TL;DR summary:

- Texas homeowners often face under-insurance, risking inadequate protection during severe weather events.

- Licensed agents personalize coverage by assessing regional risks, policy gaps, and recommending appropriate adjustments.

- Agents assist with claims and disaster response, ensuring proper documentation and advocating for fair settlements.

Most Texas homeowners assume that buying a policy online is enough to protect their families. It is not. Under-insurance is prevalent among vulnerable households across Texas, and rising premiums make the stakes even higher for young families and first-time buyers. Insurance agents are often misunderstood as salespeople pushing products. In reality, a licensed agent bridges the gap between confusing policy language and real-world protection tailored to your home, your neighborhood, and the specific weather risks Texas throws at you every single year. This guide explains what agents actually do, how they personalize your coverage, and why their role matters most when disaster strikes.

Table of Contents

- Key Takeaways

- What insurance agents actually do for Texas homeowners

- Personalizing coverage: Avoiding under-insurance and addressing weather risks

- Navigating premiums, discounts, and affordability in Texas

- Agents’ role in filing claims and disaster response

- A fresh perspective: Why Texas insurance agents are more than policy sellers

- Discover tailored insurance solutions for your Texas home

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

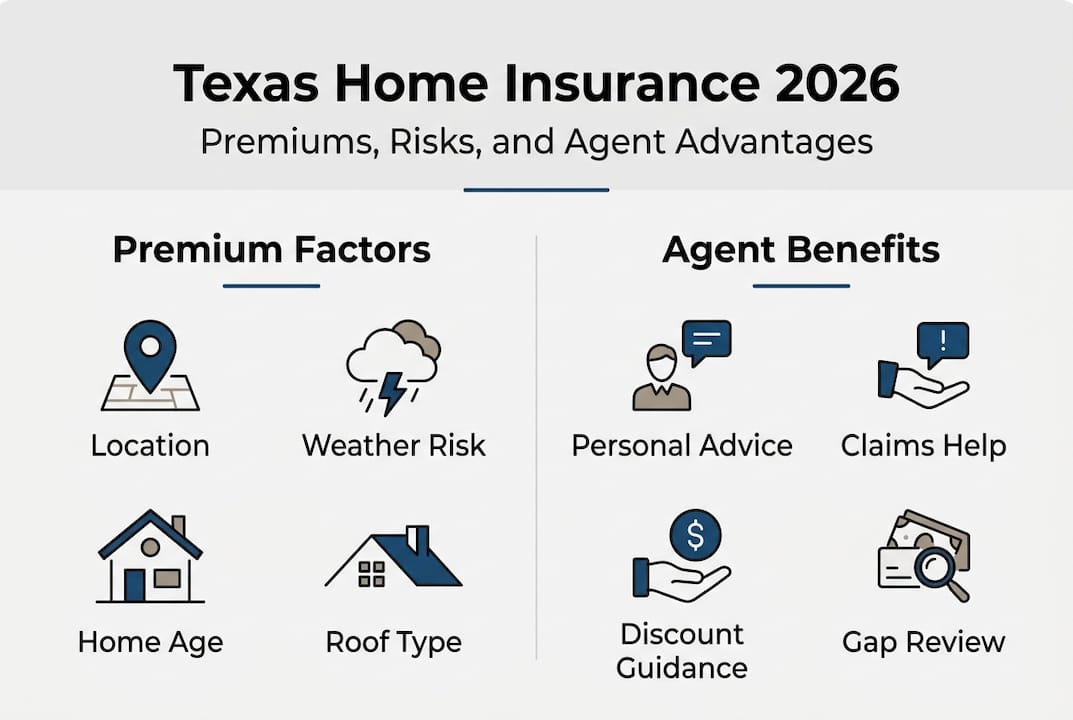

| Personalized advice | Insurance agents tailor coverage for Texas-specific risks such as wind, hail, and flood. |

| Prevent under-insurance | Working with an agent helps avoid common coverage gaps and costly shortfalls. |

| Premium optimization | Agents leverage discounts and smart bundling to help make coverage affordable for families. |

| Claims support | Agents guide homeowners through claims and disaster recovery for a smoother process. |

| Client advocacy | Texas agents legally represent the client’s interests, ensuring better protection and outcomes. |

What insurance agents actually do for Texas homeowners

Let’s be direct: an insurance agent is not just someone who hands you a quote and collects a commission. A licensed agent advises on policy coverages and helps you select options designed around Texas-specific risks like wind, hail, and flood. That is a very different service than what an online comparison tool offers.

In Texas, the weather is not predictable. Lubbock gets hail. The Gulf Coast gets hurricanes. The Hill Country floods. North Texas deals with tornadoes. Your agent’s first job is to understand exactly where you live and what risks your home faces before recommending a single policy.

