TL;DR summary:

- Windstorm insurance in Texas is a separate policy essential for coastal homeowners, covering wind and hail damage.

- Many homeowners mistakenly rely solely on standard policies, which often exclude windstorm coverage in high-risk coastal areas.

- Traveling through TWIA or private insurers, homeowners should compare options and ensure comprehensive coverage, including flood policies.

Most Texas homeowners believe their standard homeowners policy has them covered when a hurricane or tornado tears through. That assumption can be a costly mistake, especially if you live near the coast. Windstorm insurance is a separate, specialized policy, and in many parts of Texas it is the only thing standing between your home and a total financial loss after a major storm. This article breaks down exactly how windstorm coverage works in Texas, who needs it, what it costs, and how to make sure you are not paying too much or leaving gaps in your protection.

Table of Contents

- How windstorm insurance works in Texas

- Understanding TWIA: Texas’s windstorm insurer of last resort

- Who needs windstorm coverage and what are the requirements?

- Coverage, costs, and claims: what Texas homeowners can expect

- The smarter way: how homeowners can get better protection and value

- Looking for real savings and the right Texas windstorm policy?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Wind damage isn’t always covered | Standard homeowners insurance may not protect you from wind or hail in much of coastal Texas. |

| TWIA is the backup plan | If private insurers won’t cover you, TWIA provides windstorm coverage as insurer of last resort with specific requirements. |

| Shop for alternatives first | Independent agents can help you find better rates and protection before relying on TWIA. |

| Pair with flood protection | To be fully safe in storm-prone Texas, consider separate flood insurance with your windstorm policy. |

.

How windstorm insurance works in Texas

Now that you know why regular insurance often isn’t enough, let’s look at how windstorm coverage operates specifically in Texas.

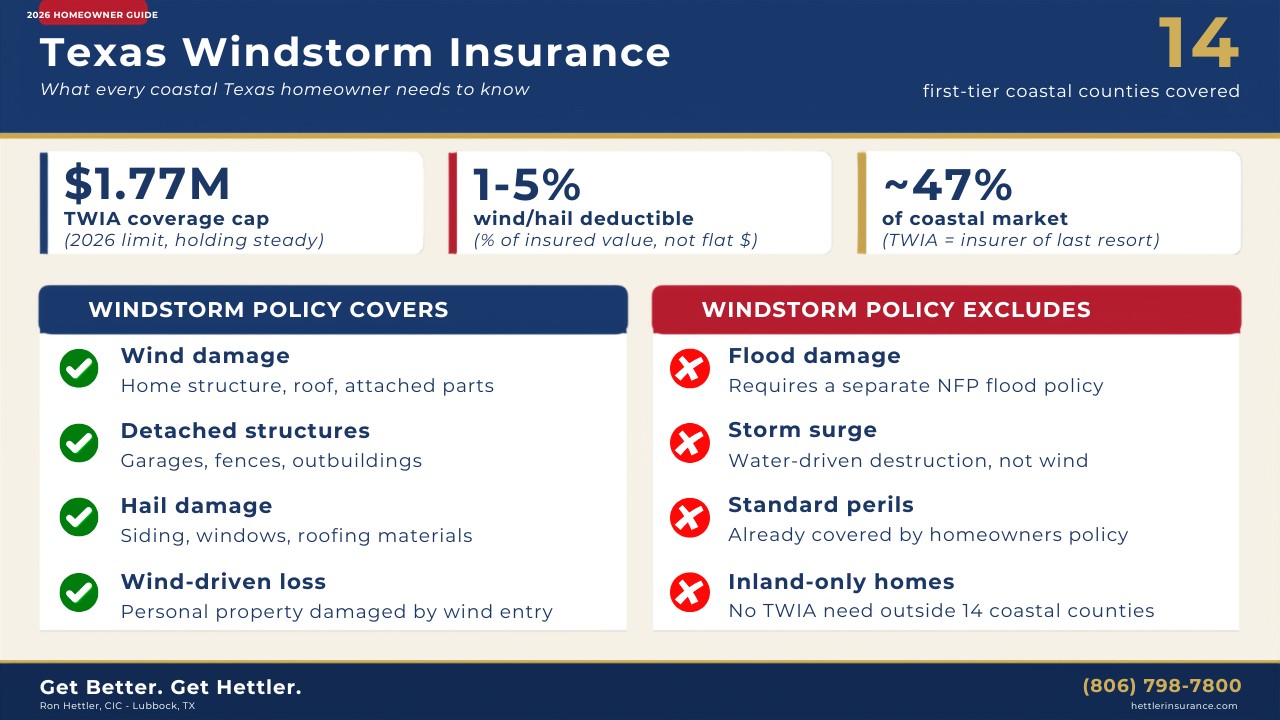

Windstorm insurance is a policy that covers physical damage to your home and belongings caused by wind and hail. According to the Texas insurance department’s explanation, windstorm insurance covers damage from hurricanes, tornadoes, and severe thunderstorms, but it is typically excluded from standard homeowners policies in coastal catastrophe areas while being included in standard policies further inland.

