TL;DR summary:

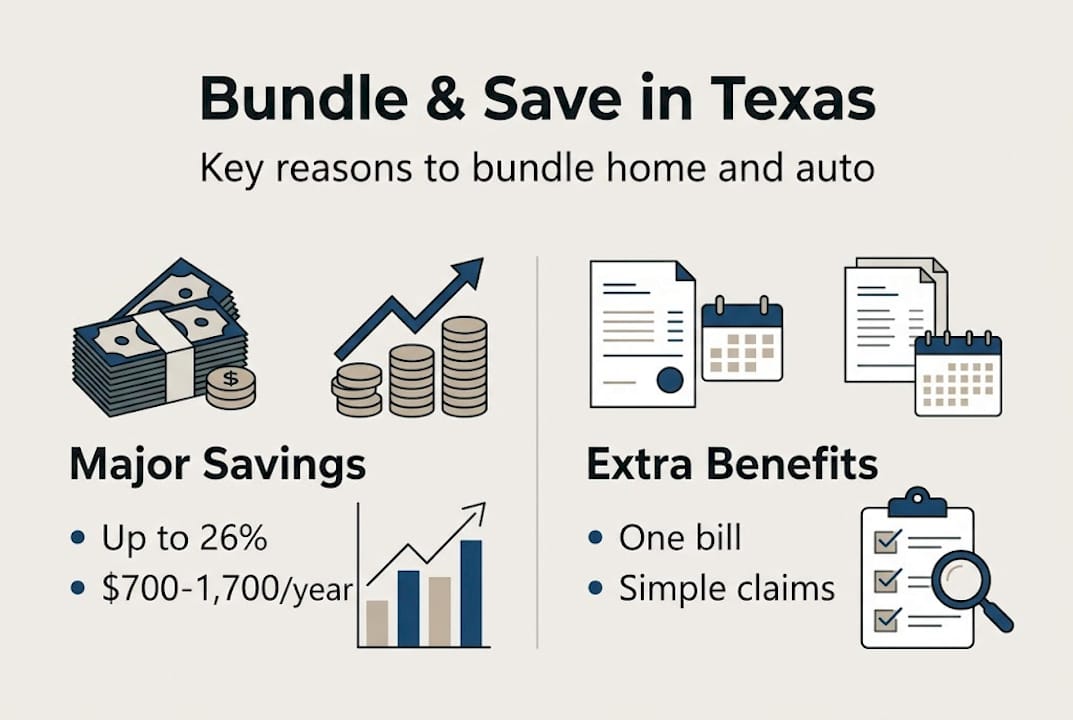

- Most Texas homeowners could save 10% to 26% annually by bundling home and auto insurance.

- Bundling offers benefits beyond savings, including simplified billing and claims processes.

- Homeowners should compare bundled and separate policies annually to ensure they get the best coverage and rates.

Most Texas homeowners between 28 and 42 are leaving real money on the table every single year. Bundling home and auto insurance typically provides multi-policy discounts of 5 to 25%, with some Texas carriers offering up to 26%. Yet a surprising number of homeowners still carry separate policies with separate insurers, pay two bills, and manage two renewal dates, often without ever comparing what a bundle would cost them. This guide breaks down exactly what bundling means, how much you can realistically save in Texas, when it makes sense, and when it does not. By the end, you will have a clear, actionable plan.

Table of Contents

- What bundling home and auto insurance really means

- How much can you save by bundling in Texas?

- Beyond price: Service, convenience, and claims in Texas

- When bundling isn’t best: Risks, edge cases, and loyalty traps

- Our take: Why smart Texas homeowners always check both options

- Get personalized bundle options with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Major savings possible | Bundling home and auto insurance in Texas can save you between 10% and 26% annually. |

| Streamlined service | Having one carrier simplifies claims, billing, and can reduce stress during Texas weather disasters. |

| Not always the best fit | In some cases, high-risk situations or specialty needs may make separate policies a smarter choice. |

| Review yearly | Always compare bundled and unbundled options each year to avoid missing better deals due to loyalty traps. |

What bundling home and auto insurance really means

Bundling simply means purchasing your homeowners policy and your auto insurance policy from the same insurance carrier. That is the core definition. You are not combining them into one policy. You still have two separate contracts with two separate sets of coverage. What changes is who issues them and how discounts get applied.

Here is how the discount structure actually works. Insurers apply the bundle discount to one or both policies as a retention incentive, meaning they want to keep your business long-term. Most commonly, the bigger discount lands on the home policy. Sometimes both policies receive a reduction. The carrier requires that both policies be active with them, but aligned renewal dates are often optional, which gives you flexibility when switching mid-term.

