TL;DR Summary:

- Understanding insurance deductible guide for Texas, deductible types and their impact helps Texas homeowners prepare financially for storms.

- Choosing a deductible aligned with your risk, home value, and savings prevents unexpected expenses.

- Implementing upgrades and policy strategies can reduce deductible costs and improve storm resilience.

Your roof just took a direct hit from a Texas hailstorm. The adjuster walks through, confirms the damage, and you’re expecting a check to cover most of the cost. Then the number hits you: your deductible is $6,000. That moment of sticker shock is something thousands of Texas homeowners experience every year after major storms. Having an insurance deductible guide for Texas before a claim is filed changes everything. This guide breaks down exactly how deductibles work, how to pick the right one for hail and flood coverage, and what practical steps you can take right now to protect your home and your bank account.

Table of Contents

- What is an insurance deductible guide for Texas? Understand the basics

- How to pick the right deductible for your Texas home

- How claim deductibles work for hail and flood damage

- Savings strategies: Reduce your deductible burden

- Our take: How to approach insurance deductibles in Texas

- Get personalized insurance deductible advice for your Texas home

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Deductibles affect claim payouts | The amount you select for your deductible is subtracted from your claim payment, so choose wisely. |

| Percent-based deductibles can cost more | A 2% deductible in Texas can mean thousands out-of-pocket after a major hail or flood event. |

| Savings strategies are available | Upgrading your roof and bundling home and flood insurance can help lower both your premiums and future deductible costs. |

| Update regularly | Review your deductible choices at every renewal to make sure they still fit your risk and budget. |

.

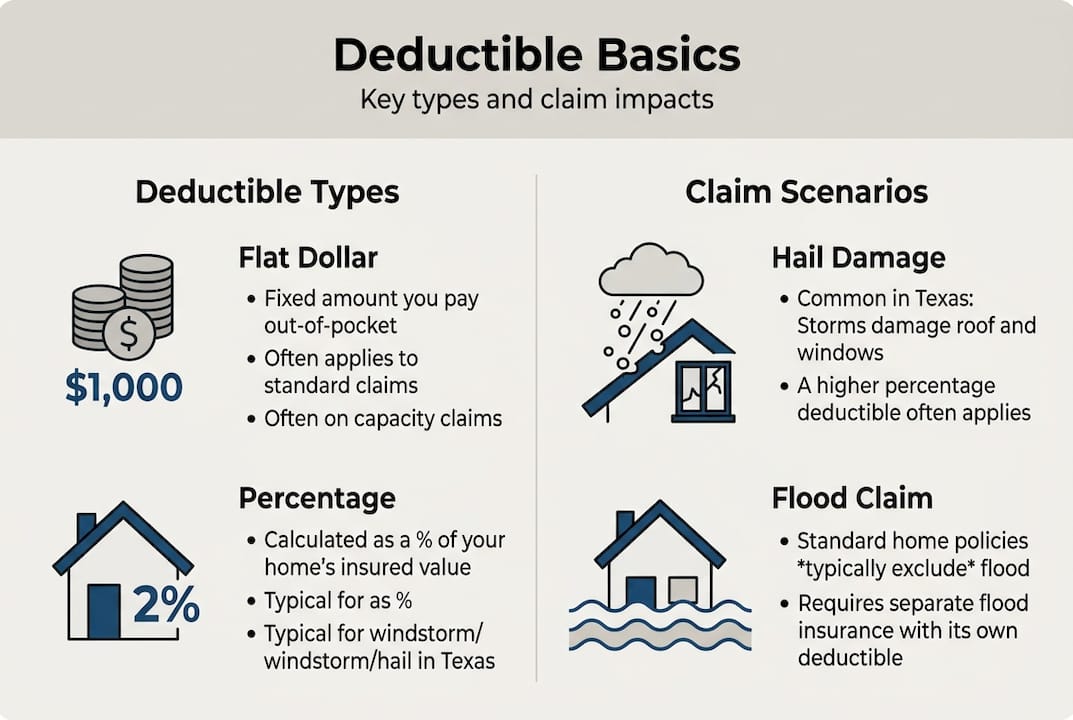

What is an insurance deductible? Understand the basics

A deductible is the amount you agree to pay out of pocket before your insurance company pays the rest of a covered claim. If a hailstorm causes $15,000 in roof damage and your deductible is $2,500, you pay $2,500 and your insurer covers $12,500. Simple in theory, but the details matter a lot in Texas.

Deductibles come in two main formats:

- Flat dollar deductibles: A fixed amount, like $1,000 or $2,500, applied to each claim regardless of your home’s value.

