TL;DR summary:

- Liability coverage protects your assets from injuries or property damage claims.

- Texas homeowners aren’t required by law to carry liability insurance but lenders often mandate it.

- Adequate limits, often $300,000 to $500,000 for homeowners and $1 million for businesses, are essential.

Most Texas homeowners and small business owners assume liability coverage is optional. That assumption can cost you everything. Liability coverage is the part of your insurance policy that pays for injuries or property damage you cause to others, and while Texas law does not mandate it for homeowners, your mortgage lender almost certainly does. If you run a business, your client contracts likely require it too. A single lawsuit from a slip-and-fall on your property or a customer injured at your shop can result in six-figure legal bills. This guide walks through what liability coverage does, how homeowners and business policies differ, what Texas-specific risks you face, and how to choose limits that actually protect you.

Table of Contents

- Understanding liability coverage: What it does and why you need it

- Key differences: Homeowners vs. small business liability coverage

- Typical exclusions and Texas-specific risks

- How much liability coverage do you really need in Texas?

- The real risk: Why ‘just enough’ coverage isn’t really enough in Texas

- Get help choosing the right liability coverage for you

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Liability coverage basics | It pays for injuries or damages you’re responsible for, protecting both homeowners and business owners from lawsuits. |

| Coverage isn’t automatic | Texas doesn’t legally require liability coverage, but most lenders and contracts do. |

| Know policy exclusions | Standard liability policies often exclude business activities at home, intentional acts, and household injuries. |

| Choose adequate limits | Selecting the right amount means considering your assets, risks, and local Texas trends—often more is better than the bare minimum. |

| Umbrella policies help | Umbrella liability insurance provides extra protection beyond what standard policies cover. |

Understanding liability coverage: What it does and why you need it

Liability coverage is the portion of your insurance policy designed to protect your financial assets when you are found legally responsible for causing harm to someone else. That harm can be physical injury or damage to someone’s property. If a neighbor trips on a cracked step at your front door and breaks a wrist, liability coverage pays for their medical bills and any legal costs if they sue you.

The Texas Department of Insurance explains that liability coverage in Texas homeowners insurance pays for medical and legal costs when you are responsible for injuring someone or damaging their property. That is a broad protection, but it has firm boundaries.

There are two main types most Texans encounter:

- Personal liability covers incidents that happen at your home or result from your personal actions. Think of a guest injured at your backyard cookout or your kid accidentally breaking a neighbor’s window.

- General liability covers businesses against third-party claims. If a customer slips at your shop, or your employee damages a client’s property while on the job, general liability responds.

One important distinction: most homeowners liability claims do not require you to pay a deductible. The policy pays the claim directly, without coming out of your pocket first. That is different from your dwelling or personal property coverage, which typically comes with a deductible.

“Liability coverage doesn’t just pay damages, it also funds your legal defense. Attorney fees alone in a civil lawsuit can easily reach tens of thousands of dollars before a verdict is ever reached.”

It is also worth noting that Texas law does not require homeowners to carry liability coverage. But your mortgage lender almost certainly does, and if you sign a commercial lease or a client contract, those agreements often require minimum liability limits too. Avoiding common homeowners insurance mistakes starts with understanding what your policy already includes and where the gaps are.

