TL;DR:

- Proper business owners policy workflow steps ensure Texas businesses avoid coverage gaps and claim denials.

- Accurate data intake and thorough review of declarations pages are essential at every stage.

- Ongoing verification habits protect businesses from costly errors and ensure policy alignment.

Running a small or mid-sized business in Texas means managing countless moving parts. Your insurance should not be one of the things that catches you off guard. Many business owners in Texas sign a policy, file it away, and assume they are fully protected until a claim arrives and they discover a gap that should never have existed. That gap almost always traces back to a workflow problem, not a coverage problem. Follow the right steps from data intake through final verification, and you can avoid overpaying, prevent missed endorsements, and walk into any claim situation with confidence.

Table of Contents

- Understanding your business owners policy workflow

- Preparing for your BOP workflow: Data intake and eligibility

- Quoting to binding: Step-by-step business owners policy workflow process

- Verifying accuracy: Reviewing declarations and endorsements

- Why business owners policy workflows could break down: What most business owners miss

- Get expert help optimizing your business owners policy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Define a clear business owners policy workflow | Having a structured process reduces errors and gaps in BOP coverage. |

| Use data-driven intake | Accurate business info at the start speeds up quoting and reduces eligibility issues. |

| Verify endorsements | Match all endorsements and forms in the policy with what was agreed during underwriting. |

| Conduct end-to-end review | A declarations page check is essential before finalizing your business owner’s policy. |

Understanding your business owners policy workflow

A business owners policy, commonly called a BOP, bundles property coverage and general liability protection into a single policy designed for small and mid-sized businesses. It is not just a convenience. It is a carefully structured contract where every form, endorsement, limit, and deductible must be documented and verified accurately. When any piece is out of place, you may face a claim denial or a payout far below what you expected.

The BOP workflow is the sequence of steps that moves your coverage from initial application to a finalized, binding policy. Think of it as a production line. If one station on the line makes an error, every stage that follows it carries that error forward. For Texas business owners specifically, the workflow has to account for state-specific carrier requirements, property risks like hail and wind, and industry-specific endorsements that vary by business type.

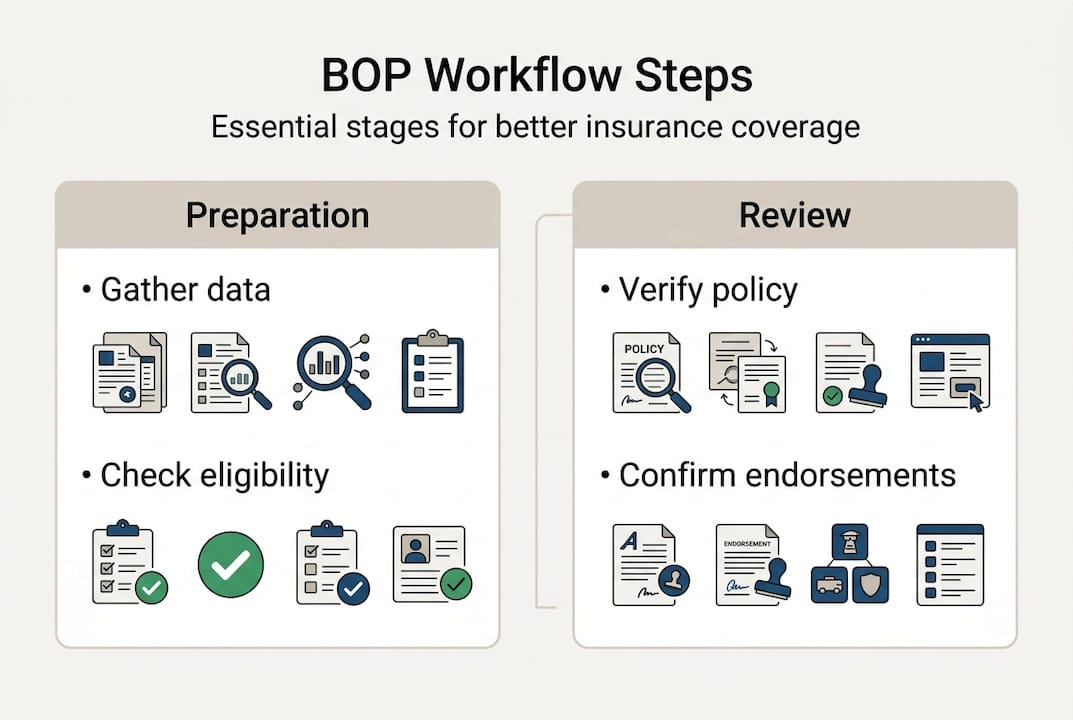

A standard BOP workflow moves through five stages:

- Data collection: Gathering accurate business and property information before quoting begins

- Coverage selection: Choosing the right property and liability limits for your specific risk profile

- Endorsement review: Confirming which optional coverages (called endorsements) need to be added to the base policy

- Binding: Finalizing the policy with the carrier and locking in coverage

- Verification: Reviewing the declarations page after binding to confirm everything agreed upon is actually in place

The declarations page (commonly called the “dec page”) is your most important tool throughout this entire process. According to insurance documentation standards, a strong workflow includes a declarations-level “single source of truth” review: ensure the declarations accurately list forms and endorsements, limits, deductibles, premises, and the effective dates that govern coverage.