- Percentage-based deductibles: Calculated as a percentage of your home’s insured dwelling value. A 2% deductible on a $300,000 home equals $6,000 out of pocket.

Texas homeowners often face separate deductibles for specific perils. Hail and windstorm deductibles are common in West Texas and are almost always percentage-based. That means the higher your home value, the larger the dollar amount you’ll owe after a storm. Many homeowners don’t realize this until a claim is filed.

Flood insurance works differently. It is sold through two main channels: the National Flood Insurance Program (NFIP) and private insurers. The NFIP sets its own deductible structures and coverage caps. Texas NFIP premiums average $600 to $1,200 per year, with coastal properties exceeding $3,000 annually, while private flood options can offer higher coverage limits and shorter waiting periods but vary widely by insurer.

Here is a quick snapshot of deductible types you may encounter:

- Standard all-peril deductible: Applies to most claims like fire or theft.

- Wind and hail deductible: Separate, often percentage-based, triggered by storm events.

- Flood deductible: Tied to your NFIP or private flood policy, applied separately from your homeowners policy.

- Named storm deductible: Triggered only when a named storm causes damage.

Understanding which deductible applies to which type of damage is the first step in knowing what you’re actually covered for.

Texas Insurance Deductible Guide, Hail Flood Coverage | Hettler Insurance Agency, Lubbock Texas, phone 8067987800, address 4720 S Loop 289

How to pick the right deductible for your Texas home

Having defined what deductibles are, it’s critical to choose one that fits your budget and risk profile as a Texas homeowner. Picking a deductible is not just about lowering your monthly premium. It’s about being honest with yourself about what you can actually afford to pay after a storm.

Three factors should guide your decision:

- Your home’s insured value: A percentage deductible hits harder on higher-value homes.

- Your emergency fund: Can you actually cover a $5,000 or $8,000 out-of-pocket cost right now?

- Your regional risk: Lubbock and West Texas see frequent hail. Coastal and low-lying areas face flood exposure. Your risk profile shapes which deductibles deserve the most attention.

Here is a sample comparison to illustrate how deductible choices play out:

| Home value | Hail deductible % | Your out-of-pocket cost | Estimated annual premium savings |

|---|---|---|---|

| $250,000 | 1% | $2,500 | Baseline |

| $250,000 | 2% | $5,000 | Moderate savings |

| $350,000 | 2% | $7,000 | Moderate savings |

| $350,000 | 5% | $17,500 | Higher savings, higher risk |

.

Percentage-based hail deductibles can create surprise bills that families simply aren’t prepared for. A homeowner insurance guide for Texas recommends that families aged 28 to 42 prioritize replacement cost value (RCV) roofs and impact-resistant materials, which can earn 15% to 35% in premium discounts, and maintain an emergency fund equal to at least 2% of their dwelling value to cover hail deductible exposure.

Pro Tip: Set a calendar reminder to review your deductible every policy renewal. Home values and repair costs shift each year, and what worked two years ago may leave you underinsured today. Pairing that review with choosing a Texas insurance carrier that specializes in storm-prone regions gives you an edge.

Do not let a lower premium tempt you into a deductible you can’t realistically pay. That tradeoff only works if your savings account is ready to back it up.

How claim deductibles work for hail and flood damage

Once you’ve selected a deductible, understanding what happens when you file a claim is vital. The process is more detailed than most homeowners expect, and missing a step can slow your payout.

Here is how a typical hail claim works, step by step:

- Document the damage immediately. Take photos and video of every affected area before any repairs begin.

- File your claim promptly. Contact your insurer as soon as the storm clears. Delays can complicate your claim.

- Get an adjuster inspection. The insurer sends an adjuster to assess damage and estimate repair costs.

- Deductible is applied to the payout. If repairs total $18,000 and your hail deductible is $4,000, you receive $14,000 (minus any depreciation if you don’t have RCV coverage).

- Contractor completes repairs. Once payment is issued, you hire a licensed contractor to complete the work.

Flood claims through the NFIP follow a similar structure but with separate building and contents coverage, each carrying its own deductible. Private flood policies may combine these or offer different deductible arrangements. If you’re unsure whether your property sits in a Lubbock floodplain, that answer directly affects which flood coverage you need and what your deductible exposure looks like.

Here is a side-by-side scenario comparison:

| Scenario | Total damage | Deductible | Insurer pays |

|---|---|---|---|

| Hail damage (2% on $300K home) | $20,000 | $6,000 | $14,000 |

| NFIP flood claim | $30,000 | $2,000 | $28,000 |

| Private flood claim | $30,000 | $5,000 | $25,000 |

.

