TL;DR summary:

- Independent insurance agents in Lubbock provide tailored coverage by shopping multiple carriers to address regional risks like hail, tornadoes, and flooding. They offer ongoing reviews, endorsements, and cost-saving strategies that captive agents cannot match, ensuring better protection and affordability for local families. Choosing a knowledgeable, community-involved agency with extensive carrier access ensures comprehensive, value-driven insurance solutions in West Texas.

Most people assume buying insurance is straightforward. You pick a company, get a quote, and sign. But if you own a home in Lubbock, Texas, that assumption could cost you thousands. West Texas weather is unpredictable, local risks are specific, and a policy that works fine in Austin may leave a Lubbock family seriously underinsured after a hailstorm. Independent insurance agents are built precisely for situations like this. They shop across dozens of carriers, explain your options without pressure, and help you get coverage that actually fits your life and your zip code.

Table of Contents

- What makes Lubbock’s insurance risks unique?

- Independent vs. captive insurance agents: what’s the difference?

- How independent agents deliver savings and better coverage

- Choosing the right independent agency in Texas

- Why independent insurance is the smarter path for Lubbock’s families

- Get started with smarter independent insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Local risks require custom coverage | Independent agents tailor insurance to Lubbock’s unique hazards, ensuring you’re properly protected. |

| Freedom to choose and save | You get more options and potential savings by comparing multiple carriers through an independent agent. |

| Trusted guidance for Texas families | Independent agencies offer education, responsiveness, and deep insight into local insurance needs. |

| Captive vs. independent matters | Knowing the difference between agent types empowers you to pick smarter, flexible policies. |

What makes Lubbock’s insurance risks unique?

Now that you know independent insurance matters, let’s see why Lubbock coverage needs are different from most of the state.

Lubbock sits squarely in the heart of Tornado Alley. The region experiences some of the most intense hail events in Texas every spring and summer. Wind-driven storms can destroy roofs overnight, and the flat, treeless landscape gives severe weather almost nothing to slow it down. Flooding, while less frequent, can still hit hard during heavy rain events because the terrain drains poorly in many neighborhoods.

Standard insurance policies sold nationally are often written for average conditions across the country. They may cap hail damage claims, exclude certain wind-related losses, or set replacement cost limits that do not reflect the actual cost of materials and labor in West Texas. That gap between what you assume you’re covered for and what your policy actually pays is called a coverage gap, and it’s more common than most Lubbock homeowners realize.

Here’s what local risks you need to think about:

- Hail damage to roofs, siding, windows, and vehicles

- Tornadoes and high winds that can total a home entirely

- Flash flooding in low-lying areas of the city

- Dust storms that cause visibility accidents and property damage

- Wildfires in surrounding rural areas that can threaten homes on the outskirts

Working with an agency that has 25 years serving Lubbock means working with professionals who know exactly which risks to watch for. A local independent agent will know which neighborhoods flood, which carriers have paid hail claims fairly, and which policy endorsements (add-ons that expand your coverage) are worth the extra premium. That kind of knowledge does not come from a national call center.

Changes in risk underwriting in 2026 mean carriers are evaluating regional hazards more precisely than ever before. Some are tightening hail coverage. Others are pulling out of certain Texas markets entirely. A local independent agent tracks these shifts in real time and steers you toward carriers that remain committed to the region.

Pro Tip: Ask your agent specifically about storm endorsements and flood riders. Standard homeowners policies often exclude flood damage entirely. A separate flood policy or a flood endorsement may be available, and in Lubbock, it is worth asking about every single year.

Independent vs. captive insurance agents: what’s the difference?

Understanding local risks is key, but how you buy insurance matters just as much.

