TL;DR summary:

- How to avoid insurance gaps in Texas:

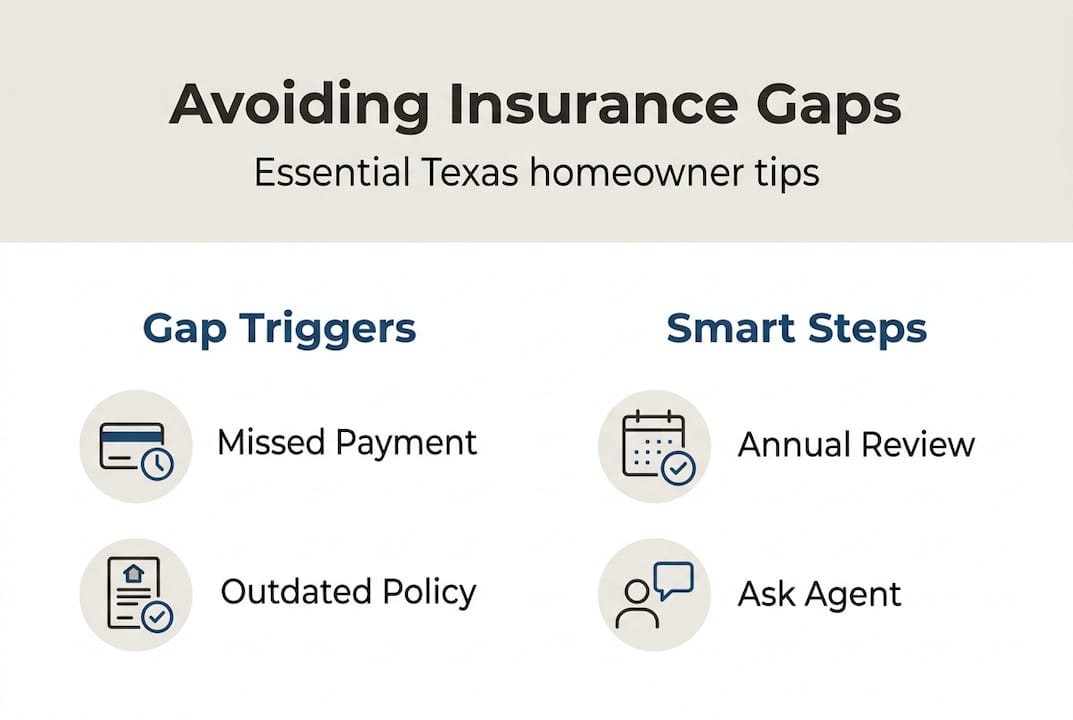

- Insurance gaps in Texas often result from missed payments, non-renewals, or outdated policies.

- Standard policies exclude flood and may limit windstorm coverage, requiring separate add-ons or endorsements.

- Regular policy reviews and proactive updates prevent underinsurance and costly coverage lapses.

A hailstorm rolls through your neighborhood, leaves a hole in your roof, and you call your insurance company expecting relief. Instead, you learn your policy lapsed two months ago after a missed payment, and now you’re facing tens of thousands in repair costs out of pocket. This scenario plays out for Texas homeowners more often than most people realize. Insurance gaps, meaning periods when your home has no active coverage or inadequate coverage, can happen fast and cost you everything. This guide walks you through exactly how gaps occur, what your policy likely excludes, and the practical steps to keep your Texas home fully protected year-round. (By the way, GAP is also an auto insurance term, but see the other article for that.)

Table of Contents

- Understand what causes insurance gaps in Texas

- Checklist: Coverage essentials and standard exclusions

- Stay protected: Keeping coverage up to date

- Avoid lapses and know your backup plans

- A fresh perspective: The less obvious pitfalls most Texas homeowners miss

- Get expert help to secure complete coverage

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Pay premiums on time | Missing payments leads to costly lender-placed insurance and increased future rates. |

| Review exclusions annually | Standard policies often exclude flood and wind; extra coverage may be necessary. |

| Update for home changes | Always adjust coverage after renovations, roof updates, or ownership shifts. |

| Act fast if non-renewed | Shop immediately or turn to the Texas FAIR Plan if you lose coverage. |

Understand what causes insurance gaps in Texas, so you know how to avoid insurance gaps in Texas

An insurance gap is any period when your home is either uninsured or underinsured relative to the actual risks you face. It does not have to mean zero coverage. A policy that excludes wind damage in a hail-prone area like Lubbock Texas is just as dangerous as no policy at all. So, let’s understand how to avoid insurance gaps in Texas

Common scenarios that create gaps for Texas homeowners:

- Missing a premium payment or failing to renew on time

- Letting a policy expire while shopping for a cheaper rate

- Leaving a home vacant for more than 60 days without notifying your insurer

- Assuming your standard policy covers flood or wind when it does not

- Failing to update your policy after a major renovation or ownership change

Paying premiums late or missing renewals can result in force-placed insurance, higher costs, and coverage restrictions. Force-placed insurance, also called lender-placed insurance, is a policy your mortgage lender buys on your behalf when yours lapses. It protects the lender, not you, and it typically costs two to three times more than a standard policy with far less protection.

