TL;DR:

- Business interruption insurance covers lost income and ongoing expenses when a covered disaster damages your property. It does not include pandemics, power outages, or cyber attacks without specific endorsements, so reviewing policy language is essential. Effective claims depend heavily on organized financial records demonstrating actual income loss and the specific risks your Texas business faces.

Your property insurance covers the building. The equipment. The inventory. What it does not cover is the income you stop earning while all of that is being repaired. That gap catches Texas small business owners off guard every single year. Business interruption coverage pays for lost income when your business is damaged by covered events, but it carries its own exclusions for situations like epidemics or power losses that are not caused by a covered event. This guide breaks down exactly what business interruption insurance is, what it covers, what it excludes, and how to build a policy that actually fits your Texas operation.

Table of Contents

- What is business interruption insurance?

- What does business interruption insurance cover and what’s excluded?

- How business interruption insurance claims work in Texas

- Customizing your business interruption coverage: endorsements and Texas tips

- What most experts miss about business interruption insurance

- Secure your Texas business with expert insurance guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Covers lost income | Business interruption insurance replaces lost income when your operations are halted by a covered event. |

| Exclusions matter | Policies often exclude pandemics, power outages, and cyber attacks unless specifically added. |

| Proof is essential | Detailed financial records are necessary to secure a strong business interruption claim. |

| Customize coverage | Review and update your policy regularly to address emerging risks unique to Texas businesses. |

| Expert advice helps | Working with Texas-focused agents ensures your coverage fits local regulations and your real risks. |

What is business interruption insurance?

Business interruption insurance, often called BI insurance, is a type of coverage that replaces the income your business loses when a covered disaster forces you to close or scale back operations. Think of it this way: your property policy pays to fix the roof after a hailstorm. Your BI policy pays your rent, your payroll, and your loan payments while the roof is being fixed and your doors are shut.

This distinction matters enormously. A lot of Texas business owners assume that because they have a business owners policy, they are fully protected. But a business owners policy, sometimes called a BOP, bundles property and general liability coverage. Income replacement is a separate component, and it only activates after a covered property event occurs.

Here is what a standard business interruption policy is designed to cover:

- Lost net income your business would have earned during the shutdown period

- Fixed operating expenses such as rent, utilities, and lease payments that continue even when you are not open

- Payroll costs so you can retain employees during the closure

- Loan payments that keep coming due regardless of whether you are generating revenue

- Temporary relocation costs if you need to move operations to a new location while repairs are made

One critical point: BI insurance does not stand alone. It attaches to a property insurance policy and only triggers when a covered peril causes physical damage to your business property. If there is no covered property loss, there is generally no BI payout.

“Standard business interruption coverage often excludes certain disruption types unless you add specific endorsements, commonly including cyber attacks, pandemics, and losses without physical damage.”

When you are choosing a Texas insurance carrier, pay close attention to how each carrier defines a “covered peril” in their BI language. The exact wording in your policy determines everything. And make sure your business also meets any relevant Texas fire code compliance basics requirements, since fire code violations can complicate property claims and, by extension, your BI claim.

What does business interruption insurance cover and what’s excluded?

This is where most business owners get surprised, often after a loss has already happened. Covered events and excluded events are not always intuitive, and the list varies by carrier and policy. Here is a practical breakdown.