Here is what a qualified agent does for you:

-

-

- Assesses your home’s physical risks, including roof age, construction type, and proximity to flood zones or coastal areas

- Reviews your replacement cost, which is the amount it would cost to rebuild your home from scratch, not just its market value

- Identifies coverage gaps in standard policies that could leave you exposed after a major weather event

- Explains exclusions in plain language so you are not surprised when you file a claim

- Shops multiple carriers to find the best fit for your budget and risk profile

- Acts as your advocate, not the insurer’s representative

-

Agents must be licensed by TDI (Texas Department of Insurance) and are legally required to represent your interests, not the insurance company’s bottom line. That legal duty matters enormously when you are negotiating a claim after a hailstorm damages your roof.

When choosing a Texas carrier, your agent compares financial strength ratings, claims handling reputation, and pricing across multiple companies. An independent agent, in particular, has access to dozens of carriers and is not locked into pushing one company’s products.

Pro Tip: Ask your agent to review your replacement cost estimate and identify any coverage gaps before you renew your policy each year. Costs to rebuild have risen sharply due to inflation, and your coverage limit may no longer be sufficient.

Agents also help with coverage beyond the home itself. If you are exploring Texas life insurance options to protect your family’s financial future, a good agent can bundle and coordinate those policies efficiently.

Personalizing coverage: Avoiding under-insurance and addressing weather risks

Understanding the duties is important, but personalizing coverage is where agents dramatically impact your protection and peace of mind.

A generic, out-of-the-box policy rarely fits a Texas home well. Agents bridge the complexity of Texas weather risks by personalizing coverage and helping homeowners avoid under-insurance. That means your agent looks at your specific location, roof condition, flood risk, and wind exposure before recommending deductibles and coverage limits.

Here is a clear comparison of what you get with and without an agent:

| Coverage factor | Generic online policy | Agent-customized policy |

|---|---|---|

| Replacement cost accuracy | Based on general estimates | Reviewed against local rebuild costs |

| Wind and hail deductible | Standard percentage | Adjusted to your risk zone |

| Flood coverage | Usually excluded | NFIP or private flood added if needed |

| TWIA eligibility (coastal) | Not assessed | Verified and applied |

| Coverage gaps | Often undetected | Identified and addressed |

.

Two programs are especially important for Texas homeowners in specific regions. The TWIA (Texas Windstorm Insurance Association) provides windstorm and hail coverage for properties in designated coastal counties. Coastal homes need TWIA inspection and certification before coverage is issued. Your agent handles that process and makes sure your home qualifies.

The NFIP (National Flood Insurance Program) covers flood damage that standard homeowners policies exclude. Many homeowners outside designated flood zones skip this coverage, but that is a costly mistake. Floods happen in low-risk areas too, and the financial damage from even a few inches of water inside your home can be devastating.

Key factors your agent will review when personalizing your policy:

-

-

- Roof age and material, which directly affects your eligibility and premium

- Wind and hail deductible percentage, which is often separate from your standard deductible in Texas

- Actual cash value vs. replacement cost for your personal property and structure

- Additional living expense coverage, which pays for temporary housing if your home becomes uninhabitable

-

Understanding replacement cost coverage is one of the most important steps you can take as a homeowner. It ensures your payout reflects what it actually costs to rebuild, not a depreciated value.

Pro Tip: Even if you are not in a designated flood zone, ask your agent about flood coverage. Non-flood-zone properties account for a significant share of flood claims in Texas every year.

Reviewing these details before you buy is critical. The insurance prep tips at Hettler’s site walk you through exactly what to gather before your first agent consultation.

Navigating premiums, discounts, and affordability in Texas

Once your coverage is tailored for weather risks, it is time to tackle the affordability and premium optimization.

Texas premiums average $1,200 to $5,000 per year, with agents helping optimize costs through discounts and bundling. That is a wide range, and where your premium lands depends on several key factors.

What drives your Texas home insurance premium:

| Factor | Impact on premium |

|---|---|

| Location and weather risk zone | High in coastal and hail-prone areas |

| Roof age and condition | Older roofs increase costs significantly |

| Home construction type | Brick typically costs less than wood frame |

| Credit score | Better credit often means lower premiums |

| Deductible amount | Higher deductible lowers your premium |

| Claims history | Prior claims raise your rate |

.

Under-insurance is prevalent among vulnerable households, and rising premiums driven by claims frequency and inflation are pushing more families toward inadequate coverage to save money. That trade-off can be catastrophic after a major storm.

Here is how an agent helps you manage costs without sacrificing protection:

-

-

- Bundle your policies. Combining home and auto insurance with the same carrier typically saves 10 to 25 percent on both policies.

- Improve your credit score. Texas insurers use credit-based insurance scores as a rating factor. A better score can meaningfully lower your premium.

- Install protective devices. Smoke detectors, security systems, and impact-resistant roofing can qualify you for discounts.

- Raise your deductible strategically. A higher deductible lowers your annual premium, but only if you can cover that amount out of pocket after a loss.

