TL;DR summary:

- On June 12, 2026, SpaceX went public at $135/share and closed up 19% — pushing Elon Musk’s paper net worth past $1 TRILLION, the first trillionaire in history.

- His wealth is concentrated in two volatile stocks and shielded by layers of legal structure — a luxury most West Texas families don’t have.

- Your “trillion-dollar lesson” isn’t about stocks. It’s whether your home, vehicles, farm, ranch, and small business are protected against the events that can wipe out your net worth in an afternoon. So, this is a West Texas insurance lesson.

On Friday, June 12, 2026, SpaceX went public on the Nasdaq under ticker SPCX, raised roughly $75 billion in the largest IPO in history, and closed the day up 19.2%. By the closing bell, Elon Musk’s paper net worth crossed $1 trillion — the first person ever to do it. That’s a remarkable headline. But here in Lubbock, Plainview, Midland-Odessa, Dallas, and across West Texas, families and business owners are asking a much more practical question: what does any of that have to do with my pickup, my home, or my small business?

Short answer: More than you might think. So, let’s discuss a West Texas insurance lesson.

Table of Contents

- What just happened with SpaceX and Elon Musk

- Why Musk’s “trillionaire” status is a paper headline

- Three risk principles every West Texas family should steal

- What this means for your home, auto, farm, and small business

- The umbrella policy: A West Texan’s “billionaire asset protection”

- A West Texas insurance specialist’s real take

- Protect what matters — your free Hettler coverage review

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Musk’s wealth is mostly paper | His ~$1.05–1.14 trillion net worth is the market value of SpaceX and Tesla shares — not cash — and can swing hundreds of billions in a single day. |

| Concentration is the real risk | Most West Texans have similar concentration — home, vehicles, business — but without billionaire-level protection around them. |

| Volatility hits everyone differently | For Musk, it’s the Nasdaq. For West Texans, it’s hail, tornadoes, wildfire, I-27 wrecks, and liability lawsuits. |

| Protection beats prediction | You can’t predict the next storm or accident, but you can decide today how protected you’ll be when one hits. |

| Umbrella policies are democratized asset protection | For roughly $150–$300 per year, a West Texan can layer an extra $1 million of liability protection on top of home and auto. |

.

What just happened with SpaceX and Elon Musk

On Friday, June 12, 2026, SpaceX went public on the Nasdaq Global Select Market under the ticker SPCX. The IPO priced at $135 per share, sold roughly 555.6 million shares, and raised about $75 billion — the largest IPO in market history.

When trading opened that morning, SpaceX shares jumped to $150 and closed at $160.95, a 19.2% first-day gain. Intraday, shares touched $176.52. By the closing bell, SpaceX carried a market capitalization of roughly $2.1 trillion.

Because Musk holds about a 42% stake in SpaceX and roughly 12% of Tesla (itself valued near $1.5 trillion), the IPO revaluation pushed his estimated net worth into the trillions. According to Forbes and Bloomberg trackers, he closed the day worth somewhere between $1.05 and $1.14 trillion — the first person in history to cross the trillionaire line, even if only on paper.

That’s a remarkable number. But the more useful question for a West Texas insurance lesson is: what does any of it have to do with your pickup, your home, or your small business?

Key takeaway: The “trillionaire” headline is really a story about how wealth — yours or his — is protected (or not) against the events that can wipe it out.

Why Musk’s “trillionaire” status is a paper headline

The first thing to understand is what kind of “trillionaire” Elon Musk actually is. Almost none of that trillion dollars is cash. It is the market value of stock he owns in two companies, and that value can rise — or fall — by tens of billions in a single trading session.

Several specific risks sit underneath the paper headline:

- Concentration: Nearly all of Musk’s wealth is tied to SpaceX and Tesla. There is very little diversification.

- Liquidity: Most of his shares are locked up by lockup periods, control structures, and the simple fact that selling at scale would crash the price. Only a small fraction is actually accessible.

- Volatility: Both SpaceX and Tesla are high-beta growth stocks. A 20–40% drawdown in either is not unusual historically.

- Leverage: Musk has pledged significant shares as collateral for personal loans, which can force sales or restructurings if prices fall too far.

- Policy risk: His companies depend heavily on government contracts and subsidies. Political and regulatory shifts can move the stock sharply.

In other words, “trillionaire” is a snapshot label that could disappear by Christmas — or by next Tuesday — if SpaceX or Tesla shares drop hard. The point isn’t to root for or against Elon Musk. The point is what his story reveals about how wealth — yours or his — actually works.

Three risk principles every West Texas family should steal

Buried in the SpaceX IPO headline are three financial principles that apply just as much to a Lubbock Texas household as to a billionaire on Wall Street.

