TL;DR summary:

- Many Texas homeowners are unaware that their wind and hail deductibles are often percentage-based rather than fixed amounts, leading to unexpectedly high out-of-pocket costs after storms. Regular policy reviews are essential to catch changes in deductibles, coverage limits, and exclusions that can significantly impact claim payouts. Consulting an experienced local agent ensures homeowners understand their policies thoroughly and remain protected before severe weather strikes.

Most Texas homeowners assume their deductible is a single, flat dollar amount. Then a hailstorm rolls through Lubbock or the DFW suburbs, and they discover their wind/hail deductible is actually a percentage of their home’s total insured value, not a fixed number. That difference can mean owing $8,000 or more out of pocket instead of $1,000. North Texas homeowners are being urged to review their policies specifically because coverage varies by location and storm deductibles can change the financial outcome of a claim dramatically. This article will show you exactly why, how, and what to check in your next policy review.

Table of Contents

- Why policy reviews matter for Texas homeowners

- How Texas storm deductibles really work

- Checklist: What to review in your Texas homeowners policy

- How to make insurance policy reviews easy and routine

- The truth most experts won’t tell you about Texas insurance reviews

- Get expert help with your Texas insurance review

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Policy terms matter | Small changes to coverage or deductibles can affect your costs by thousands in a Texas storm. |

| Understand your deductible | In Texas, wind/hail deductibles are often a percentage of your insured value, not a flat fee. |

| Annual reviews are essential | Check your homeowners policy every year, especially before hail season, to catch changes early. |

| Read the first page | Wind/hail coverage details are often right on your policy’s declarations page—don’t skip it. |

| Agent expertise helps | A Texas-based insurance agent can spot confusing terms and highlight exposures tailored to your local risks. |

Why policy reviews matter for Texas homeowners

Texas is not an average insurance market. Lubbock sits in one of the most hail-prone corridors in the United States. DFW suburbs deal with tornado watches, damaging wind events, and hailstorms that can drop baseball-sized hail without much warning. These conditions create a very specific set of insurance risks that do not apply in most other states, and they are exactly why a routine annual policy review is not optional. It is a financial necessity.

Here is the core problem: most homeowners only glance at the renewal notice to see whether the premium went up. They note the new dollar amount, maybe call their agent to ask about the increase, and then file the documents away. But homeowners policy increases are only part of the story. Your carrier may have quietly changed your wind/hail deductible structure, adjusted coverage limits, added exclusions, or modified the terms under which wind and hail claims are processed. These changes rarely come with a phone call or a clear explanation.

“Don’t review only the renewal premium. Review the wind/hail deductible structure and the specific wind/hail coverage terms, because that is where many homeowners’ expectations break at claim time.”

The financial stakes are real. Missing a single policy change can add thousands of dollars to your out-of-pocket costs after a storm. And common homeowner insurance mistakes like skipping the annual review are the ones that tend to cause the biggest surprises at the worst possible time.

What a thorough policy review actually reveals:

- Whether your wind/hail deductible changed from last year

- Whether your insured dwelling value kept pace with rising local construction costs

- Any new endorsements (add-ons or restrictions) your carrier attached to the policy

- Whether your personal property limits are still adequate

- Whether your liability coverage meets today’s standards

- Any exclusions that did not exist in your prior policy year

Many Texas families have no idea these changes happen until they file a claim. Reviewing your policy annually, ideally before peak hail season in the spring, puts that knowledge in your hands before it matters most. Use a Texas homeowner checklist to stay organized and make sure you cover every key section.

How Texas storm deductibles really work

Understanding Texas wind/hail deductibles requires knowing the difference between two types: flat deductibles and percentage-based deductibles.

A flat deductible is a fixed dollar amount. If you have a $1,500 flat deductible and your roof repair costs $9,000, you pay $1,500 and your insurer covers the rest. Simple.