There are a few myths worth clearing up before you go any further.

- Myth: You sacrifice coverage for convenience. Not true. Bundling does not force you to accept lower limits or drop endorsements (add-ons that expand coverage). You can still customize each policy fully.

- Myth: You must renew both at the same time. Most carriers allow staggered renewals, so you are not locked into a rigid schedule.

- Myth: Bundling always means one phone call handles everything. Claims processes vary by carrier, so confirm the workflow before you commit.

- Myth: Only big national carriers offer bundles. Many regional Texas carriers offer competitive bundle pricing too.

The bundling advantages extend beyond price. Billing consolidates to one statement, your agent relationship deepens because they manage both lines, and renewal conversations become more productive because your advisor sees your full picture. You can also explore whether buying together makes sense for your specific situation before committing.

Pro Tip: Ask your agent to show you the itemized discount on each policy separately. Some carriers bury the savings in one line item, making it hard to see exactly where the money is going.

The bottom line on the basics: bundling is a straightforward pricing arrangement that rewards loyalty without requiring you to give anything up coverage-wise. Learn more about bundling details from carriers currently offering the strongest packages.

How much can you save by bundling in Texas?

Now for the numbers that actually matter to your wallet. Texas averages a 10 to 26% discount on bundled policies, translating to roughly $700 to $1,700 in annual savings on combined premiums averaging $6,600 per year. That is not a rounding error. That is a car payment, a vacation, or a solid emergency fund contribution.

Here is a comparison table showing how savings can vary based on your combined premium and the discount percentage a carrier offers:

| Combined annual premium | 10% discount | 18% discount | 26% discount |

|---|---|---|---|

| $5,000 | $500 saved | $900 saved | $1,300 saved |

| $6,600 | $660 saved | $1,188 saved | $1,716 saved |

| $8,000 | $800 saved | $1,440 saved | $2,080 saved |

| $10,000 | $1,000 saved | $1,800 saved | $2,600 saved |

Those numbers assume the discount applies across both policies. Even at the low end, $500 per year is meaningful. At the high end, you are looking at serious annual savings that compound over time.

So how do you gauge whether a quote is actually a good deal? Follow these steps:

- Get your current combined premium total (add home plus auto).

- Request a bundled quote from at least two or three carriers.

- Compare the bundled total against your current total, not just the percentage discount.

- Review coverage limits side by side. A lower price with weaker coverage is not a win.

- Check the carrier’s claims satisfaction ratings for Texas specifically.

One thing many young homeowners miss: the bundled savings are not always advertised upfront. You have to ask for them or work with an independent agent who shops multiple carriers at once.

You can also improve your individual savings by customizing your policy to match your actual risk profile rather than accepting default coverage levels. Higher deductibles, usage-based auto programs, and updated home valuations can all push your bundle savings even higher.

Key takeaway: Most young Texas homeowners who bundle save between $700 and $1,700 per year. If you have never compared a bundled quote against your current setup, you are likely overpaying right now.

Beyond price: Service, convenience, and claims in Texas

Saving money is just the start. Real life in Texas brings hailstorms, tornadoes, and flash floods, which makes service quality and claims simplicity just as important as the price tag.

With a bundle, you get single billing and renewal, one claims contact, and in many cases, a single deductible if a storm damages both your home and your vehicle at the same time. That last point is significant. Imagine a West Texas hailstorm that dents your car and punches holes in your roof. With separate carriers, you file two claims, deal with two adjusters, and pay two deductibles. With a bundle from one carrier, you often pay only the higher of the two deductibles and work with one team.

Here is a side-by-side comparison of the claims experience:

| Claims scenario | Single bundled carrier | Two separate carriers |

|---|---|---|

| Storm damages home and car | One adjuster, one deductible | Two adjusters, two deductibles |

| Billing after a claim | One updated statement | Two separate billing changes |

| Dispute resolution | One point of contact | Potentially conflicting processes |

| Renewal after a claim | One conversation | Two separate renewal reviews |

Texas weather and claims complexity are real concerns, especially in West Texas where hail is a near-annual event. Simplifying your claims process before a storm hits is a smart, proactive move.

Here are the convenience features to look for when evaluating a bundle:

- Mobile app access for both policies in one place

- 24/7 claims reporting by phone or app

- A dedicated local agent who knows both your home and auto coverage

- Fast response times specifically for Texas storm claims

- Digital ID cards and policy documents

Pro Tip: Before you bundle, research the carrier’s Texas-specific claims history. Picking a Texas carrier with strong storm response is more important than a slightly larger discount from a carrier with slow claims service. A 20% discount means nothing if your roof claim sits unresolved for three months.

