TL;DR summary:

- Texas homeowners face rising insurance premiums due to severe weather and inflation, making insurance a vital part of financial planning. Proper coverage should focus on risk transfer, liquidity, and matching deductibles to emergency savings to prevent financial setbacks. Building a sequence of emergency funds, insurance policies, and investments creates a resilient financial foundation that protects against catastrophic losses.

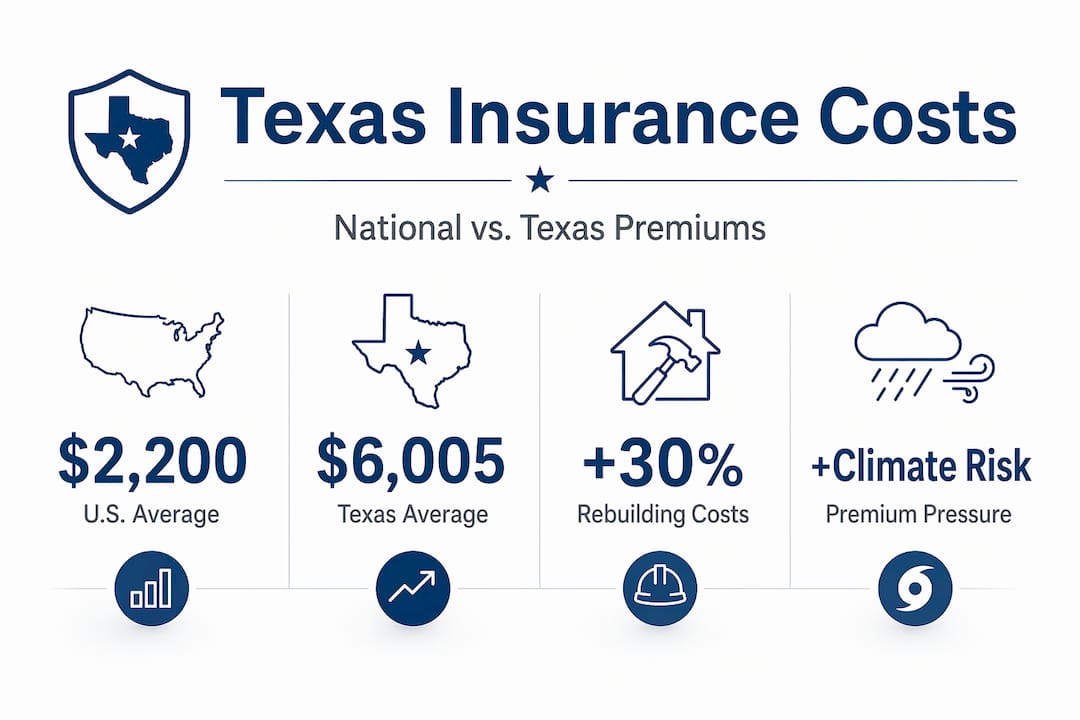

Picture this: a young couple in Lubbock closes on their first home in March. By June, a hail storm rips through West Texas, punching holes in the roof and flooding the garage. The repair estimate comes in at $18,000. Their insurance policy has a $5,000 wind and hail deductible — money they haven’t budgeted for because they assumed insurance “takes care of everything.” Now they’re choosing between a high-interest personal loan and draining the savings account they were building for their kids. That scenario isn’t rare. Texas premiums climbed nearly 19% in 2024, with average annual rates reaching $6,005, and weather events are hitting harder and more often. If you’re a Texas homeowner between 28 and 42, integrating insurance into your financial plan isn’t optional anymore — it’s the foundation everything else stands on.

Table of Contents

- Why insurance belongs at the core of your financial plan

- The right order: Sequencing insurance and emergency funds for stability

- Texas premium pressure: How weather risk shapes your insurance costs

- Deductibles, limits, and the risks most people underestimate

- What most Texas families get wrong about insurance and financial security

- Take the next step toward financial security

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Insurance prevents financial ruin | It safeguards your finances from large, unpredictable expenses that could otherwise destroy your budget. |

| Sequence matters | Tackle emergency funds and key insurance policies before prioritizing investments. |

| Texas premiums are rising | Extreme weather and market changes mean higher costs and bigger planning challenges for Texas homeowners. |

| Plan for out-of-pocket costs | Keep enough emergency cash to handle insurance deductibles and required repairs without adding debt. |

Why insurance belongs at the core of your financial plan

Insurance gets misunderstood more than almost any other personal finance topic. People either treat it as a reluctant monthly bill or assume it functions like a savings account that pays out when things go wrong. Neither view is accurate, and both lead to costly decisions.

The clearest way to think about it: insurance functions as a risk-financing tool. You pay premiums to transfer low-probability, high-cost losses to an insurer — not as an investment, and Not as a substitute for savings. It’s a financial shield, not a piggy bank.

What that means in practice is important. Insurance doesn’t grow your wealth. It protects the wealth you’re building. When a tornado takes your roof, or a kitchen fire destroys your cabinets and appliances, the repair bill isn’t a predictable expense you saved up for — it’s a sudden, massive financial disruption. That’s exactly the kind of loss insurance for catastrophic risks is designed to absorb.