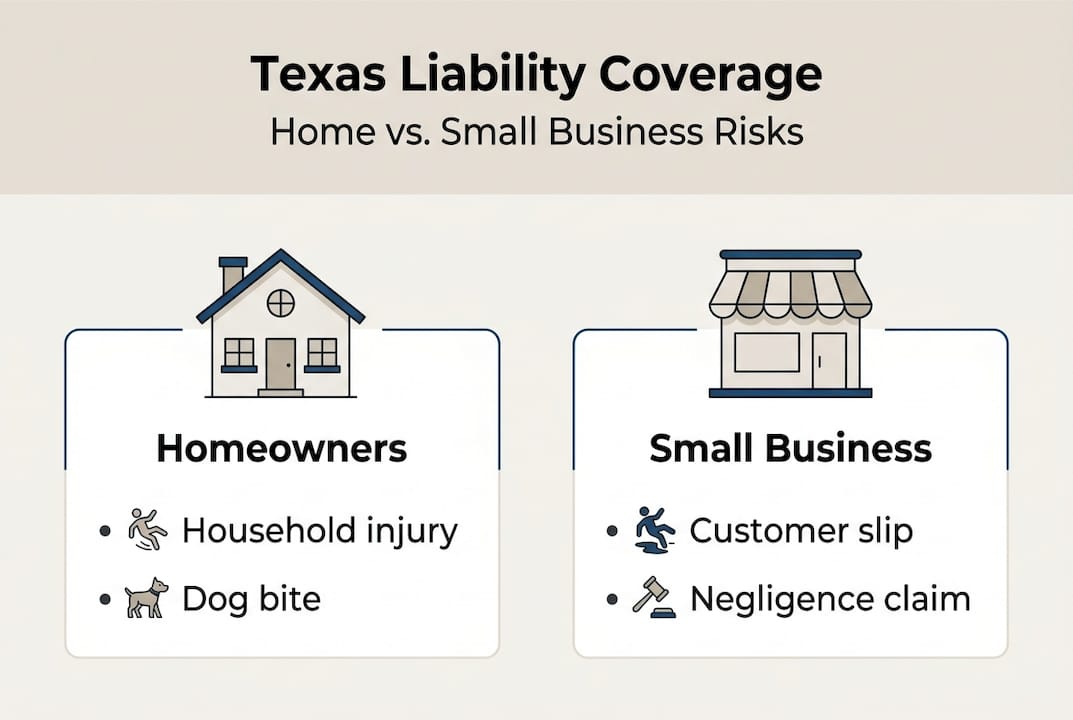

Key differences: Homeowners vs. small business liability coverage

With the basics down, let’s compare how liability coverage protects you at home versus in your small business. The core function is the same: protect your assets if someone makes a claim against you. But the details, limits, and exclusions differ significantly.

| Feature | Homeowners liability | Small business liability |

|---|---|---|

| Who it covers | You and household members | Business, employees, operations |

| Typical limits | $100,000 to $500,000 | $1M per occurrence, $2M aggregate |

| Deductible | Usually none | Varies by policy |

| Business activities | Excluded | Included (BOP or GL policy) |

| Legal defense costs | Included | Included |

| Workers’ compensation | Not applicable | Separate policy required |

A homeowners policy will not protect you if you are running a business out of your home and a client gets hurt during a visit. That claim falls under a business activity, which is typically excluded from homeowners coverage. The Texas Real Estate Research Center notes that personal liability differs from general liability, and business risks are specifically carved out from standard homeowners policies.

Here is a real-world example to make this clear. Your friend comes over for a weekend barbecue, slips on a wet patio, and sprains an ankle. Your homeowners liability handles that. But if a client visits your home office, trips on the same patio, and sues you for lost wages due to the injury, your homeowners policy may deny that claim because it involved a business activity. That is a gap that a Business Owners Policy (BOP) or a standalone general liability policy would cover.

Small business owners may also need Errors and Omissions (E&O) coverage, which is a type of professional liability policy that covers claims related to advice or services you provide. A contractor, consultant, or accountant faces very different risk exposure than a retail shop, and understanding personal vs. general liability helps you avoid paying for the wrong type of protection.

Pro Tip: If you operate any kind of home-based business, even part-time freelancing, notify your insurance agent. A simple endorsement (an add-on to your existing policy) may be all you need, or you may need a separate policy. Either way, you need to know.

Typical exclusions and Texas-specific risks

Even with liability coverage, not everything is covered. Next, let’s zero in on what these policies typically exclude, especially in Texas.

Most liability policies, whether for homes or businesses, exclude the following:

- Intentional acts. If you deliberately injure someone or destroy their property, your policy will not pay for it.

- Business activities at home. As noted above, any income-producing activity is usually excluded from a homeowners policy.

- Auto accidents. Car-related liability is covered under your auto policy, not your home policy.

- Household member injuries. If someone who lives with you gets hurt in your home, liability coverage typically does not apply.

- Contractual liability. If you sign a contract agreeing to be liable for something you otherwise would not be, that may not be covered.

Texas adds its own layer of complexity. The state of Texas sees significant weather events, from hail in Lubbock to flooding along the Gulf Coast. While weather damage to your property falls under property coverage, liability claims tied to weather events can arise. For example, if a dead tree on your property falls and damages your neighbor’s fence, Texas law requires proof of negligence for the tree owner to be liable. The Houston Chronicle explains that Texas tree liability requires showing the owner knew or should have known the tree was hazardous.

Texas also has active litigation trends. Slip-and-fall lawsuits, premises liability claims, and contractor disputes are all common. If you are a small business owner, the risk is even higher because customers, vendors, and contractors all have potential grounds for claims against you.

To reduce your exposure to exclusions, take these steps:

- Tell your agent about any home-based business activity, no matter how small.

- Have dead or damaged trees professionally assessed and document the evaluation.

- Review your auto liability requirements separately from your home coverage to avoid any gaps between policies.