Skipping any of these stages, or treating them as automatic, is where coverage gaps begin. Reviewing your insurance FAQs is a good starting point for understanding the terminology you will encounter at each stage.

Pro Tip: Print your declarations page on day one of your new policy and compare it line by line against what your agent quoted. If anything does not match, call before you file.

Optimize Business Owners Policy BOP Workflow for Better Coverage | Hettler Insurance Agency, Lubbock Texas, call phone 8067987800 | Come in at 4720 S Loop 289, Lubbock Texas

Preparing for your BOP (business owners policy workflow) workflow: Data intake and eligibility

The most preventable mistakes in any BOP workflow happen before a single quote is generated. Inaccurate or incomplete data at intake does not just slow things down. It can result in a non-bindable submission, meaning a carrier refuses to finalize your policy at all. Worse, it can mean the policy binds with incorrect information that quietly voids specific coverages.

Here is what you need to have ready before your agent begins quoting:

| Information required | Why it matters |

|---|---|

| Legal business name | Must match the named insured on all policy documents |

| Business address and premises details | Determines property risk, zone, and carrier eligibility |

| Annual gross revenue | Used to set general liability limits and premium basis |

| Payroll figures | Impacts workers’ compensation and some liability calculations |

| Full description of operations | Identifies industry-specific endorsement needs |

| Prior loss history (5 years) | Affects carrier eligibility and pricing |

| Square footage of owned or rented property | Sets building and contents values |

Getting these details right the first time matters more than most owners realize. The quoting workflow’s data intake sequence, moving from carrier eligibility to endorsement selection, is specifically designed to prevent stalling or non-bindable submissions. When the data is clean going in, the rest of the workflow runs without friction.

Here is a numbered process to follow for intake preparation:

- Confirm your legal business structure (LLC, sole proprietor, corporation) because carriers classify risk differently by structure.

- Pull your most recent profit and loss statement so revenue and payroll figures are precise, not estimated.

- List every physical location where your business operates, stores inventory, or has employees on-site.

- Document any special equipment or high-value contents that may require scheduled property endorsements.

- Request your prior loss runs from your current carrier so your agent can review your claims history accurately.

Common eligibility traps for Texas businesses include operating in a class code (a carrier’s internal industry classification) that a particular carrier excludes, having a prior loss that exceeds a carrier’s threshold, or owning a building that exceeds the square footage limit for a standard BOP. An independent agent with deep operational insurance experience can identify these traps early and route your application to the right carrier before you waste time on a dead-end quote.

Pro Tip: Never round up or estimate revenue figures on a BOP application. Overstated revenue can spike your premium unnecessarily. Understated revenue can create a co-insurance penalty at claim time, where the carrier only pays a proportional share of your loss.

Quoting to binding: Step-by-step policy workflow process

Once your data is accurate and carrier eligibility is confirmed, the workflow moves into the active quoting and binding phase. This is the stage where most handoff errors occur, and where even a small miscommunication between you, your agent, and the underwriter can produce a policy that does not match your actual needs.

Follow these steps carefully during this phase:

- Request quotes from multiple carriers. An independent agent can submit your application to multiple carriers simultaneously, giving you real options to compare on price, coverage breadth, and carrier financial strength.

- Compare coverage terms, not just price. Two policies at similar premiums may have vastly different property sub-limits, liability exclusions, or deductible structures.

- Select endorsements deliberately. Endorsements are add-ons that customize your BOP. Common examples include equipment breakdown coverage, cyber liability, hired and non-owned auto, and ordinance or law coverage. Each one must be specifically requested and formally attached.

- Confirm the forms list before binding. Every endorsement and form should appear on a list within your quote documentation. If your agent says it is included but it is not listed, it is not binding.

- Review the final quote summary with your agent line by line before authorizing the bind.

Use declarations review as a formal control point: verify that the endorsements and forms actually attached to the policy match what you agreed upon during underwriting. Treat discrepancies as a reason to correct before binding.

The table below compares how different endorsement handling approaches affect your coverage outcome:

| Endorsement handling method | Result |

|---|---|

| Verbal confirmation only | High risk of omission; not legally binding |

| Written quote with forms list | Low risk; provides documentation trail |

| Declarations page post-bind review | Best practice; confirms what actually bound |

| No review after binding | Coverage gaps go undetected until a claim |

Understanding your minimum insurance requirements before you begin quoting keeps the process anchored. And when it comes to setting deductibles, getting solid insurance deductibles advice before you choose a figure can prevent a painful out-of-pocket surprise at claim time.

Pro Tip: Ask your agent to send the bound policy declarations page within 48 hours of binding. Do not wait for the full policy packet to arrive by mail weeks later. Early review means early correction.

Verifying accuracy: Reviewing declarations and endorsements

Binding the policy is not the finish line. It is actually the moment when the most important review step begins. Many Texas business owners treat binding as the end of the process, but experienced agents treat it as the beginning of the verification stage.