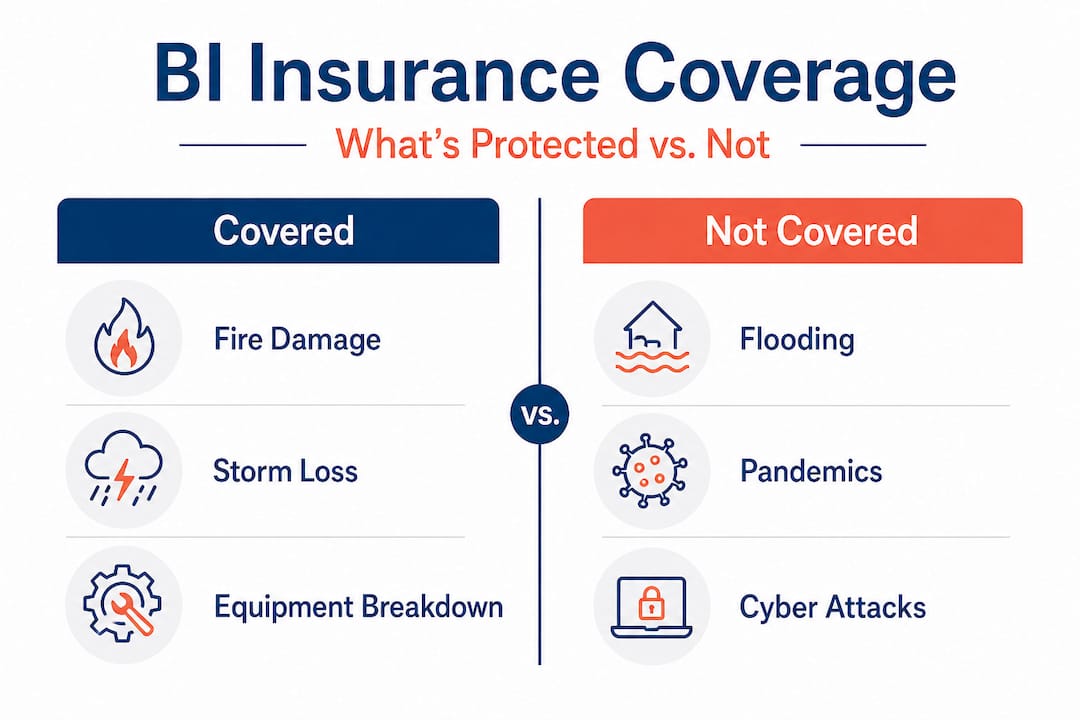

Commonly covered events:

- Fire damage that forces you to close a restaurant or retail location

- Windstorm or hail damage that destroys your roof and makes the building unusable

- Vandalism that damages your equipment and requires you to shut down

- Burst pipes or water damage from a covered cause that makes your space uninhabitable

- Explosion or structural collapse tied to a covered peril

Commonly excluded events:

- Pandemic or epidemic closures without physical property damage (a painful lesson from 2020)

- Power outages caused by a utility grid failure, not by damage to your own property

- Cyber attacks that shut down your systems but do not cause physical damage

- Flooding from outside water sources, unless you carry a separate flood policy

- Government-ordered shutdowns not tied to physical property damage at your location

Here is a direct comparison to help you see the difference clearly:

| Situation | Covered by standard BI? | Notes |

|---|---|---|

| Fire destroys your kitchen | Yes | Must be a covered peril in the property policy |

| Hailstorm damages your roof | Yes | Common Texas peril; verify coverage terms |

| COVID shutdown, no property damage | No | Pandemics typically excluded without endorsement |

| Ransomware shuts down operations | No | Requires separate cyber endorsement |

| Flood closes your retail store | No | Requires separate flood coverage |

| Burst pipe damages your office | Possibly | Depends on cause and policy wording |

.

Texas insurers follow state regulations but every policy is written differently. Reading the actual policy language, not just a summary sheet, is the only way to know what you have. If your policy contains terms you do not understand, call your agent before you need to file a claim. Not after.

Pro Tip: Review your uncommon insurance types that might fill gaps your standard BI policy leaves open. Many Texas business owners are unaware that endorsements exist specifically for utility service interruptions, supply chain failures, and civil authority orders.

It is also worth checking your current coverage for common insurance gaps that business owners overlook, particularly around workers’ compensation for owners and endorsement shortfalls. A missing endorsement that costs you a few hundred dollars a year in premium can cost you tens of thousands of dollars in an uncovered claim.

How business interruption insurance claims work in Texas

Filing a BI claim is not as simple as calling your insurance company and describing what happened. The process is evidence-heavy, and the strength of your claim depends almost entirely on the quality of your financial documentation.

Here is how the process typically works:

- Report the covered loss. Notify your insurer promptly after the covered event. Delay can complicate your claim.

- Document the property damage. BI claims require an underlying covered property loss. Photograph and document everything before cleanup begins.

- Submit financial records. This is where most claims get complicated. You will need tax returns, profit and loss statements, bank statements, and sales records going back at least 12 months.

- Demonstrate the income loss. You must show what your business would have earned during the interruption period versus what it actually earned. The insurer uses this to calculate your payout.

- Cooperate with the claims investigation. Insurers may send an adjuster or forensic accountant to review your records and verify your numbers.

Here is what that evidence requirement looks like in practice:

| Document type | Why it matters |

|---|---|

| Federal tax returns (2 years minimum) | Establishes baseline annual income |

| Monthly profit and loss statements | Shows seasonal patterns and recent trends |

| Payroll records | Supports payroll continuation claims |

| Accounts receivable records | Demonstrates revenue that was in progress |

| Fixed expense documentation | Proves ongoing costs during the shutdown |

| Lease or loan agreements | Supports expense continuation claims |

.

According to claims analysis from Insurance Journal, claim strength depends on available financial evidence and robust analysis, and disputes often turn on causation and the length of time needed for restoration.

That last point is important. Insurers do not simply pay you for however long you say the business was affected. They calculate the “period of restoration,” which is the reasonable time it would take a comparable business to get back to normal operations. If you claim 14 months but the adjuster believes the repairs should have taken 6 months, that disagreement becomes a dispute.

Pro Tip: Involve your CPA from the moment you report the loss, not just at tax time. A CPA who understands business interruption claims can organize your financial evidence in the format insurers expect, which speeds up the process and reduces the risk of disputes.

Clean bookkeeping is not just good business practice. It is your single strongest tool in a BI claim. Messy books mean lower payouts, longer delays, and in some cases, denied claims. Set up your accounting systems now, before you ever need to file.

Customizing your business interruption coverage: endorsements and Texas tips

A standard BI policy is a starting point, not a finished product. Texas businesses face a specific mix of risks, from West Texas hailstorms and tornadoes to flash flooding, ransomware attacks, and supply chain disruptions. Your policy should reflect those realities.