A percentage-based deductible works differently. It is calculated as a percentage of your home’s insured value (also called the dwelling coverage limit), not of the total claim amount. This is the structure many Texas carriers now use specifically for wind and hail damage. Percentage-based deductibles can surprise homeowners who assume they have a manageable flat deductible, only to discover at claim time that their true out-of-pocket exposure is far higher.

| Home insured value | 1% deductible | 2% deductible | 3% deductible |

|---|---|---|---|

| $250,000 | $2,500 | $5,000 | $7,500 |

| $350,000 | $3,500 | $7,000 | $10,500 |

| $400,000 | $4,000 | $8,000 | $12,000 |

| $500,000 | $5,000 | $10,000 | $15,000 |

.

As you can see, the numbers add up fast. A 2% wind/hail deductible on a $400,000 home means you absorb $8,000 before your insurer pays a single dollar. In 2026, the 2% wind/hail deductible has become one of the most common structures carriers use in Texas because severe weather claim costs have climbed sharply in recent years. Many homeowners in Lubbock and DFW suburbs signed policies with a 1% deductible a few years ago and have no idea that their renewal quietly moved to 2%.

That is not a minor detail. That is a $4,000 difference on a $400,000 home. After a bad storm, when you are already dealing with damaged property and disruption to your household, discovering that gap is brutal.

“Texas wind and hail deductibles are often percentage-based and can surprise homeowners who assume a single flat deductible.”

Pro Tip: Do not just look at your deductible percentage. Run the actual dollar calculation using your current insured dwelling value. Write that number down. That is your real storm exposure, and knowing it in advance lets you plan, budget, and ask your agent the right questions.

It is also worth reviewing coverages that tie into storm damage more broadly. If you own a vehicle, windshield coverage is another Texas-specific item worth checking. Hail that damages your roof often damages your car too. And if you have solar panels, make sure you understand solar coverage policy details, as not all standard Texas policies automatically cover solar equipment at full replacement value.