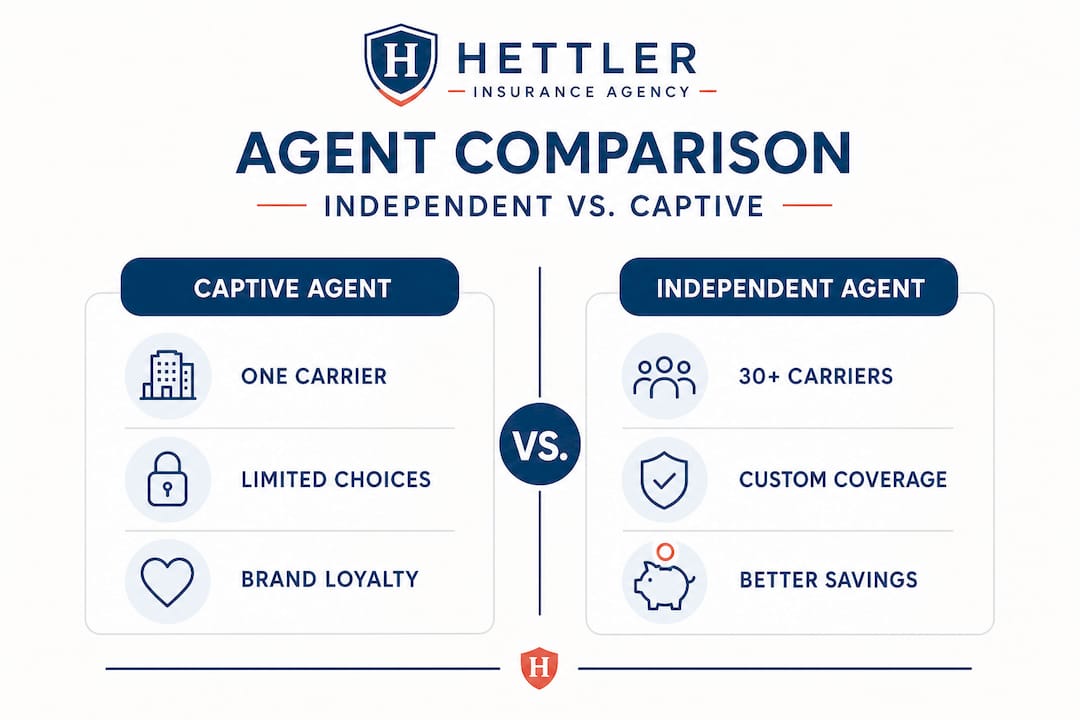

There are two types of insurance agents. Captive agents represent a single insurance company. Think of the well-known brand-name agencies where the agent sells only that company’s products. They know their company’s products well, but they cannot shop around on your behalf. If that company’s rates go up or their coverage terms change, your only option is to accept it or find a new agent entirely.

Independent agents, on the other hand, represent multiple insurance carriers. They are not tied to one company’s products, prices, or underwriting rules. They work for you, not for the carrier.

Here is a side-by-side comparison:

| Feature | Captive agent | Independent agent |

|---|---|---|

| Carrier options | One company only | 10 to 30+ carriers |

| Price shopping | Not available | Shops on your behalf |

| Coverage flexibility | Limited to one product line | Broad and customizable |

| Local market knowledge | Varies widely | Often deep and specific |

| Loyalty | To their employer | To the client |

| Annual policy review | Rarely offered | Standard practice |

| No extra fee for service | Sometimes | Yes, at Hettler |

The 2026 insurance market has made this distinction even more critical. Carrier consolidation, rising reinsurance costs, and climate-driven underwriting changes mean that loyalty to one company can leave you exposed. The carrier you’ve been with for a decade may no longer offer the best rate or even the right coverage for your home.

Here is how the process changes when you work with an independent agent:

- You share your situation. Your agent learns about your home, vehicles, family, and specific concerns, including any local risks like hail or flooding.

- Your agent shops the market. They pull quotes from multiple carriers and compare coverage terms, not just price.

- You review real options. Your agent explains the differences in plain language so you can make an informed decision.

- Your agent recommends the best fit. This recommendation is based on your needs, not on which carrier pays the highest commission.

- You get an annual review. Your independent agent checks in each year to make sure your coverage still fits as your life changes.