Vacant homes over 60 days lose most coverage, and lenders can force-place expensive policies in that situation. If you own a rental property or a second home that sits empty for stretches, this rule applies directly to you.

Important: The long-term consequences of a coverage gap extend beyond the immediate claim denial. Your insurer may flag you as high-risk, which raises your future premiums significantly. Some carriers will refuse to write a new policy if you have a recent lapse on record.

Texas homeowners insurance also fall into gaps through common insurance mistakes like assuming their coverage automatically adjusts for inflation or that their lender’s requirements equal full protection. They do not. Understanding these pitfalls is the first step toward closing them, and that is how to avoid insurance gaps in Texas.

| Gap trigger | Immediate risk | Long-term consequence |

|---|---|---|

| Missed payment | Policy cancellation | Higher future premiums |

| Vacancy over 60 days | Most coverage suspended | Force-placed policy |

| Coverage exclusions | Claim denied | Out-of-pocket repair costs |

| Non-renewal | No active policy | Lapse on insurance record |

After recognizing the risks, the next step is knowing the essentials every Texas homeowner needs.

Lubbock Texas homeowner reviewing insurance paperwork at kitchen table

Checklist: Coverage essentials and standard exclusions

Standard Texas homeowners insurance policies, often called HO-3 policies, cover your dwelling, personal property, liability, and additional living expenses if your home becomes uninhabitable. But what they exclude is just as important as what they cover when you want to know how to avoid insurance gaps in Texas.

Covered vs. excluded perils in a standard Texas HO policy:

| Peril | Standard HO-3 | Requires separate coverage |

|---|---|---|

| Fire and smoke | Covered | No |

| Windstorm and hail | Often excluded in coastal/high-risk zones | TWIA or endorsement |

| Flood | Never covered | NFIP or private flood policy |

| Roof damage (aging roof) | Limited or excluded | Endorsement needed |

| Water backup/sewer | Usually excluded | Add-on endorsement |

Texas HO policies exclude flood; wind and hail often require coverage through TWIA (Texas Windstorm Insurance Association); and roof age matters for what type of payout you receive. If your roof is over 10 to 15 years old, many carriers will only pay actual cash value (the depreciated amount) rather than replacement cost. That difference can be thousands of dollars.

If your home sits in or near a floodplain, a separate flood policy through the National Flood Insurance Program or a private carrier is not optional. It is essential.

How to verify what your policy actually covers:

- Pull out your declarations page and read the list of covered perils carefully.

- Look for exclusions listed in Section I of your policy document.

- Check whether wind and hail are covered or excluded based on your county.

- Confirm whether your roof is covered at replacement cost or actual cash value.

- Ask your agent directly: “What would not be covered if a storm hit my home tomorrow?”

Pro Tip: Do not wait for a claim to discover your exclusions. Call your agent and ask them to walk through your policy with you. A 20-minute conversation now can prevent a five-figure surprise later.

Once you know what your current policy excludes, it is time to make sure your coverage amounts are adequate.

Stay protected: Keeping coverage up to date

Buying a policy and forgetting it is one of the most common and costly mistakes Texas homeowners make. Your home’s value changes. Construction costs change. Your personal property changes. Your policy needs to keep up.

Life events that require a policy update:

- Major renovation or addition (kitchen remodel, new room, pool)

- Roof replacement

- Purchase of high-value items (jewelry, electronics, art)

- Change in home ownership structure (adding a spouse, transferring to a trust or LLC)

- Renting out part of your home

- Installing a home security system (may qualify for discounts)

Rebuild costs in Texas rose up to 50% since 2020, usually outpacing inflation guard add-ons that many policies include automatically. An inflation guard endorsement typically adjusts your dwelling coverage by 4 to 8 percent annually. When actual construction costs jump 30 to 50 percent in just a few years, that add-on falls far short, and you need to know how to avoid insurance gaps in Texas.

Annual policy reviews ensure your dwelling coverage matches current costs, especially given recent Texas construction increases. Schedule this review every year, ideally before your renewal date.

Underinsurance is a silent gap. You may have a policy in force, but if your dwelling coverage is set at $200,000 when your home would cost $320,000 to rebuild, you are exposed to a $120,000 shortfall. This is especially common for homeowners who bought years ago and never updated their coverage limits. Learn more about what drives policy increases so you can plan ahead rather than react.

One often-overlooked situation: if you transfer your home into a trust or LLC for estate planning purposes, your existing homeowners policy may no longer be valid. The named insured on the policy must match the legal owner of the property. Get this confirmed in writing before any ownership transfer.