The declarations page is the official summary of your entire policy. As documented by insurance policy standards, the Businessowners Policy declarations page is the “snapshot” showing named insured, policy term, covered premises, purchased coverages and limits, applicable deductibles, schedule of forms and endorsements, and premium basis. It is the document used to verify that endorsements and limits match the agreed risk plan.

Use the following checklist when reviewing your declarations page after binding:

- Named insured: Is your legal business name spelled correctly and listed completely?

- Policy term: Are the effective and expiration dates accurate?

- Covered premises: Are all business locations listed, including any secondary or seasonal locations?

- Coverage types and limits: Do the property and liability limits match what you requested?

- Deductibles: Is the deductible amount for each coverage type what you agreed to?

- Forms and endorsements list: Is every endorsement you selected specifically listed by form number?

- Premium basis: Is the revenue or payroll figure used to calculate your premium accurate?

Any discrepancy on this list is not a minor administrative issue. It is a potential coverage gap that a carrier can point to during a claim to limit or deny payment. Missing an endorsement, for example, means that coverage does not exist, regardless of what was discussed verbally or quoted in writing.

The declarations page is your single source of truth. If an endorsement is not listed on it, the coverage is not in force. This applies to every policy term without exception.

Getting into the habit of reviewing your dec page at every renewal is one of the most effective policy optimization tips any business owner can follow. It takes 20 minutes and can prevent a claim denial that costs tens of thousands of dollars. If you ever need to understand how this verification step connects to the broader insurance claim preparation process, the connection is direct: a clean, accurate declarations page is the foundation of every successful claim.

Pro Tip: After reviewing the declarations page, create a one-page coverage summary for your own records. Include coverage types, limits, deductibles, and endorsement names. Store it digitally and share it with your office manager or bookkeeper so someone else in your organization understands what is in force.

Why workflows break down: What most business owners miss

After more than 30 years working with Texas business owners, here is what we have observed time and again: the workflow does not usually break down because someone chose the wrong policy. It breaks down because everyone assumed someone else was handling the details.

The business owner assumes the agent caught every endorsement. The agent assumes the underwriter attached every form. The underwriter assumes the dec page was reviewed. Nobody actually checks. Then a claim arrives, and suddenly the missing equipment breakdown endorsement is not a paperwork oversight. It is a $40,000 out-of-pocket repair that the business owner has to absorb.

Small handoff errors have real consequences. A premises address listed incorrectly can void property coverage for that location entirely. An annual revenue figure left as an estimate can trigger a co-insurance penalty. An endorsement discussed in a meeting but never formally added to the policy simply does not exist. These are not hypothetical situations. They happen to Texas businesses every year.

The difference between a business owner who files a successful claim and one who gets a denial letter often comes down to one thing: a control mindset. Not just a checklist. A mindset that says, “I will not assume this is correct. I will verify it myself.” As a core principle, treat discrepancies as a reason to correct before binding, not after.

That verification habit, applied consistently at every renewal and every mid-term change, is the hidden workflow step that separates businesses with genuine protection from those with an illusion of it.

Get expert help optimizing your business owners policy

Putting this workflow into practice is straightforward when you have an experienced team guiding each step. At Hettler Insurance Agency, we have helped Texas business owners build BOP workflows that catch errors before they become claim denials.

Our team shops across more than 30 top-rated carriers to find coverage that fits your business accurately, not just approximately. Whether you are reviewing an existing policy or starting a new one, we walk you through every stage: data intake, carrier eligibility, endorsement selection, and post-bind verification. Understanding your minimum insurance for entrepreneurs is just the starting point. Call us today at Hettler Insurance Agency in Lubbock and let us make sure your BOP is working as hard as your business does.

Frequently asked questions

What is the declarations page in a business owners policy?

The declarations page is a summary sheet listing the named insured, policy term, covered locations, coverages, limits, and attached endorsements. Per insurance policy standards, it serves as your coverage snapshot and the primary verification tool for confirming your policy reflects what you agreed to with your carrier.

How can I avoid errors during the BOP workflow?

Always double-check that endorsements and limits on the declarations page match your agreed risk plan before binding the policy. Following the principle to verify before binding ensures that any discrepancies are corrected while they are still easy to fix.

What information do Texas business owners need to start a BOP quote?

You will need your legal business name, property addresses, payroll info, annual revenue, and a clear description of operations to begin. The data intake sequence is specifically designed to prevent stalled or non-bindable submissions, so accurate data at the start saves time for everyone involved. There’s a business owners policy workflow

How often should I review my BOP workflow?

Review your workflow and policy details at every renewal, or any time your business operations change significantly, to ensure your coverage remains accurate and there are no gaps introduced by mid-term changes.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: What is the declarations page in a Business Owners Policy?

Q2 ?: What information do Texas business owners need to gather for an accurate BOP quote?

Q3 ?: What are the five stages of a thorough BOP workflow?

Q4 ?: Which endorsements should Texas businesses commonly review on a BOP?

Q5 ?: How can I avoid coverage gaps and errors during the BOP workflow?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com