TL;DR:

- Personal property coverage protects belongings but is often misunderstood and can have limits.

- Texas weather risks make understanding exclusions like flood and earthquake coverage essential.

- Regular policy reviews and proper documentation improve claim success and coverage adequacy.

Most Texas homeowners assume their insurance policy covers everything under their roof. That assumption can be costly. Your homeowners policy is actually divided into separate sections, and the part that protects your belongings, called personal property coverage, has its own rules, limits, and exclusions you need to understand. In Texas, where hail storms, tornadoes, and high winds are regular threats, the gap between what you think is covered and what actually is can add up to thousands of dollars in out-of-pocket losses. This guide walks you through what personal property coverage is, what it includes, how it differs from dwelling coverage, and how to file a claim the right way.

Table of Contents

- Defining personal property coverage for Texas homeowners

- What does personal property coverage include and exclude?

- Personal property coverage vs. dwelling coverage: Key differences

- How to file a personal property claim and maximize your coverage

- What most Texas homeowners overlook about personal property coverage

- Get expert help optimizing your property coverage

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Covers your belongings | Personal property coverage protects items like furniture, electronics, and clothing in and around your Texas home. |

| Know exclusions | Typical policies exclude flood and earthquake damage, with special limits for valuables like jewelry and collectibles. |

| Documentation matters | Keeping an updated home inventory and clear records can speed up claims and avoid disputes. |

| Adjust for Texas risks | Review your coverage to match regional threats like hail or tornadoes, and consider endorsements for high-value items. |

Defining personal property coverage for Texas homeowners

Personal property coverage is the section of your homeowners or renters insurance policy that protects your physical belongings. Think furniture, electronics, clothing, appliances, and everyday items you own. It does not protect the physical structure of your house. That is a separate section called dwelling coverage. Understanding this distinction upfront saves you from major surprises when you file a claim.

What homeowners insurance covers is broader than many people realize, but it is also more specific than most assume. Personal property is covered beyond the physical structure of your home, meaning your TV, your couch, and your kids’ laptops all fall under this section. But each item has a coverage limit, and certain categories have special sub-limits that can leave you underinsured if you are not careful.

For Texas homeowners specifically, this coverage matters more than in many other states. Texas ranks among the top states for severe weather events, including hail damage and tornado activity. A single hail storm in Lubbock or a windstorm in the DFW suburbs can break windows, scatter belongings, and destroy electronics or furniture left in exposed areas of your home.

Here is what personal property coverage typically protects:

- Electronics: Televisions, laptops, tablets, gaming systems

- Furniture: Sofas, beds, dining sets, home office equipment

- Clothing and footwear: Wardrobes for all family members

- Appliances: Washers, dryers, refrigerators (not permanently installed)

- Sports equipment and tools: Bicycles, golf clubs, power tools

- Kitchen items: Dishes, cookware, small appliances

If you rent your home, renters insurance basics explain why this coverage is just as critical for you. Your landlord’s policy covers the building, not your stuff. According to Texas insurance consumer rights, policyholders have the right to a clear explanation of their coverage. Read your declarations page carefully and ask your agent to walk you through your personal property limits.

Statistic to know: The average U.S. household owns between $20,000 and $30,000 worth of personal belongings. Many homeowners are insured for far less.