- Volatility is real — yours just looks different. SpaceX swung from $135 to $176 and back to $160 in a single day. For West Texans, volatility shows up as a late-spring Plainview hailstorm that totals a roof in 20 minutes, a tornado warning over Lubbock County, a Midland grass fire that jumps a pasture line, a serious wreck on I-27 or US-84, or a customer slip-and-fall at your small business in Dallas.

- Concentration is dangerous. Musk’s wealth is concentrated in two companies. Most West Texas families have similar concentration risk — except instead of stocks, it’s their home, their vehicles, their farm or ranch equipment, or their small business. When most of your net worth sits in a handful of assets, protecting those assets isn’t optional. It’s the whole game.

- Protection beats prediction. Nobody knows whether SpaceX will be worth $3 trillion or $1 trillion at the end of next year. Likewise, nobody knows when the next hailstorm, wreck, or liability claim is coming. But you can decide in advance how protected you’ll be when one hits.

Pro Tip: Most West Texans haven’t reviewed their actual policy limits in 3–5 years. In that time, Texas construction costs, medical bills, vehicle repair costs, and jury awards have all climbed sharply. The right time to review your coverage is before a claim happens — not after. Start with this short refresher on how to avoid the most common insurance gaps in Texas. Then, continue reading this West Texas insurance lesson.

What this means for your home, auto, farm, and small business

Musk can afford a bad day in the market. Most West Texas families cannot afford a bad day with no coverage. Here’s how the “trillionaire news” translates into specific, practical action items.

Homeowners Insurance

Musk’s net worth can swing billions in a day. Your biggest “swing” might be a roof totaled by a single hailstorm — and in West Texas, that’s not hypothetical. The Texas Department of Insurance consistently ranks Texas among the top states for hail and wind insurance losses, and the average Texas homeowners policy now runs roughly $4,100 a year on a $300,000 dwelling — nearly double the national average.

What actually protects you:

- Replacement cost coverage — not actual cash value — so a 12-year-old roof gets replaced at today’s prices, not depreciated to nothing.

- Adequate dwelling limits — set to rebuild cost, not market value, because Texas construction costs have climbed sharply.

- A clear understanding of your wind and hail deductible. Most West Texas policies now use a 1–2% percentage deductible, which on a $300,000 home is $3,000–$6,000 per claim. We unpack exactly how this works in How Percentage Deductibles Work on Texas Homes.

- A Class 4 impact-resistant roof — most carriers credit 20–30% off the wind and hail portion of your premium.

Auto Insurance

SpaceX’s rockets reach orbit. Our vehicles reach I-27, Loop 289, Spur 327, FM-179, and the school pickup line. The most expensive financial risk for many West Texas families isn’t the cost of a car — it’s the cost of a serious at-fault accident. Texas state minimum liability limits (30/60/25) have not kept up with modern medical bills, vehicle repair costs, or jury awards. One bad wreck can lead to a six-figure liability claim that follows you for years.

Higher liability limits — 100/300/100 or more — typically cost a few extra dollars a month per vehicle. An umbrella policy on top costs less per month than what most people spend on streaming services.

Warning: If you’re still riding on the Texas state minimum auto liability limits of 30/60/25, one serious at-fault wreck on I-27 can mean a six-figure judgment that follows you for years — and the difference between “covered” and “not covered” is usually a few extra dollars a month.

Where West Texas “volatility” actually shows up

The table below contrasts billionaire-style risk with the day-to-day exposures we see on Lubbock kitchen tables — and what insurance product is actually built for each one. This table is an important part of this West Texas insurance lesson.

| Billionaire-style risk | West Texas household equivalent | Coverage that actually responds |

|---|---|---|

| Stock market crash | Hail or wind event totals a roof | Homeowners policy with replacement cost + realistic dwelling limits |

| Lawsuit from investors | At-fault auto wreck on I-27 with serious injuries | Higher auto liability limits + personal umbrella policy |

| Factory fire or supply-chain hit | Small business fire, theft, or storm shutdown | Business Owner’s Policy (BOP) with business interruption |

| Regulatory or political risk | Wildfire jumps a fence line; crop loss; livestock loss | Farm & ranch policy tailored to West Texas exposures |

| Concentrated stock exposure | Most of your net worth tied up in home + vehicles + business | Layered plan: home + auto + umbrella + business reviewed annually |

Small business, farm, and ranch insurance

SpaceX is capital-intensive. So is a cotton farm in Lynn County, a welding shop in Slaton, or a retailer on Broadway here in Lubbock, Texas. If a fire shuts down operations, a customer slips and falls, equipment is stolen, or a hailstorm wipes out a crop, the question is the same: does my coverage actually replace what I lost, or does my business close?