That distinction matters a great deal. If you own a home in Galveston, Corpus Christi, or another coastal community, your standard homeowners policy almost certainly does not cover wind damage. You need a separate windstorm policy to fill that gap. Inland homeowners in places like Lubbock or Amarillo usually have wind and hail included in their standard policy, though it is always worth confirming with your agent. You can find useful wind and hail policy tips to understand how this coverage applies to your specific situation.

What windstorm insurance covers:

- Wind damage to your home’s structure, roof, and attached structures

- Hail damage to siding, windows, and roofing

- Hurricane and tornado-related wind destruction

- Damage to detached garages, fences, and outbuildings (with proper coverage)

- Personal property inside the home damaged by wind entry

What windstorm insurance does NOT cover:

- Flood or storm surge damage (requires a separate flood policy)

- Fire, theft, or liability

- Mold or water damage not directly caused by wind

Important: Many homeowners confuse storm surge with wind damage. Storm surge is water-driven destruction, not wind. Your windstorm policy will not pay for it. You need flood insurance for that, typically through the National Flood Insurance Program (NFIP).

Windstorm claims also work differently from standard homeowners claims. You file directly with your windstorm insurer, not your regular homeowners carrier. Adjusters are trained specifically for wind damage, and the timeline can move faster than a general claim, especially after a declared disaster.

Understanding TWIA: Texas’s windstorm insurer of last resort

With the basics covered, let’s look at the main organizations and options Texans have for windstorm coverage.

The Texas Windstorm Insurance Association, known as TWIA, is the most well-known source of windstorm coverage for coastal Texans. TWIA is a non-profit, state-created insurer designed to step in when private insurance companies refuse to write windstorm policies in high-risk coastal areas. It is not a government agency, but it operates under state oversight.

The numbers tell the story of how significant TWIA is. TWIA serves approximately 252,000 to 285,000 policies, carries $113 to $127 billion in exposure, and holds roughly 47% of the coastal windstorm market in Texas. That is a massive share of the market, which reflects just how hard it is for coastal homeowners to find private coverage.

TWIA covers 14 first-tier coastal counties and parts of Harris County. If you live in one of those areas and a private insurer has declined to cover you, TWIA is your fallback option. You can review the full TWIA annual report for the most current data on their coverage footprint and financial standing.

TWIA vs. private windstorm insurance: a side-by-side comparison

| Feature | TWIA | Private market |

|---|---|---|

| Availability | Coastal counties only, last resort | Statewide, where offered |

| Eligibility | Must be denied by private insurer | Open market, no denial required |

| Coverage cap | $1.77 million (2026) | Varies by carrier |

| Pricing | State-regulated rates | Market-driven, can be lower |

| Flexibility | Limited endorsements | More customizable |

| Best for | High-risk coastal homes | Higher-value or lower-risk homes |

.

For higher-value homes, TWIA’s coverage cap can be a real problem. If your home is worth more than $1.77 million, you will need to supplement TWIA with a separate excess policy. Private carriers like Lloyd’s of London or surplus lines insurers sometimes offer better terms for these situations, which is why shopping around matters.

Who needs windstorm coverage and what are the requirements?

But who actually needs to buy windstorm insurance, and what hoops do you have to jump through?

The answer depends heavily on where your home is located. Inland Texas homeowners, think West Texas, the Panhandle, or Central Texas, typically have wind and hail built into their standard homeowners policy. Coastal homeowners in TWIA-eligible counties almost always need a separate windstorm policy.

Steps to get windstorm coverage through TWIA:

- Confirm your property is in an eligible county (14 first-tier coastal counties or parts of Harris County).

- Apply for coverage with a private insurer first. You must be denied before TWIA will accept you.

- Get a WPI-8 certificate, which is a building code compliance certificate issued after a state inspection.

- Submit your application to TWIA with proof of denial and your inspection certificate.

- Review your policy terms, deductibles, and coverage limits before binding.

As TWIA eligibility rules confirm, TWIA coverage requires a private insurer denial, location in specific counties, and passing a building code inspection. The law does not require you to carry windstorm insurance, but your mortgage lender almost certainly will. Most lenders in coastal areas will not fund or maintain a loan without proof of windstorm coverage.

Pro Tip: If your home was built before 1988 or has had major renovations, it may need a re-inspection before qualifying for TWIA. Get ahead of this early, because inspection delays can slow down your closing or leave you temporarily uninsured.

There are also edge cases to know. Homes in Coastal Barrier Resources Act (CBRA) zones are not eligible for TWIA at all. Older homes may face stricter inspection requirements. And in some situations, you may need flood insurance as a condition of your mortgage even before windstorm coverage comes into play. Review TWIA eligibility questions for detailed guidance on your specific situation.