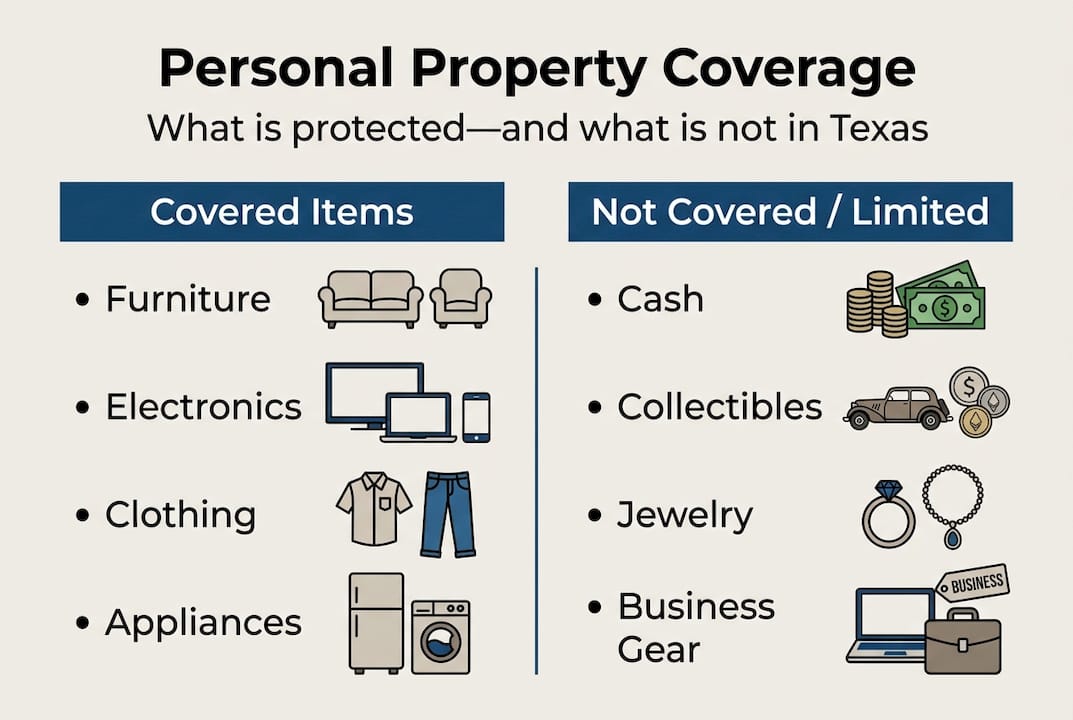

What does personal property coverage include and exclude?

Not everything you own is protected equally under a standard policy. Knowing the boundaries of your coverage helps you avoid filing a claim only to find out the item was excluded or only partially reimbursed.

Here is a quick comparison of what is typically covered versus what is not:

| Covered items | Not covered or limited |

|---|---|

| Furniture and electronics | Cash and gift cards |

| Clothing and footwear | Jewelry above sub-limit (often $1,500) |

| Appliances (non-built-in) | Fine art above sub-limit |

| Sports equipment | Business property kept at home |

| Bicycles (often with limits) | Flood or earthquake damage |

| Kitchen items | Normal wear and tear |

Texas weather risks make the exclusion column especially important. Flood damage from heavy rains is excluded from standard policies. Standard policy coverage confirms that earthquake and flood losses require separate policies entirely. If you live in a flood-prone area near the DFW metroplex or along a creek in West Texas, this is a gap you cannot afford to ignore.

Jewelry, collectibles, and cash often have low special coverage limits, sometimes as low as $200 for cash and $1,500 for jewelry. If your engagement ring or coin collection is worth more than those amounts, your standard policy will not make you whole after a theft or fire.

Business property is another commonly overlooked exclusion. If you work from home and have expensive equipment like a professional camera, a high-end computer setup, or product inventory, your personal policy likely limits that coverage significantly. Check your coverage limits and exclusions before assuming your home office is fully protected.

Pro Tip: Ask your agent about endorsements or floaters. A floater is an add-on to your policy that provides dedicated coverage for specific high-value items like jewelry, musical instruments, or fine art. It is usually affordable and closes a real gap.

Personal property coverage vs. dwelling coverage: Key differences

Homeowners insurance is not a single blanket policy. It is a set of coverage types bundled together, and two of the most important are personal property coverage and dwelling coverage. Knowing which covers what helps you file the right claim and avoid denial.

Home structure and personal items are covered under different sections of a policy. Here is how to think about it in practical terms:

- A tornado damages your roof. That is a dwelling coverage claim.

- That same tornado sends debris through your window and destroys your TV. That is a personal property claim.

- A burglar breaks your back door and steals your laptop. The door repair is dwelling. The laptop is personal property.

- Hail cracks your siding. Dwelling coverage handles that.

- Hail breaks a skylight and ruins your sofa beneath it. Sofa replacement falls under personal property.

| Coverage type | What it protects | Typical claim example | Common payout limit |

|---|---|---|---|

| Dwelling | Walls, roof, floors, built-in fixtures | Tornado roof damage | Based on rebuild cost |

| Personal property | Movable belongings you own | Stolen electronics | 50-70% of dwelling limit |

| Other structures | Garage, fence, shed | Hail-damaged fence | 10% of dwelling limit |

“Understanding the difference between your dwelling and personal property coverage can be the deciding factor in whether your claim is approved or denied.” This is especially true for first-time homeowners who often assume one policy covers all losses equally.