Pro Tip: Always ask your agent about deductible waivers or endorsements before storm season. Some policies offer features that limit your exposure under specific conditions. Also review whether a homeowners policy increase has changed how your deductible is calculated, especially after a home renovation or appraisal update.

Knowing flood insurance deductibles before a storm hits means you won’t be scrambling to understand the math when you’re already stressed about damage.

Savings strategies: Reduce your deductible burden

Lowering the financial blow of a deductible is possible with smart upfront moves. You don’t have to accept high out-of-pocket costs as an unavoidable part of Texas home ownership.

Here are the most effective strategies:

- Upgrade to an impact-resistant roof. This single improvement can earn you a premium discount of 15% to 35% depending on your insurer, and it directly reduces the chance of severe hail damage in the first place. Texas families who invest in impact-resistant materials see real long-term savings on both premiums and repair costs.

- Bundle your home and flood policies. Bundling policies is one of the fastest ways to lower your total insurance spend. When your homeowners and flood coverage are managed together, you often unlock better pricing and streamlined claims.

- Ask about multi-policy discounts. Multi-policy discounts are often available when you combine auto, home, and flood coverage with the same carrier or agency.

- Request a deductible waiver review. Some Texas policies include endorsements that modify or waive deductibles under certain conditions. Ask your agent to walk through every available option.

- Build and maintain a dedicated emergency fund. Size it to at least 2% of your home’s insured dwelling value. This protects you from financial hardship when a hail deductible comes due.

Pro Tip: Don’t wait until renewal to make these moves. Roof upgrades and policy changes can often be implemented mid-term, and the premium adjustment may take effect sooner than you expect. Talk to your agent now, not after the next storm rolls through.

Small decisions made before storm season can make a significant difference in what you owe after a major event.

Our take: How to approach insurance deductibles in Texas

After helping Texas families manage insurance for over 30 years, we’ve seen one mistake repeat itself: choosing a deductible based on the premium alone. A lower premium feels like a win until a hailstorm hits and the out-of-pocket bill is more than a month’s mortgage payment.

The conventional advice is to pick the highest deductible you can afford to lower your monthly costs. That advice ignores something important: Texas weather is not average. West Texas sees some of the highest hail frequency in the country. Coastal Texas faces flood exposure that most homeowners underestimate until they’re standing in water.

Families who fare best financially after major storms are the ones who treated their deductible as a savings target, not just a policy number. Impact-resistant materials that earn a 15% to 35% discount do double duty: they lower your premium and reduce storm damage severity. That’s a real, measurable outcome.

We also think it’s worth paying attention to how climate change affects insurance in Texas over time. Storm patterns are shifting. What was a low-risk zone five years ago may carry higher exposure today. Reviewing your deductible annually isn’t extra work. It’s how financially prepared Texas families stay ahead.

Get personalized insurance deductible advice for your Texas home

You’ve now got a clear picture of how deductibles work, how to pick the right one, and how to reduce your exposure before the next storm hits. The next step is making sure your current policy actually matches your needs.

At Hettler Insurance, we work with over 30 top-rated carriers to find you the right coverage at the best price. Whether you need help reviewing your hail deductible, exploring flood policy options, or understanding minimum insurance essentials for your home, our team is ready to walk you through it, no pressure, no insurance-ese. Call us or visit our site to schedule a free personalized evaluation with a local expert who knows Texas weather and Texas homes.

Frequently asked questions

What is the average deductible for hail damage in Texas?

Most Texas homeowners carry hail deductibles between 1% and 2% of their dwelling value, though some insurers set higher thresholds depending on location and property type. Maintaining an emergency fund equal to 2% of your dwelling value is a practical way to stay prepared.

Can I choose a different deductible for flood coverage in Texas?

Yes, both NFIP and private flood insurance in Texas offer several deductible options, and each choice directly affects your annual premium and claim payout. Texas NFIP premiums and deductibles vary by coverage level and property location.

How can I lower my insurance deductible costs?

Installing an impact-resistant roof, bundling your home and flood policies, and asking your agent about Texas-specific discounts are among the most effective ways to reduce your overall insurance burden. Impact-resistant materials can cut premiums by 15% to 35%.

Does my deductible change if I make multiple claims?

Your deductible is applied per claim and does not automatically increase, but filing multiple claims may prompt your insurer to re-evaluate your rates or adjust your deductible terms at renewal. Talk to your agent before filing smaller claims to understand the long-term cost impact.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: How does a percentage wind and hail deductible actually work on a Texas home?

Q2 ?: Does my Texas homeowners insurance cover flood damage?

Q3 ?: Can I lower my insurance premiums without raising my out-of-pocket risk?

Q4 ?: How much should I keep in an emergency fund to cover my deductible?

Q5 ?: How often should I review my deductibles?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com