- Review your policy annually. Your agent checks for new discounts, updated replacement cost values, and coverage changes that affect your rate.

-

Understanding why your policy premium increases year over year helps you make informed decisions rather than just accepting the renewal bill. The TDI consumer guide also outlines your rights as a policyholder when it comes to rate changes.

Surprisingly, the same factors that affect your home insurance can overlap with auto premium factors. Bundling both with one agent gives you a clearer picture of your total insurance spend and more leverage when negotiating rates.

Agents’ role in filing claims and disaster response

Even with the best policy and pricing, when disaster strikes, an agent’s real worth is revealed during claims and recovery.

Filing a claim after a hailstorm, tornado, or flood is stressful. Most homeowners have never done it before. Your agent guides you through every step, from the moment the storm passes to the final settlement check.

Here is what to do immediately after a weather event damages your home:

-

-

- Document everything. Take photos and videos of all damage before any cleanup or repairs begin.

- Prevent further damage. Cover broken windows or roof openings with tarps. Insurers call this mitigation, and failing to do it can reduce your claim payout.

- Report your claim immediately. Claims must be reported immediately to your insurer for the best outcome and prompt recovery.

- Keep all receipts. Any emergency repairs or temporary housing costs should be documented for reimbursement.

- Coordinate with your adjuster. Your agent helps you prepare for the adjuster’s visit and ensures your damage is fully documented.

-

For coastal homeowners with windstorm coverage through TWIA, the claims process has additional steps. Your agent knows those steps and prevents costly delays.

One option homeowners sometimes consider is hiring a public adjuster, which is an independent professional who represents you during the claims process. They can be helpful in complex or large claims, but they charge fees of up to 10 percent of your settlement. Your licensed agent can advise you on whether a public adjuster is worth it for your specific situation.

“Report damage to your insurance company as soon as possible. Delays can complicate your claim and reduce your recovery.” — TexasLawHelp Disaster Manual

Understanding how climate change affects insurance in Texas is also becoming more relevant. Severe weather events are increasing in frequency, which is why having an agent who stays current on carrier changes and coverage updates is more valuable than ever.

A fresh perspective: Why Texas insurance agents are more than policy sellers

Conventional wisdom treats insurance agents as salespeople. That view misses the real value they provide, especially for young homeowners who are buying their first home and have no frame of reference for what good coverage looks like.

At Hettler Insurance Agency, we have seen what happens when families skip the agent and buy online. They end up with wrong deductibles, missing flood coverage, and replacement cost limits that have not kept pace with inflation. When a hailstorm hits, they find out the hard way.

The consultative role of an agent is what prevents those costly mistakes. Agents demystify Texas regulations, explain weather-related exclusions in plain language, and make sure your policy actually fits your home and your life. That is not a sales pitch. That is risk management.

When selecting the right carrier, your agent is comparing dozens of options you would never find on your own. That expertise compounds over time as your home, family, and risk profile change.

Pro Tip: Always ask your agent directly whether your policy covers hail and windstorms. In Texas, these are sometimes listed as separate deductibles or excluded entirely from standard policies. Do not assume. Ask.

Discover tailored insurance solutions for your Texas home

You now understand how a licensed agent protects you from under-insurance, weather-related gaps, and costly claims mistakes. The next step is working with an agent who knows Texas inside and out.

At Hettler Insurance Agency, we have served Texas homeowners since 1992 with certified expertise and no-pressure guidance. As an independent agency, we represent over 30 top-rated carriers and shop your coverage at no extra fee. Whether you need minimum coverage guidance or a full policy review, our team is ready to help. Visit Hettler Insurance to get started or call us today for a personalized consultation. Get Hettler, Get Better.

Frequently asked questions

What does an insurance agent do that an online quote can’t?

A licensed agent personalizes your coverage, accounts for Texas-specific risks, advises on discounts, and helps you file claims. Online quotes generate numbers but cannot assess your actual risk or advocate for you.

Do Texas agents need special licenses for windstorm or flood coverage?

Yes. Agents must be licensed by TDI and follow TWIA and NFIP guidelines to write windstorm and flood insurance in Texas.

What is the average annual premium for Texas homeowners insurance?

Premiums range from $1,200 to $5,000 annually, depending on your location, roof age, construction type, and deductible choices.

How quickly should claims be reported after a weather event?

Report claims immediately after a weather event. Delays can complicate your case and reduce your final settlement.

Can agents help me save on premiums?

Yes. Agents use bundling, credit scoring, and discount optimization strategies to lower your annual premium without cutting critical coverage.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: What does a Texas insurance agent do that an online quote cannot?

Q2 ?: Do Texas agents need special licenses for windstorm or flood coverage?

Q3 ?: What is the average annual premium for Texas homeowners insurance?

Q4 ?: How quickly should I report a claim after a weather event in Texas?

Q5 ?: How can a Texas agent help me save on premiums without losing coverage?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com