- Business Owner’s Policy (BOP) bundles general liability, commercial property, and business interruption — typically saving small Texas businesses 15–25% versus buying each policy standalone. We walk through the mechanics in our BOP workflow guide.

- Farm and ranch policies in West Texas need to address hail, wildfire, livestock, equipment, and crop exposures that standard homeowners coverage simply doesn’t touch.

- Workers’ compensation is technically optional for most private Texas employers, but going without it strips your business of key legal defenses and exposes you to unlimited employee injury lawsuits.

The umbrella policy: A West Texan’s “billionaire asset protection”

Elon Musk has lawyers and corporate structures whose entire job is shielding his assets from massive claims. He didn’t get to a trillion dollars by ignoring downside risk. For West Texas families, the simple version of that same idea is a personal umbrella policy.

An umbrella policy sits on top of your home and auto liability coverage and adds an extra $1 million, $2 million, $3 million, or more in liability protection. It kicks in when a claim blows past your primary policy limits.

Why this matters in Lubbock and West Texas specifically:

- Texas juries can — and do — award damages that exceed the typical home or auto policy limit

- Many West Texas households have farm, ranch, or small-business exposures that compound liability risk

- Umbrella coverage is one of the cheapest dollar-for-dollar coverages in all of insurance: $1 million of extra protection often costs $150–$300 per year for the average household

Key takeaway: You don’t need a billion-dollar legal team to protect what you’ve built. You need a properly layered insurance plan — and an umbrella policy is the most affordable layer of all.

Pro Tip: When you stack home, auto, umbrella, and a Business Owner’s Policy with the same independent agency, you can usually capture multi-policy discounts and ensure those policies talk to each other when a claim happens. That coordination is what most “lowest-rate” online quotes leave out.