Here are the most important add-on endorsements to discuss with your agent:

- Cyber interruption endorsement: Covers income loss if a cyber attack or ransomware shuts down your operations, even without physical damage. Learn more about why cyber insurance for Texas businesses has become essential as attacks on small businesses increase. The current cyber insurance trends show that ransomware targeting small and mid-sized businesses is accelerating in 2026.

- Utility services interruption endorsement: Extends BI coverage to income losses caused by power, water, or gas outages originating outside your property. This matters significantly for businesses in areas with aging infrastructure.

- Civil authority endorsement: Covers income losses when a government authority prevents access to your business due to damage at a nearby property, not just your own.

- Contingent business interruption endorsement: Protects you if a key supplier or customer suffers a covered loss that disrupts your own operations, even though your property is undamaged.

- Pandemic or contagion rider: Less common and more expensive after 2020, but worth asking about. Review pandemic preparedness tips to understand how coverage gaps affected Texas businesses during the COVID era.

As the Texas Department of Insurance notes, standard business interruption coverage often excludes cyber attacks, pandemics, and losses without physical damage unless you specifically add those endorsements. Not all carriers offer the same endorsements. Some carriers that are strong on property coverage have limited endorsement options for cyber or utility interruption. This is exactly why working with an independent agency that represents multiple carriers gives you real leverage.

Pro Tip: Review your BI coverage every year, ideally before your renewal date. New threats emerge constantly. The ransomware and supply chain disruptions of 2022 and 2023 exposed gaps that most small businesses had never considered. Your 2019 policy almost certainly does not address your 2026 risk profile. Ask your agent to walk you through what has changed.

What most experts miss about business interruption insurance

Here is the honest truth that most insurance conversations gloss over: the coverage itself is only half the equation. The other half is whether you can prove your loss when it counts.

We have seen Texas business owners carry solid BI policies for years, pay their premiums faithfully, file a legitimate claim after a covered event, and still walk away with far less than they expected. Why? Because their financial records were incomplete, inconsistent, or simply not organized in a way that supported the claim calculation.

Most experts focus heavily on what the policy covers. Far fewer spend time explaining that your books are your biggest asset in a claim. A business with modest coverage and excellent records will often recover better than a business with higher limits and chaotic bookkeeping.

The second thing most people miss: exclusions cause more financial pain than any premium ever will. Reading your policy takes an afternoon. Discovering an exclusion after a catastrophic loss takes years to recover from. Negotiate your endorsement terms before you need them. Ask specifically about what is not covered and what it would cost to add it. If an endorsement feels too expensive, that is information worth having before a loss, not after.

Annual reviews are not optional if you are serious about protecting your business. Texas weather evolves. Your business evolves. Cyber threats evolve. A policy that fit your operation three years ago may have gap insurance pitfalls you are not aware of today.

The bottom line: do not trust a generic policy to cover a specific Texas business. Get advice that accounts for your location, your industry, your revenue patterns, and your actual risk exposure. That is what separates owners who recover quickly from owners who do not recover at all.

Secure your Texas business with expert insurance guidance

If this guide has made you realize your current coverage might have gaps, that is exactly the right reaction. Understanding your policy before a loss, not during one, is how you protect everything you have built.

At Hettler Insurance Agency, we have been helping Texas small business owners build smarter coverage since 1992. As an independent agency representing over 30 top-rated carriers, we do not push one company’s products. We find the right fit for your business, whether you are in Lubbock, Midland, or anywhere across Texas. Start with understanding the minimum recommended insurance every business owner should carry, then let our team review your full exposure and identify the endorsements that matter most for your specific risks. No pressure. No confusion. Just clear, expert guidance from a team that has seen what happens when coverage falls short.

Frequently asked questions

Does business interruption insurance cover pandemic-related closures in Texas?

Most Texas policies do not cover pandemic losses because standard BI coverage excludes pandemics unless you have added a specific endorsement. Always read your policy language carefully and ask your agent about available riders.

How does my business prove lost income for a BI insurance claim?

You will need organized financial records including tax returns, profit and loss statements, and sales history, because claim strength depends on financial evidence and detailed analysis to support your numbers.

Is business interruption insurance mandatory for small businesses in Texas?

It is not required by Texas law, but many commercial lenders and landlords require it as a condition of a loan or lease agreement, making it a practical necessity for most businesses.

Can I add cyber attack coverage to my business interruption policy?

Yes, cyber coverage is available as an endorsement on many policies, but BI insurance excludes cyber attacks by default, so it will not be included unless you specifically request and pay for that add-on.

How long will a business interruption claim pay benefits?

Benefits last for the reasonable period required to restore your business to normal operations, and payout duration depends on restoration evidence and the specific terms outlined in your policy.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: What does business interruption insurance actually cover for a Texas business?

Q2 ?: Does business interruption insurance cover pandemics, power outages, or ransomware attacks?

Q3 ?: How do business interruption claims work in Texas?

Q4 ?: What endorsements should Texas business owners ask about?

Q5 ?: Why is bookkeeping so important to a business interruption claim?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com