If you are investing in real estate or renovating a property, the same principle applies. Coverage for house flippers works differently from standard homeowner policies and requires careful review. Your Texas policyholder rights guarantee access to a clear policy explanation. Use that right.

How to file a personal property claim and maximize your coverage

Knowing how to file a claim correctly is just as important as having the right coverage. A poorly documented claim often results in a lower payout or outright denial. Follow these steps when something goes wrong.

- Secure the area and prevent further damage. Do not throw away damaged items yet. Your insurer will need to inspect them.

- Document everything immediately. Take photos and videos of all damage before moving or cleaning anything.

- Make a list of damaged or missing items. Include brand names, model numbers, approximate age, and estimated value.

- Locate receipts or proof of purchase. Bank statements, emails, and credit card records all count as documentation.

- Contact your insurance agent. Report the claim as soon as possible. Delayed reporting can create complications.

- Request a written summary of your claim status. Keep records of all conversations with your insurer.

Proper documentation is the single most important factor in a successful claim. Timely and complete records help ensure a successful outcome. The National Association of Insurance Commissioners provides consumer claim guides you can reference for additional support.

Pro Tip: Create a home inventory today and store it in the cloud or email it to yourself. Walk through every room with your phone camera and narrate what you own. Update this inventory every time you make a major purchase. This alone can significantly increase your payout after a loss.

Common mistakes Texas homeowners make when filing claims:

- Waiting too long to report. Most policies require prompt notice.

- Throwing away damaged items. Insurers often want to inspect them.

- Underestimating item values. Use replacement cost, not what you paid years ago.

- Not asking about additional living expenses. If your home is uninhabitable, this coverage pays for temporary housing.

What most Texas homeowners overlook about personal property coverage

Here is what we see regularly at Hettler Insurance: homeowners who have had the same policy for 10 years without ever reviewing it. Their family has grown, they have bought new furniture, replaced appliances, and accumulated electronics, but their personal property limit has not changed. That is a serious problem.

Texas families face a specific set of risks that most national policy templates are not built to address perfectly. Hail, wind, and the occasional tornado are not hypothetical. They happen every year, sometimes every season. Your coverage should reflect where you actually live.

Annual policy reviews are not optional. They are how you find coverage gaps before a storm does. We also find that working with an independent agent, rather than a single-carrier agent, gives you the ability to find the right coverage limit across multiple carriers. That flexibility often leads to better coverage at a lower premium. You get real choices, not just one company’s options.

Do not wait for a claim to find out your policy is not enough.

Get expert help optimizing your property coverage

You now understand what personal property coverage is, how it works, and where the gaps tend to hide. The next step is making sure your actual policy reflects that knowledge.

At Hettler Insurance Agency, our team of independent agents works with over 30 top-rated carriers to find coverage that fits your life and your budget. We serve homeowners across Lubbock, DFW, and all of Texas. Whether you need a full policy review, help understanding your insurance minimums, or a quote that actually competes, we are ready to help. There is no pressure and no extra fee. Call us or reach out online to schedule your free consultation. Get Hettler, Get Better.

Frequently asked questions

Does personal property coverage protect items outside my home?

Personal property coverage often extends to belongings stored off-premises, such as items in a storage unit or at a college dorm, but coverage limits for off-site items are typically lower than for belongings inside your home.

Is water damage from storms or floods in Texas covered by personal property insurance?

Standard homeowners policies exclude flood damage, so a separate flood insurance policy is required for Texas weather risks. Some water damage, such as from a burst pipe, may be covered depending on the source.

How much personal property coverage do I need?

Experts recommend conducting a complete home inventory first, then choosing a limit that reflects the full replacement value of your belongings. A home inventory is the most accurate way to set the right coverage amount.

Are high-value items like jewelry or collectibles fully covered?

No. Jewelry and collectibles are subject to special sub-limits under a standard policy, often far below their actual value. Adding an endorsement or floater is the correct way to close that gap.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: Does personal property coverage protect items outside my Texas home?

Q2 ?: Is water damage from storms or floods in Texas covered by personal property insurance?

Q3 ?: How much personal property coverage do I really need?

Q4 ?: Are high-value items like jewelry or collectibles fully covered?

Q5 ?: How is personal property coverage different from dwelling coverage?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com