You can find answers to common questions about this process in the agency’s insurance agent FAQs. And if you’ve ever wondered whether a smaller carrier might actually serve you better than a large national brand, the breakdown at small vs. large carriers is worth reading before your next renewal.

Independent agents also stay current on digital networking for agents and industry tools, which helps them move faster and communicate more clearly with clients.

How independent agents deliver savings and better coverage

But even more important than agent type is how independence drives cost and coverage in practical, measurable ways.

When an independent agent has access to 30 or more carriers, something powerful happens. Carriers compete for your business. That competition directly benefits you through lower premiums, better coverage terms, and more flexible deductible options. This is not theoretical. Hettler Insurance added its 8th auto carrier back in 2018, and the agency has continued expanding its carrier roster to ensure clients always have real choices.

One of the most effective cost-saving strategies available through an independent agent is bundling. When you combine your home and auto policies under the same carrier, most companies offer a multi-policy discount that can range from 5% to 25% of your total premium. You can learn more about how to bundle for savings in a way that makes financial sense for West Texas families specifically.

Here are the most impactful cost-saving moves that only an independent agent can make possible for you:

- Annual market reviews to make sure you are not overpaying as rates shift across carriers

- Bundle discounts by placing home, auto, and umbrella policies with the same carrier

- Claims history analysis to place you with carriers that reward clean records

- Coverage right-sizing to eliminate gaps and remove redundant coverage you are paying for twice

- Deductible optimization to balance your premium cost against realistic out-of-pocket exposure

- Endorsement reviews to add critical protections like replacement cost coverage on personal property

Knowing when to check auto insurance rates is another area where an independent agent adds visible value. Most families set their auto policy and forget it. But rates change constantly, and a policy that was competitive two years ago may now cost significantly more than comparable coverage from another carrier.

The table below shows a quick look at where savings typically show up for Lubbock families:

| Savings strategy | Typical annual impact | Who makes it possible |

|---|---|---|

| Bundling home and auto | $200 to $600 | Independent agent |

| Annual rate shop | $150 to $800 | Independent agent |

| Coverage gap correction | Varies, often significant | Independent agent |

| Deductible adjustment | $100 to $400 | Either agent type |

| Loyalty discount | $50 to $150 | Captive agent only |

Working with a trusted restoration partner also matters when a claim does happen. Independent agents often maintain relationships with local contractors and restoration companies, which can speed up claims and reduce the stress of recovery after a storm.

Choosing the right independent agency in Texas

Ready to pursue independent insurance? Choosing the right agency can make all the difference in what you get from the relationship.

Not all independent agencies are built the same. Some have access to only a handful of carriers. Others lack the local knowledge to identify Lubbock-specific risks. Here is a checklist to help you evaluate any agency before you commit:

- Carrier access. Ask how many carriers they represent. Fewer than 10 is a warning sign. A strong agency like Hettler represents over 30.

- Local experience. How long have they served the Lubbock or West Texas market? Local history means local knowledge.

- Credentials. Look for agents who hold a Certified Insurance Counselor (CIC) designation. This is the gold standard in the industry and requires ongoing continuing education.

- Annual review policy. A quality agency proactively reviews your coverage each year, not just at renewal.

- Communication. Can you reach a real person quickly? Is your agent responsive to claims questions and life changes?

- Community involvement. Agencies rooted in the community have a stronger incentive to serve you well long-term.

- No-pressure environment. You should never feel pushed toward a specific carrier or product. A good agent educates first.

If you are still figuring out how to start finding insurance in Lubbock, that resource walks through some of the common challenges and what to look for in a local agency.

You can also review insurance provider options to better understand the landscape of carriers operating in Texas before you begin your search.

“The best independent agents don’t just sell policies. They build relationships, review coverage annually, and treat every client like a neighbor. In a market as unpredictable as West Texas, that kind of ongoing partnership is what protects families when it matters most.” — Ron Hettler, CIC, Founder, Hettler Insurance Agency

Pro Tip: Look for agencies that are actively involved in the Lubbock community. An agency sponsoring local events, supporting local nonprofits, or showing up consistently in the community is one that plans to be here for the long haul. That commitment matters when you file a claim.