For Texas homeowners specifically, this risk calculus is changing. Severe weather events — hail, flooding, high winds, winter freezes — are no longer outliers. They’re showing up on a near-annual basis in many parts of the state. Climate risk and insurance in Texas are now tightly linked, meaning the financial stakes of being underinsured or uninsured are higher than they were even five years ago.

Key reasons insurance belongs in the financial core of your plan:

- It absorbs low-probability, high-severity events that savings alone cannot realistically cover

- It keeps your investment and retirement contributions intact when disasters strike, because you don’t have to liquidate accounts to pay for repairs

- It protects income continuity through disability and life policies when the earner in your household can’t work

- It stabilizes your mortgage situation by ensuring a covered loss doesn’t lead to a property that can’t be repaired or sold

Without this foundation in place, every other piece of your financial plan — the 401(k), the college savings fund, the emergency reserve — becomes vulnerable to a single bad weather event.

The right order: Sequencing insurance and emergency funds for stability

Knowing that insurance matters is one thing. Knowing where it fits in your overall financial sequence is what actually changes outcomes. A lot of young Texas families do things out of order — they invest first, insure later, and then discover the hard way that one hailstorm can set them back years.

Here’s a practical, proven sequence that works for Texas households:

- Build a baseline emergency fund. Start with $1,000 as your immediate buffer. This isn’t a long-term solution, but it prevents you from going into debt over a minor car repair or appliance replacement. Once you have the basics covered, build toward one to three months of essential expenses.

- Establish a working budget. Know your actual monthly income, fixed expenses, and discretionary spending before you commit to premium payments. Insurance premiums that strain your budget lead to dropped coverage at exactly the wrong moment.

- Prioritize “protect what you have.” Before you invest aggressively, lock in smart insurance policy types: health, life, disability, homeowners or renters, and auto. The Consumer Financial Protection Bureau recommends this sequence — establish a budget and baseline emergency fund first, then prioritize key policies to prevent financial derailment from major risks.

- Expand your emergency fund to 3 to 6 months. Once your core policies are in place, grow your reserve to handle a deductible, a job gap, or a major unexpected expense.

- Then invest for growth. With your foundation intact, contributions to retirement accounts and other investments are protected by the safety net underneath them.

Pro Tip: The biggest mistake families make is jumping straight to investment step five without completing steps one through four. If a hailstorm hits and you don’t have a homeowners policy or the cash to cover your deductible, that Roth IRA you’ve been growing gets raided instead.

Understanding minimum insurance needs at each life stage also helps you avoid over-insuring in areas that don’t need it while leaving genuine gaps elsewhere. A 30-year-old with two kids and a mortgage has very different priorities than a 29-year-old renting an apartment, even if they earn the same income.

Texas premium pressure: How weather risk shapes your insurance costs

Texas has a weather problem — and it’s becoming an insurance cost problem at the same time. The combination of hail, flooding, high winds, and winter storm events has pushed home insurance rate increases to levels that directly affect how families budget.

Here’s what the numbers look like:

| Factor | National average | Texas average |

|---|---|---|

| Average annual homeowners premium | ~$2,200 | ~$6,005 |

| Premium increase (2022 to 2024) | ~15% | ~40%+ |

| Primary cause | General inflation | Weather claims + repair costs |

| Common deductible type | Flat dollar amount | Percentage of home value |

Texas premiums are increasingly treated as a financial-stability constraint, not just an insurance line item. A family paying $500 per month for homeowners coverage is making a significant budget decision — one that competes with savings, childcare, and debt repayment.

Why are costs this high in Texas specifically? Several forces are stacking on top of each other:

- Weather frequency and severity. Hailstorms that once hit every few years are now annual events in many West Texas zip codes.

- Rebuilding cost inflation. Labor shortages and materials prices have pushed the cost of repairing or rebuilding structures sharply higher since 2020.

- Reinsurance market pressure. The companies that back your insurance carrier have raised their own costs, which gets passed directly to policyholders.

- Population and property value growth. More homes, higher values, and more total insured loss exposure across Texas.

Research from the Levy Institute shows that climate change is accelerating these premium pressures nationally, but Texas sits near the top of the risk exposure curve. Choosing a Texas insurance carrier wisely — one with strong financials and deep Texas market experience — is now a financial planning decision, not just a shopping preference.

The practical implication for your budget: build premium increases into your annual financial review. Don’t assume your $4,800 annual premium stays flat for five years. Budget for 10 to 15% annual adjustments and let a pleasant surprise (no increase) be the exception, not your plan.

Deductibles, limits, and the risks most people underestimate

Premium costs get most of the attention. Deductibles and coverage limits cause most of the real financial pain. This is the gap between what people think insurance does and what it actually pays for.