Also, if you are moving or storing belongings, review how possessions are protected during moves since your homeowners policy may offer only limited off-premises coverage.

Pro Tip: Take a video walkthrough of your home every year and store it in the cloud. If you ever need to file a claim, this documentation speeds up the process and supports your case.

Texas climate trends and rising rebuild costs are not slowing down. Staying proactive with your coverage is the only reliable defense.

Keeping your coverage updated is crucial, but avoiding a gap also means responding quickly to changes in your insurance status.

Avoid lapses and know your backup plans

Preventing a lapse starts with simple habits, but knowing your options when a carrier drops you is just as important so you’ll know how to avoid insurance gaps in Texas.

Steps to prevent a coverage lapse:

- Set up automatic premium payments through your insurer or mortgage escrow account.

- Add your policy renewal date to your calendar with a 45-day advance reminder.

- Keep your contact information updated with your insurer so notices reach you.

- If you receive a cancellation notice, call your agent the same day. Do not wait.

- Review any non-renewal notice carefully. Insurers must give you a reason.

Texas law gives homeowners 60 days notice before a non-renewal takes effect, and the Texas FAIR Plan provides basic last-resort coverage if you are denied by two or more insurers. The FAIR Plan (Fair Access to Insurance Requirements) is not a preferred option. It offers limited coverage at higher rates. But it keeps you from being completely uninsured while you search for a standard carrier.

Premiums rose sharply post-pandemic, non-renewals doubled, and FAIR Plan policies surged across Texas. Over 41,000 Texas homeowners were enrolled in the FAIR Plan as of 2024, a number that reflects how many people are being pushed out of the standard market. If you receive a non-renewal, do not panic. Act immediately.

If your insurer non-renews your policy: Contact an independent agent right away. They can shop across multiple carriers simultaneously to find replacement coverage before your current policy expires. Do not let even one day go uncovered.

The effects of urban growth in areas like Lubbock also affect your risk profile and available carriers, so working with a local agent who understands the West Texas market matters. If you are relocating, also check relocation coverage options to make sure you are not exposed during the transition.

With these strategies, you are prepared to act fast if your coverage is at risk. Now let us look at the less obvious pitfalls that even careful homeowners tend to miss.

A fresh perspective: The less obvious pitfalls most Texas homeowners miss

Most homeowners believe that as long as they pay their bill and auto-renew, they are covered. That assumption is where the real danger hides.

Auto-renewal does not update your coverage limits. It does not add flood protection. It does not account for the new addition you built last spring. Your policy renews at the same terms it had last year, even if your home’s rebuild cost has jumped significantly.

Trust and LLC ownership mismatches are another trap. Estate attorneys set up these structures without always coordinating with the insurance agent. The result: a claim gets denied because the named insured does not match the legal property owner.

Then there is the inflation guard assumption. Many homeowners see this endorsement on their policy and assume they are covered for rising costs. In a normal market, maybe. In Texas since 2020, construction inflation has outrun standard guard percentages by a wide margin.

The fix is not complicated. Review your common pitfalls with a knowledgeable agent annually. Ask pointed questions. Document everything. Proactive homeowners do not get surprised at claim time.

Get expert help to secure complete coverage

If reading this guide made you realize your current policy might have gaps, you are not alone. Most Texas homeowners have at least one area of underinsurance they are unaware of.

At Hettler Insurance Agency, we represent over 30 top-rated carriers and specialize in Texas-specific risks including hail, wind, flood, and rising construction costs. Our team reviews your existing policy, identifies gaps, and shops the market to find the right fit at the best price. There is no extra fee for this service. Whether you need to understand minimum insurance requirements or want a full coverage overhaul, we are here to help. Call us or request a review online. Get Hettler, Get Better.

Frequently asked questions

What should I do if my Texas homeowners policy is non-renewed?

Shop for a new policy immediately and consider the Texas FAIR Plan if denied by two or more insurers, as Texas law requires 60 days notice before non-renewal takes effect.

Are flood and wind/hail covered by all Texas home insurance policies?

No. Texas standard HO policies exclude floods entirely, and wind and hail may require separate TWIA coverage depending on your region.

How often should I review my homeowners coverage?

Review your policy annually or after major changes like renovations or roof replacements to make sure your dwelling coverage reflects current rebuild costs.

What happens if I miss a premium payment?

A missed payment can trigger a policy lapse, leading to force-placed insurance and significantly higher costs that protect your lender, not you.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: What is an “insurance gap” on a Texas homeowners policy?

Q2 ?: What does a standard Texas HO-3 policy typically exclude?

Q3 ?: Why is my “auto-renewed” policy still risky?

Q4 ?: What should I do if my insurer non-renews my policy?

Q5 ?: How often should I review my Texas homeowners coverage?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com