Coverage, costs, and claims: what Texas homeowners can expect

Getting the policy is only one step. Understanding what you are buying and how it works in the real world is just as important.

A standard TWIA windstorm policy covers your dwelling (the structure of your home), other structures on your property, and personal property inside the home, but only for damage caused by wind or hail. This is called named peril coverage, meaning only the specific events listed in the policy are covered. Everything else is excluded.

What a windstorm policy typically covers:

- Structural damage to your home from wind or hail

- Roof damage, broken windows, and siding

- Detached structures like garages or sheds

- Personal belongings damaged by wind entry

What it does NOT cover:

- Flood or storm surge

- Personal liability

- Additional living expenses after a storm (you need your homeowners policy for that)

Sample rate comparison by location (2026 estimates):

| Location | Home value | Estimated annual premium |

|---|---|---|

| Galveston | $300,000 | $2,000 to $4,000 |

| Corpus Christi | $250,000 | $1,800 to $3,500 |

| Houston (coastal) | $350,000 | $2,500 to $4,500 |

| Lubbock (inland) | $300,000 | Included in HO policy |

.

Deductibles for windstorm policies are typically 1% to 5% of your home’s insured value, not a flat dollar amount. On a $300,000 home, a 2% deductible means you pay $6,000 out-of-pocket before the policy kicks in. That is a significant number to plan for.

TWIA 2026 rates are holding steady this year, which is good news for coastal homeowners. The 2026 TWIA coverage cap sits at $1.77 million, with claims settled in as few as 10 days after inspection in straightforward cases.

Pro Tip: Pair your windstorm policy with a flood policy and a standard homeowners policy to close all the gaps. A storm can cause wind damage, flooding, and fire all at once. One policy alone will not cover all three.

The smarter way: how homeowners can get better protection and value

With the mechanics covered, let’s get personal. What does all this mean for a savvy Texas homeowner, and what do most people get wrong?

The biggest mistake we see is homeowners defaulting straight to TWIA without checking the private market first. TWIA exists for a reason, and it serves a critical role, but it is not always the best deal. Private insurers can offer better terms than TWIA for some homeowners, particularly those with higher-value properties or newer construction that meets current building codes.

Carriers like Lloyd’s of London, Allstate, State Farm, and various surplus lines insurers do write windstorm coverage in Texas. Their rates can sometimes beat TWIA, especially if your home has impact-resistant roofing, storm shutters, or other wind-mitigation features. These upgrades can earn you meaningful discounts that TWIA’s regulated rate structure may not fully reflect.

Here is what we recommend: check private options first, compare the total cost including deductibles and coverage limits, and then make an informed decision. Do not skip the comparison step just because TWIA feels like the obvious answer.

Skipping windstorm insurance altogether is the other major pitfall. If your lender finds out you are uninsured, they will force-place a policy on your behalf, and force-placed insurance is almost always more expensive and less protective than what you could have chosen yourself. It protects the lender, not you.

Coordination is everything. Wind, flood, and homeowners coverage each fill a different role. A local independent agent who knows the Texas market can help you build a stack of policies that works together without overlap or gaps.

Looking for real savings and the right Texas windstorm policy?

Navigating TWIA, private carriers, deductibles, and building inspections is a lot to manage on your own. That is exactly where an independent agent earns their value.

At Hettler Insurance Agency, we represent over 30 top-rated carriers and shop both the TWIA and private markets to find the right windstorm policy for your Texas home. Whether you are on the Gulf Coast or in West Texas dealing with hail season, we compare your options at no extra cost to you. Get a windstorm insurance quote from our team today and find out if you can get better coverage at a lower price. Call us or visit online. Get Hettler, Get Better!

Frequently asked questions

Is Texas windstorm insurance mandatory?

Windstorm insurance is not required by state law, but most mortgage lenders in designated coastal areas will demand it as a condition of your loan if you do not have a private alternative.

What does a Texas windstorm policy cover?

It covers your home, personal belongings, and outbuildings from wind and hail damage, but flood and storm surge are excluded and require separate policies.

How much does Texas windstorm insurance cost?

2026 TWIA rates are holding steady, but premiums vary widely by location. A modest home in Galveston typically runs $2,000 to $4,000 per year, while inland homeowners usually pay nothing extra because wind is included in their standard policy.

How do I get Texas windstorm insurance?

Start with private insurers first. If you are denied, you can apply to TWIA after denial, but your property must pass a building code inspection and meet location eligibility requirements.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: Is Texas windstorm insurance mandatory?

Q2 ?: What does a Texas windstorm policy cover and exclude?

Q3 ?: How much does Texas windstorm insurance cost in 2026?

Q4 ?: How do I qualify for TWIA coverage?

Q5 ?: Why are windstorm deductibles 1–5% of insured value instead of a flat dollar amount?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com