You can also watch a helpful walkthrough on choosing the best independent agency in Texas to help you ask the right questions before you sign anything.

Why independent insurance is the smarter path for Lubbock’s families

With these criteria in mind, let’s step back for a frank look at why independence matters most in a market like Lubbock.

Here is something most insurance articles won’t tell you. A captive agent is not your advocate. They are a sales representative for their employer’s products. That’s not an insult. It’s simply the structure they operate within. When Lubbock sees a bad hail season, some captive carriers respond by raising rates across the board, tightening coverage terms, or non-renewing policies in higher-risk zip codes. A captive agent cannot offer you an alternative. They can only apologize and process your renewal at the new, higher rate.

We’ve seen this play out repeatedly over the years. After major storm seasons, Lubbock families who were locked in with a single-company agent found themselves scrambling for new coverage with far fewer options. Families who worked with Lubbock insurance options through an independent agency were simply moved to a different carrier, often with comparable coverage at a better price. The process was smooth because the relationship was already in place.

The other uncomfortable truth is this: most people are underinsured, not because they chose bad policies, but because they were never educated about their options. A captive agent doesn’t always have the time or the incentive to explain coverage gaps, endorsement options, or what your policy actually excludes. An independent agent’s business model depends on keeping you satisfied and informed, year after year. That accountability changes how you are treated.

Don’t wait for a claim to find out your coverage isn’t what you thought it was. The time to ask hard questions is before the hailstorm, not during it.

Get started with smarter independent insurance

Finally, here’s how to take advantage of local expertise for your insurance needs.

If you are ready to stop guessing and start getting coverage that actually fits your home, your family, and your West Texas lifestyle, Hettler Insurance Agency is the place to start. Whether you are protecting your first home, looking to lower your auto premium, or wondering what minimum insurance for entrepreneurs looks like for a side business, the team at Hettler can walk you through your options without pressure.

Founded in 1992 by Ron Hettler, CIC, the agency represents over 30 top-rated carriers and has earned recognition from Three Best Rated and Expertise.com as one of the leading insurance agencies in Lubbock. With a 4.5-star Google rating and an A+ BBB rating, the agency’s track record speaks for itself. Visit hettlerinsurance.com to get a quote, review your current coverage, or simply ask a question. The team is ready to shop the market on your behalf and find the right fit at the best price, at no extra fee to you.

Frequently asked questions

Why do independent insurance agents offer more choices in Lubbock?

Independent agents work with multiple carriers, allowing them to tailor coverage and pricing for Lubbock’s unique risks. Because they represent over 30 insurers, they can shop the market and find policies that captive agents simply cannot access, as demonstrated by agencies like Hettler that have added carriers specifically to serve West Texas clients better.

Can bundling home and auto policies really save money for Texas families?

Yes, bundling policies with an independent agent often results in discounts and more flexible coverage options. Combining home and auto under one carrier can reduce your total premium significantly, and a Lubbock-specific approach to bundling home and auto ensures those savings account for local risks at the same time.

What’s the difference between captive and independent insurance agents?

Captive agents represent only one company, while independent agents can offer policies from many insurers. In the current Texas market, that distinction is especially important because carriers are adjusting their coverage terms and pricing in response to storm activity, and enrollment and market shifts have made access to multiple carriers more valuable than ever before.

How do I know which independent agency is best for my family?

Look for agencies with local expertise, strong communication, and track records of helping families with unique Texas risks. The video guide on choosing the best independent agency in Texas offers practical questions you should ask before you commit to any agency.

Are independent agents more expensive than captive agents?

Often, independent agents find policies with better coverage at lower prices due to their access to many carriers. Because they can compare dozens of options on your behalf, independent agents routinely identify savings that offset any perceived cost difference, which is why expanding carrier access is a priority for agencies committed to client value.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com