. Whether you are buying your first home in Lubbock, managing a growing business in Midland, or just trying to get your coverage organized, our team is ready to help. Explore the insurance minimums for Texas entrepreneurs that apply to your business, and contact us to schedule a no-pressure review. Get Hettler, Get Better.

Frequently asked questions

What documents qualify as proof of insurance for a mortgage in Texas?

A certificate of property insurance or the declarations page are both acceptable; they must include the policy number, coverage amounts, effective dates, property address, and mortgagee information exactly as your lender requires.

Why is the mortgagee clause wording so important on Texas insurance documents?

Correct mortgagee wording ensures the lender is properly listed as an interested party, and getting that wording precise prevents loan or claims delays caused by mismatched legal names or missing ISAOA/ATIMA language.

How does proof of insurance affect a Texas insurance claim?

Claims adjusters use your proof document to confirm that current coverage, property identification, and policy limits are in place, because proof connects to actual coverage and documented limits, not just to the existence of a policy.

What happens if my Texas proof of insurance is expired or incomplete during an audit?

If your proof is outdated, Texas regulatory processes allow your lender or agency to issue immediate update demands and suspend your compliance status until the correct documentation is on file.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: What documents qualify as proof of insurance for a mortgage in Texas?

Q2 ?: Why is the mortgagee clause wording so important on Texas insurance documents?

Q3 ?: How does proof of insurance affect a Texas insurance claim?

Q4 ?: What happens if my Texas proof of insurance is expired or incomplete during an audit?

Q5 ?: How often should I update or review my proof of insurance in Texas?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com