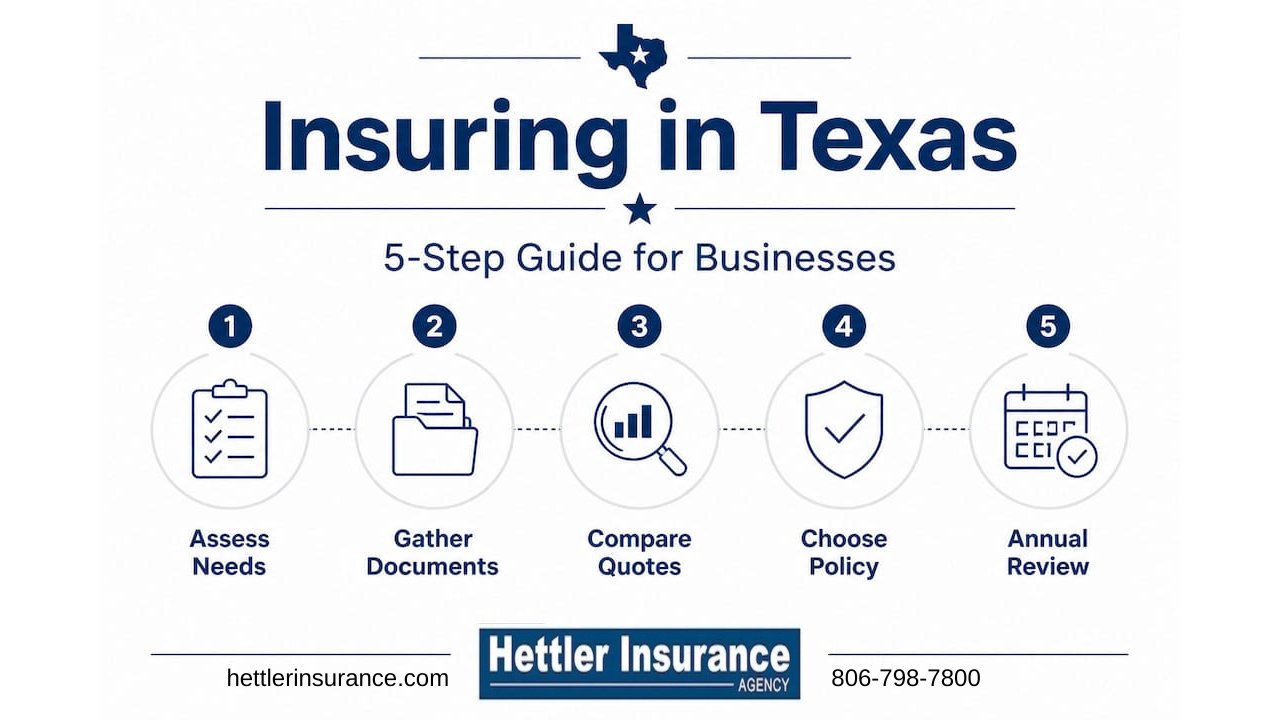

Checklist: What to review in your Texas homeowners policy

A policy review does not need to take hours. But it does need to be systematic. Most homeowners who skip reviews are not lazy. They just do not know exactly where to look or what to look for. Here is a numbered checklist you can work through every year, ideally in February or March before hail season peaks.

- Declarations page. This is the summary page at the front of your policy. It shows your dwelling coverage amount, personal property limits, liability limits, and deductibles. Confirm every number matches what you agreed to and check whether anything changed from the prior year.

- Wind/hail deductible section. Find the specific section that addresses wind and hail separately from your standard deductible. Note whether it is a flat dollar amount or a percentage, and calculate the actual dollar impact against your current insured dwelling value.

- Coverage limits for personal property. Replacement costs for furniture, appliances, clothing, and electronics have risen significantly. Make sure your personal property limit still reflects what it would actually cost to replace your belongings today.

- Liability coverage. Review how much protection you have if someone is injured on your property. Minimum amounts set years ago may no longer be adequate given the cost of medical care and legal fees.

- Endorsements and exclusions. These are additions or restrictions attached to your base policy. New exclusions can appear at renewal. Read every endorsement page, even if it feels tedious.

- Insured dwelling value. Construction costs in Texas have risen sharply. If your insured value is based on outdated cost-per-square-foot estimates, you could be underinsured and receive less than you need to fully rebuild after a total loss.

- Documentation of any changes. If your agent or carrier confirms a change or clarification, get it in writing. A verbal agreement that never makes it into the policy documents is not enforceable.

Pro Tip: Keep a digital copy and a printed copy of your policy’s first page and the most recent endorsement page. Store the digital copy in cloud storage so you can access it from your phone immediately after a storm, even if power is out.

Severe weather drives frequent policy changes in Texas, and deductibles for wind and hail can shift materially from one year to the next. The only reliable way to catch those shifts is to review the documents yourself and ask your agent directly about anything that looks different. When it comes to choosing a Texas carrier, working with an independent agent who represents multiple carriers helps you compare terms, not just prices. A useful contractor security checklist approach applies here too: verify, document, and clarify before you need to use the coverage.

How to make insurance policy reviews easy and routine

Understanding your policy is one thing. Actually carving out time to review it every year is another. Here is how to make it a consistent habit rather than something you put off until the next storm scare.

Build calendar reminders into your year:

- Set a recurring reminder for early March, before the heart of hail season in Texas

- Add a second reminder for when your renewal documents arrive, typically 30 to 45 days before your renewal date

- If you do a spring home maintenance walkthrough, add a policy review to the same day

Bundle your review with home maintenance tasks:

When you walk your property to check gutters, trim trees, and inspect the roof after winter, bring your policy documents with you. Note any new structures, additions, or improvements that might affect your coverage needs. A new deck, a detached garage, or a major kitchen renovation can all change your insured value.

Use a simple tracking system:

A basic spreadsheet works well. Track your premium, dwelling coverage, personal property limit, liability limit, and wind/hail deductible each year in a separate row. When you see a column shift between years, you know exactly what changed and when. There are also apps designed for home inventory and document management that let you attach photos and track policy documents in one place.