The service and simplicity benefits of bundling are often what keep Texas homeowners with the same carrier for years. When bundling for storms is part of your decision, prioritize claims track record above all else.

When bundling isn’t best: Risks, edge cases, and loyalty traps

While bundling makes sense for most, ignoring the exceptions could cost you. Here are the main scenarios where bundling may not be your best move.

- You have a high-risk driver on your policy. Young drivers, recent DUIs, or multiple at-fault accidents can make auto insurance expensive with any carrier. Some specialty auto insurers offer better rates for high-risk policies than a bundled carrier will.

- Your home has high-risk characteristics. Older homes, homes in catastrophe zones, or properties with prior claims may be better served by a specialty home insurer that focuses on those risks.

- One carrier is simply best-in-class for one line. Sometimes the best auto insurer and the best home insurer are two different companies. Forcing a bundle sacrifices quality on one side.

- The bundle discount is smaller than the gap between carriers. If Carrier A offers a $400 bundle discount but Carrier B’s standalone auto rate is $600 cheaper, the math favors splitting.

- You have not compared recently. Rates change every year. What was the best deal two years ago may not be today.

The loyalty trap is real and worth understanding. Rate creep is the gradual increase in your premiums over time that happens when you stop shopping around. Carriers count on your inertia. They know most people will not switch once they are bundled, so they raise rates slowly, year after year, knowing you will probably stay.

Audit your bundle annually. Get separate best-rate quotes for home and auto, add them together, and compare that total to your current bundle price. If the difference is less than $50, the bundle wins on convenience. If it is more, you have a real decision to make.

This kind of annual check-up is something most homeowners skip entirely, which is a mistake. A few hours of comparison shopping every year can save you hundreds. Be cautious of insurance misunderstandings that lead you to assume your current setup is still optimal. For more on when to split policies, review this annual comparison advice before your next renewal.

Our take: Why smart Texas homeowners always check both options

After working with Texas families for over 30 years, here is our honest perspective: bundling usually wins, but not always, and assuming it does without checking is where homeowners get burned.

Texas is not a gentle insurance market. Hail, wind, and flooding put real pressure on both your home and auto coverage every single year. That means both lines of coverage matter equally. You cannot afford a weak home insurer just because their bundle discount looks attractive, and you cannot afford a slow-paying auto carrier just because they offer a good roof replacement program.

Our advice is simple. Before every renewal, get a bundled quote and get separate quotes. Compare them honestly, coverage for coverage, not just price for price. The best deal shifts over time as carriers adjust their rates and appetite for Texas risk.

Insist on carriers with proven storm service and local claims support. A carrier based in a state that rarely sees hail may not have the infrastructure to handle a West Texas hailstorm efficiently. Local knowledge matters. You can track future Texas insurance trends to stay ahead of market shifts that affect your options.

Bundling is a strong default strategy. But smart homeowners treat it as a starting point for comparison, not a final answer.

Get personalized bundle options with expert guidance

Having a knowledgeable independent agent is your shortcut to stress-free, genuinely cost-effective coverage. At Hettler Insurance Agency, we represent over 30 top-rated carriers, which means we can shop bundled and separate options at the same time and show you exactly where you stand.

We offer no-obligation consultations for Texas families who want a real comparison, not a sales pitch. Whether you are a first-time homeowner in Lubbock or a growing family in Midland, we will run the numbers both ways and give you a straight answer. Understanding your minimum coverage requirements is a good starting point, and from there we build a plan that fits your life and your budget. Visit Hettler Insurance Agency to request a quote or call us directly. Get Hettler, Get Better.

Frequently asked questions

How much can I really save by bundling home and auto insurance in Texas?

Most Texas homeowners save between 10% and 26%, which equals roughly $700 to $1,700 per year on average combined premiums.

Does bundling affect my coverage or just my price?

Bundling can also simplify claims and billing, but always review your coverage details carefully to make sure no gaps appear when switching to a single carrier.

Is it ever better not to bundle my home and auto insurance?

Yes. If you have high-risk factors like young drivers, older homes, or properties in catastrophe zones, separate policies may offer better rates or stronger coverage than any bundle.

What is the main convenience of bundling for claims in Texas?

A bundled policy lets you work with one claims adjuster and often pay only the higher deductible when a single event, like a hailstorm, damages both your home and your vehicle.

Recommended

———————

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) with over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local Independent insurance agency representing multiple carriers. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.)

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: How much can I realistically save by bundling home and auto insurance in Texas?

Q2 ?: Does bundling mean I have to compromise on coverage limits or endorsements?

Q3 ?: What happens with deductibles when a storm damages my home AND my car?

Q4 ?: When does bundling NOT make sense?

Q5 ?: How often should I re-shop my bundle?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com