- Ask your agent to walk through your specific exclusions line by line.

Knowing what your policy does not cover is just as important as knowing what it does.

How much liability coverage do you really need in Texas?

Having seen where standard policies may fall short, it is crucial to know how much protection is right for your specific needs. There is no single correct answer, but there are clear factors that determine your minimum safe limit.

- Your total assets. If you own a home with equity, investment accounts, or other valuable assets, a lawsuit can target all of it. Your coverage limit should at least match your net worth.

- Your risk profile. A home with a pool, trampoline, or frequent visitors has more exposure than a home without those features. A business with foot traffic has far more exposure than a solo consultant.

- Contract obligations. If a client contract requires you to carry $1 million in general liability, your standard $300,000 homeowners limit simply will not satisfy that requirement.

- Local risk factors. West Texas hail, tornado activity, and Texas litigation trends all increase your potential exposure compared to lower-risk states.

- Type of business operations. Businesses that work on client property or handle high-value goods face larger potential claims than those with limited physical exposure.

For most Texas homeowners, a minimum of $300,000 in personal liability is a reasonable starting point, but $500,000 is better. For small business owners, $1 million per occurrence and $2 million aggregate is the standard general liability baseline.

Beyond standard limits, umbrella liability insurance adds an extra layer of protection over your existing home or business policy. An umbrella policy typically kicks in after your underlying policy limits are exhausted, and it usually provides an additional $1 million to $5 million in coverage at a relatively low premium. The TDI 2024 Property and Casualty Report shows that general liability premiums and losses are rising, with umbrella policies increasingly recommended to offset growing litigation risk.

Pro Tip: Review your liability limits every year and any time you experience a major life change, such as buying a new home, starting a business, or hiring employees. Find out more about minimum business insurance requirements so you never find yourself under-covered when it matters most.

The real risk: Why ‘just enough’ coverage isn’t really enough in Texas

Here is an honest observation after decades of helping Texans manage their insurance needs. The most dangerous mindset we see is not “I don’t need coverage.” It is “I have the minimum, so I’m covered.”

Minimum coverage satisfies a lender or a contract requirement. It does not protect you against real-world financial exposure. In Texas, where jury verdicts in civil cases routinely exceed policy limits and severe weather creates chain-reaction liability scenarios, the gap between “minimum required” and “actually protected” is wider than most people realize.

Consider this: the marginal cost difference between $100,000 and $500,000 in personal liability is often less than $20 per year on a homeowners policy. Yet the difference in protection during a serious claim is enormous. Checking whether you have sufficient home insurance coverage is not pessimistic thinking. It is responsible planning.

We encourage every client to think through their worst-case scenario. If a serious injury happened on your property tomorrow, would your current limits cover it? If the answer is uncertain, that is the answer.

Get help choosing the right liability coverage for you

Choosing the right liability limits is not a decision you should make by guessing or by defaulting to whatever your lender requires.

At Hettler Insurance Agency, our team of experienced, CIC-credentialed agents works with over 30 top-rated carriers to find coverage that fits your exact risk profile, whether you are protecting a family home in Lubbock or running a small business in West Texas. We assess your assets, your exposures, and your contract obligations, then shop across carriers to get you the best value. We also help you understand Texas business insurance needs and personal liability options side by side. Visit Hettler Insurance Agency or call us today for a no-obligation policy review. Get Hettler, Get Better.

Frequently asked questions

Is liability coverage required by law in Texas?

No, Texas law does not require homeowners to carry liability coverage, but mortgage lenders and contracts typically mandate it as a condition of doing business.

What does liability insurance not cover in a Texas homeowners policy?

It typically excludes business activities, intentional acts, car accidents, and injuries to household members, regardless of fault.

Does liability insurance cover accidents on my property if I wasn’t at fault?

Yes, your liability coverage can pay for injuries to others even without a finding of fault, handled through medical payments coverage included in most policies.

Do I need extra liability coverage if I have an umbrella policy?

An umbrella policy adds coverage above your standard policy limits, but it requires underlying coverage to be in place first and does not replace your base liability policy.

What is the difference between occurrence-based and claims-made liability policies?

Occurrence-based policies cover any incident that happens during the policy period, while claims-made policies only respond if the claim is reported while the policy is still active.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: Is liability coverage required by law in Texas?

Q2 ?: What is typically excluded from a Texas homeowners liability policy?

Q3 ?: How much liability coverage do I really need in Texas?

Q4 ?: How does an umbrella policy fit in?

Q5 ?: What is the difference between occurrence-based and claims-made liability policies?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com