Engage your agent for a walkthrough:

Do not try to interpret confusing policy language alone. Ask your agent to walk you through any terms you do not understand. A good local agent knows how Texas weather impacts your insurance costs and can explain exactly why certain deductible structures or exclusions exist in your specific policy. If your property is in an area with elevated wildfire risk, make sure you also address wildfire insurance needs during the same conversation.

Request written clarifications:

If your policy includes special regional coverage terms or endorsements specific to your zip code, ask your carrier or agent to confirm those details in writing. A clarification email or a written policy amendment protects you far better than a phone conversation that was never documented.

Percentage-based deductibles are the single most common source of post-storm financial shock in Texas. Building a routine that keeps you informed ahead of each storm season takes less than an hour per year and can save you thousands.

The truth most experts won’t tell you about Texas insurance reviews

Here is the uncomfortable reality after more than three decades of helping Texas homeowners with their coverage: most people who feel blindsided after a storm did not have the wrong policy. They had a policy they never fully read.

The insurance industry does not hide this information. It is right there in the documents. But it is written in dense language, tucked between pages of conditions and definitions, and most homeowners never open the packet beyond the declarations page. That is understandable. Life is busy. But the consequences of that inaction are not small.

We have sat with families who received far less than they expected after a major hail event because their wind/hail deductible had quietly moved from 1% to 2% at renewal. They never noticed because they only checked the premium. The premium increase was $180 for the year. The deductible change cost them an extra $6,000 at claim time.

That is the trade-off no one talks about loudly enough. Carriers can adjust deductible structures in ways that reduce their exposure and shift costs to you, and they do it within the bounds of your policy documents. They are not doing anything wrong. But if you are not reviewing, you are not aware, and that gap becomes your financial problem the day you file a claim.

The wind/hail coverage terms are where most homeowners’ expectations break at claim time. Not the liability section. Not the personal property limits. The wind/hail section. Review that first.

And if your premium jumped last year, that increase alone is reason to open the full policy and check what else changed. Homeowners policy increases often come paired with deductible adjustments. Finding both at the same time is not a coincidence. A ten-minute review now prevents a $10,000 regret later.

Get expert help with your Texas insurance review

Knowing what to look for is one step. Having an expert in your corner makes the whole process faster and far more reliable.

At Hettler Insurance Agency, we have been helping Texas homeowners understand their policies since 1992. As an independent agency representing over 30 top-rated carriers, we do not just sell you a policy and disappear. We review it with you, explain the wind/hail deductible structure for your specific address, and flag any changes that could catch you off guard at claim time. Ron and Meghan Hettler are both Certified Insurance Counselors (CIC), which means you get expert-level guidance, not a script. Before hail season hits, let us walk you through your current coverage and make sure your minimum insurance requirements and storm protections are exactly where they need to be. No pressure. No obligation. Just clarity.

Frequently asked questions

How often should I review my Texas homeowners policy?

Review your policy at minimum once per year and always before hail season in the spring. Wind/hail deductibles can change annually, so reviewing before storm season is critical.

Where can I find the wind/hail deductible amount in my policy?

Look on the first or declarations page under a section labeled “Wind/Hail Deductibles.” Review the first pages of the policy for these specific coverage terms.

What does a percentage-based deductible mean?

It means your deductible is calculated as a percent of your home’s insured value, not a fixed dollar amount. Wind/hail deductibles in Texas typically range from 1% to 5% of insured value.

Why do insurance policy terms change so often in Texas?

Severe weather drives up costs and claim frequency, which prompts carriers to adjust deductibles and coverage terms frequently to manage their risk exposure.

Can an agent help me review these details?

Yes. A local independent agent who understands Texas-specific weather risks can walk through confusing policy language with you and clarify exactly what your deductibles and storm coverage actually mean.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: How often should I review my Texas homeowners insurance policy?

Q2 ?: Where do I find my wind/hail deductible in my policy?

Q3 ?: What does a percentage-based deductible actually mean?

Q4 ?: Why do Texas insurance policy terms change so often?

Q5 ?: Can an independent agent really help me with a policy review?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com