Lubbock TX Homeowners Guide [3 Common Homeowners Insurance Mistakes]

Buying homeowners insurance often feels like a box to check at closing. The paperwork is overwhelming, timelines are tight, and many homeowners assume all policies are basically the same.

Unfortunately, that’s how costly mistakes happen.

At Hettler Insurance Agency, we regularly review policies for homeowners insurance in Lubbock and West Texas and see the same issues again and again. Below are the three biggest mistakes homeowners make when buying homeowners insurance — and how to avoid them.

Mistake #1: Insuring the Home for the Purchase Price Instead of the Rebuild Cost

One of the most common — and most expensive — mistakes homeowners make is assuming their insurance should be based on what they paid for the home. But, homeowners insurance is designed to cover the cost to rebuild the home after a covered loss, not the real estate market value or sales price.

In Lubbock, this distinction matters. Construction costs fluctuate, labor availability can change, and rebuilding after a widespread storm can be significantly more expensive than homeowners expect.

Why this homeowners insurance mistake is risky

— Rebuild costs often differ from market value

— Older homes may require specialized materials or updated building codes

— Construction labor and material costs can rise unexpectedly

— Being underinsured can lead to out-of-pocket costs after a major loss

How to avoid it

Make sure your policy is based on a current replacement cost estimate, and review that estimate periodically as costs and home features change.Mistake #2: Choosing the Cheapest Policy Without Understanding What’s Excluded

Price matters — but homeowners insurance is not a commodity. Two policies with similar coverage limits can provide very different protection depending on:

— deductible structure

— roof coverage

— wind and hail provisions

— personal property valuation

— how claims are settled

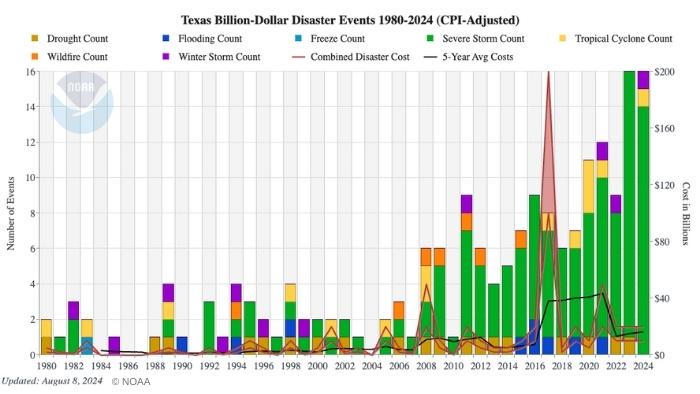

In West Texas, where wind and hail claims are common, these differences can have a major impact when a claim occurs.

Many homeowners don’t realize that a 1% or 2% wind or hail deductible is based on the home’s insured value — not a flat dollar amount. For example, a 2% deductible on a $350,000 home means you could be responsible for $7,000 out of pocket before insurance applies.

Common surprises homeowners discover too late

— Not realizing percentage-based deductibles are a percent of the home’s insured value

— Limited roof settlement options

— Restrictions on certain types of water damage

— Coverage limitations for high-value personal property

How to avoid it

Ask what’s excluded or limited, not just what’s covered. In many cases, paying slightly more upfront can result in significantly better protection when it matters most.

In Texas, and especially in West Texas, wind and hail deductibles deserve special attention. These deductibles are often percentage-based and apply specifically to storm-related claims. Because hail and wind damage are among the most common homeowners claims in the Lubbock Texas and West Texas area, understanding how these deductibles work before a loss occurs is essential.

Mistake #3: Overlooking Liability Exposure and Personal Risk

Many homeowners focus entirely on protecting the house itself, but liability claims are often the most financially damaging losses.

Homeowners liability coverage helps protect you if someone is injured on your property or if you’re found legally responsible for damage to others. However, many policies carry liability limits that can be exceeded faster than homeowners realize.

Common liability risks we see locally

— Guests injured at the home

— Dog-related incidents

— Backyard pools or trampolines

— Accidents involving teenage drivers

— Claims that extend beyond the home itself

How to avoid it

Review your liability limits and consider whether umbrella liability insurance makes sense. Umbrella coverage provides an extra layer of protection beyond homeowners and auto insurance and is often more affordable than people expect.

Bonus Mistake: Not Reviewing Coverage as Life Changes

Homeowners insurance should not be treated as a one-time decision.

Renovations, new vehicles, increased income, added assets, or changes in household members can all affect how much coverage you need. Yet many homeowners go years without reviewing their policy.

A periodic coverage review helps ensure your protection keeps pace with your life.

How Hettler Insurance Helps Homeowners Avoid These Mistakes

As an independent insurance agency in Lubbock, Hettler Insurance Agency works with multiple insurance companies to help homeowners:

— Insure their home based on accurate rebuild costs

— Understand policy differences beyond price

— Identify coverage gaps before claims occur

— Adjust coverage as homes and lifestyles change

If you’re unsure whether your current homeowners insurance is truly protecting you — or if you’re purchasing a new home — a review can provide clarity and peace of mind.

👉 If you’d like a second opinion on your homeowners insurance, contact Hettler Insurance Agency in Lubbock Texas, to schedule a no-pressure coverage review. * Click to Call us @ (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm).

-- Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

-- Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

-- Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com