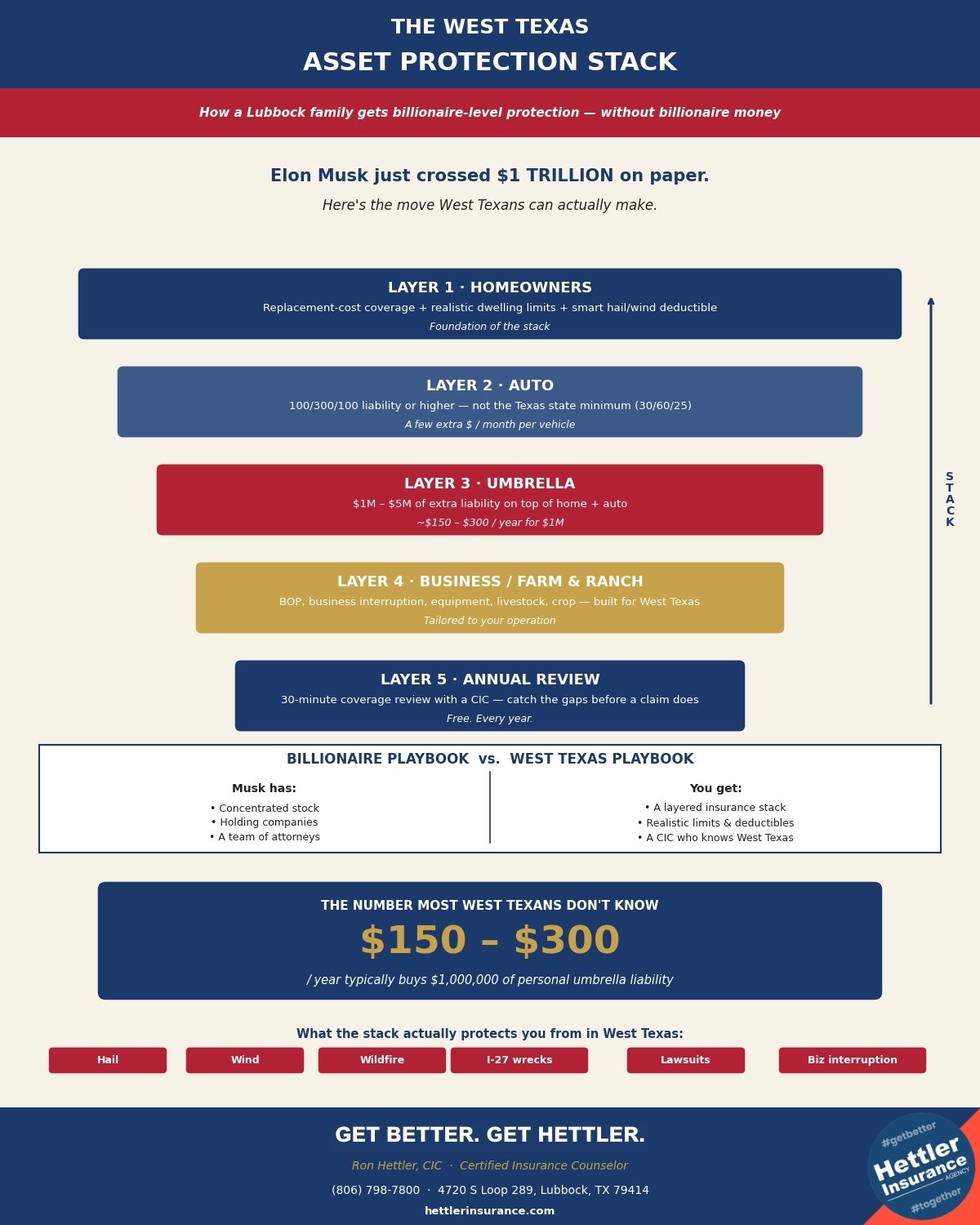

The five layers of a West Texas asset protection stack showing five insurance layers — homeowners, auto, umbrella, business or farm and ranch, and annual review — for Lubbock families — built by Ron Hettler, CIC. | Don’t do insurance alone. Hettler speaks insurance-ese. Call (806) 798-7800.

Why this concept:

It visualizes the article’s central argument — that a layered insurance stack is the West Texas equivalent of the corporate / legal structures shielding Musk’s trillion-dollar paper net worth — and it leads with the single most-shareable stat from the article: only $150–$300/year buys $1M of umbrella liability.

A West Texas insurance specialist’s real take

Here’s the part the financial news won’t tell you. Elon Musk’s trillion-dollar headline matters less than what it reveals: every household and business has a “net worth” that can be wiped out by a handful of events. For a billionaire, those events are stock market crashes, regulatory actions, or lawsuits. For a West Texas family, those events are hailstorms, wrecks, fires, theft, and liability claims.

The single biggest mistake we see at Hettler Insurance Agency isn’t carrying too little coverage. It’s owning a home, a couple of vehicles, and possibly a small business — and never sitting down to ask whether the existing policies actually protect them anymore.

Premiums change. Property values change. Texas construction costs change. Your family’s situation changes. The policy that fit your life ten years ago — or even three years ago — is almost certainly not the policy you need today. That’s exactly why we recommend working with an independent agency representing 30+ carriers rather than a single-carrier captive office: when your needs change, your coverage can move with you.

A free annual coverage review takes 30 minutes. It can identify the gap between what you think you have and what you actually have. And it can mean the difference between an inconvenience and a financial crisis when the next storm rolls across the Caprock.

Protect what matters — your free Hettler coverage review

You don’t have to buy SpaceX stock to “act” on this headline. (And we are not giving investment advice.) The smarter move for almost every West Texan is much closer to home:

- Review your home and auto liability limits

- Confirm your home, business, or farm is insured to realistic replacement values — not old purchase prices

- Add an umbrella policy if you have a home, a decent income, or any significant assets

- Ask questions until you understand, in plain language, what is and isn’t covered

If a trillionaire is working that hard to protect his assets, it’s worth asking: have you done everything reasonable to protect yours? We can’t launch rockets, and we definitely don’t manage a trillion dollars. But Ron Hettler, CIC (Certified Insurance Counselor) and the Hettler Insurance Agency team help West Texans protect what matters most — homes, vehicles, farms, ranches, and local businesses — every single day. Thank you for following along with this West Texas insurance lesson.

If you need a no-pressure review of your current policies, call (806) 798-7800 or stop by 4720 S Loop 289 in Lubbock. You can also start an online home quote in minutes. You don’t need billionaire problems to deserve a smart risk plan. Get Better. Get Hettler.

*Sources: CNBC, BBC News, The New York Times, Washington Times, Capital.com, TheStreet, Texas Department of Insurance.

Primary keyword: Lubbock insurance agency

Secondary keywords: West Texas home insurance, Lubbock umbrella insurance, hail insurance West Texas, farm and ranch insurance Lubbock, asset protection Texas, Elon Musk Trillionaire wealth and risk management

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Frequently Asked Questions ?

Q1 ?: Is Elon Musk really a trillionaire now?

Q2 ?: What does the SpaceX IPO have to do with my West Texas insurance?

Q3 ?: What is an umbrella policy and do I really need one in Lubbock?

Q4 ?: Why are West Texas home and auto premiums so high right now?

Q5 ?: How do I get a free coverage review with Hettler Insurance Agency?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com