Every time you file a claim, you pay your deductible first. In Texas, wind and hail deductibles are often structured as a percentage of your home’s insured value — not a flat dollar amount. On a home insured at $350,000 with a 2% hail deductible, you owe $7,000 before the insurer pays a cent. On a 3% deductible, that’s $10,500. Do you have that sitting in a savings account right now?

Aligning your emergency fund to your deductible obligation is critical. The biggest planning failure is underestimating out-of-pocket exposure — deductibles, co-insurance, and coverage limits — and assuming insurance alone prevents financial hardship. Insurers and financial advisors consistently emphasize aligning your policy choices with your emergency fund so you can pay required outlays without taking on new high-interest debt.

A practical approach: treat deductibles as part of your emergency cash requirement, not as something insurance will cover automatically. If your highest possible deductible exposure is $8,000, your emergency fund target should account for that $8,000 as a realistic near-term cash need.

| Home insured value | 1% hail deductible | 2% hail deductible | 3% hail deductible |

|---|---|---|---|

| $250,000 | $2,500 | $5,000 | $7,500 |

| $350,000 | $3,500 | $7,000 | $10,500 |

| $450,000 | $4,500 | $9,000 | $13,500 |

Coverage limits carry equal risk. If your home’s rebuilding cost has risen 30% since you bought your policy but you haven’t updated your dwelling coverage limit, you could be significantly underinsured after a total loss. The insurer pays up to your policy limit — not what it actually costs to rebuild.

Pro Tip: Ask your agent to run a replacement cost estimator on your home every two to three years. Rebuilding costs in West Texas have shifted sharply since 2020, and a policy that was adequate in 2021 may leave you $60,000 short today if you have to rebuild from scratch. Managing insurance deductibles proactively — by matching them to your savings capacity — is one of the smartest financial moves you can make.

What most Texas families get wrong about insurance and financial security

After more than 30 years of working with Texas homeowners, we’ve seen the same mistake repeated more than any other: families focus almost entirely on the premium and almost never on liquidity. They shop hard to save $200 a year on their homeowners policy by taking a higher deductible, but they don’t increase their emergency fund to match. Then a hailstorm hits and the deductible they chose to save money becomes a $9,000 bill they have no plan to pay.

Over-insuring creates its own problem. Paying for coverage levels you don’t need — like replacement value policies on older vehicles you’d replace anyway, or high-limit umbrella policies before you’ve finished your emergency fund — drains the cash you actually need in the near term. Balance matters.

The families who navigate Texas weather events with the least financial disruption share one trait: they treat liquidity as a first-class component of their insurance strategy. They know their deductibles. They know what a major claim would require out-of-pocket. And they keep that cash accessible, not tied up in long-term investments.

Navigating rising homeowner premiums isn’t just about finding the cheapest carrier. It’s about building a financial structure where a storm doesn’t become a crisis. Smart coverage paired with adequate cash reserves is the combination that actually works — not perfect coverage alone, and certainly not an emergency fund without adequate insurance underneath it.

The honest truth is that no policy eliminates risk. It transfers the catastrophic part. Your financial plan has to handle everything else.

Take the next step toward financial security

If this article has clarified how insurance fits into your overall financial picture, the next step is making sure your actual policies reflect that clarity. Many Texas families are either over-covered in areas that don’t move the needle or dangerously underinsured against the risks that could genuinely derail their finances.

At Hettler Insurance Agency in Lubbock, Texas, we’ve been helping homeowners like you build a coverage foundation since 1992. As an independent agency, we represent over 30 top-rated carriers — which means we shop and compare options across the market to find the right fit for your home, your family, and your budget. No pressure, no single-carrier limitations. Just honest guidance from a family-owned team with CIC-credentialed advisors who know Texas risk inside and out. Start by reviewing your minimum insurance needs — then call us to put a real plan together. Get Hettler, Get Better.

Frequently asked questions

What types of insurance should young Texas families prioritize?

Focus on homeowners, health, life, auto, and disability coverage as your core protections. The CFPB recommends establishing an emergency fund first, then securing these key policies before moving on to investment goals.

How large should my emergency fund be, given Texas’s high deductibles?

Aim for enough to cover at least your largest deductible obligation, with a long-term target of three to six months of expenses. Treating deductibles as a required cash reserve — not something the insurer absorbs — protects you from debt after a claim.

Why are insurance premiums in Texas rising so fast?

More frequent severe weather events, sharply higher repair and labor costs, and statewide reinsurance market pressure are all compounding at once. Texas premiums have risen substantially even for homeowners who have never filed a claim.

Do I need to review my insurance policies every year?

Yes, and in Texas, annual reviews are especially important because rebuilding costs, risk exposure, and premium rates shift significantly year over year. Schwab emphasizes maintaining proper coverage alongside emergency reserves as the foundation of sound financial planning.

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: What types of insurance should young Texas families prioritize?

Q2 ?: How large should my emergency fund be, given Texas’s high deductibles?

Q3 ?: Why are insurance premiums in Texas rising so fast?

Q4 ?: Do I need to review my insurance policies every year?

Q5 ?: What’s the biggest mistake Texas families make with insurance?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com