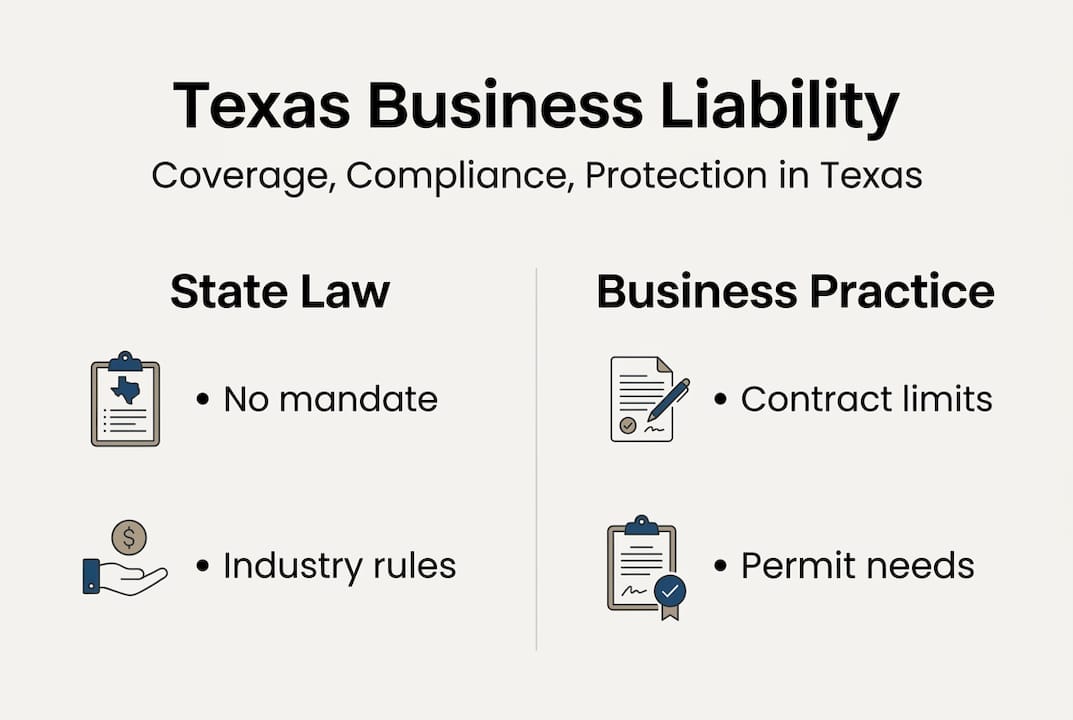

Many Texas small business owners assume they are legally required to carry general liability insurance. That assumption is understandable, but it is not entirely accurate. Texas state law does not mandate general liability for most small businesses, yet operating without it can still expose you to serious financial risk. The gap between what the law requires and what clients, landlords, and permits demand is where most business owners get caught off guard. This guide walks you through what liability coverage actually means, who genuinely needs it in Texas, and how to stay compliant without overpaying or underprotecting your business.

Table of Contents

- What is business liability insurance?

- Texas liability laws versus business reality

- Who must have liability coverage in Texas?

- How Texas businesses stay compliant

- Special considerations: Industry edge cases and exceptions

- Work with an independent agent who knows Texas business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| No universal mandate | Texas does not legally require general liability insurance for all businesses. |

| Industry-specific rules | Certain sectors and contracts require liability coverage to operate or get permits. |

| Client-driven enforcement | Most enforcement comes from clients, landlords, and government contracts, not state law. |

| Coverage protects assets | Liability insurance can save you from paying lawsuits and claims from business accidents. |

| Compliance is ongoing | Staying compliant means updating documents and understanding contract requirements. |

.

What is business liability insurance?

Business liability insurance is a policy that pays for legal costs, settlements, and damages when your business is held responsible for injuring someone, damaging their property, or causing financial harm. It exists because lawsuits happen, even to careful, well-run businesses. One slip-and-fall at your storefront, one client who claims your work caused them a loss, and you are looking at legal bills that can drain your business account fast.

There are several types of liability coverage worth knowing:

- General liability insurance: Covers bodily injury, property damage, and personal injury claims like defamation or false advertising.

- Professional liability insurance: Also called errors and omissions (E&O), this covers claims that your professional advice or service caused a financial loss.

- Product liability insurance: Protects manufacturers, distributors, and retailers if a product causes harm.

- Specialized liability policies: These include garage liability, cyber liability, and liquor liability, each designed for specific industries.

Typical covered incidents include a customer tripping in your office, a contractor accidentally damaging a client’s property, or a social media post that leads to a defamation claim. The Texas Department of Insurance provides guidance on what commercial liability policies must cover under Texas law.

Important: Liability insurance is often contractually required by clients, landlords, and government entities in Texas, even when state law does not mandate it.

When you are choosing a Texas insurance carrier, understanding which type of liability coverage fits your specific business operations is the first step toward real protection.

Texas liability laws versus business reality

With an understanding of what liability coverage offers, it is vital to separate what Texas law says from what actually gets enforced in real-world business. The distinction matters because confusing the two can leave you either over-insured or dangerously exposed.

From a legal standpoint, Texas does not have a universal liability insurance mandate for small businesses. General liability is not required by state law but is commonly required by contract. That means the state will not fine you for lacking a policy, but your clients, landlords, and project owners absolutely can refuse to work with you without one.

Here is how the two realities compare:

The financial risk of going without coverage is real. Lawsuit costs can exceed $50,000 even for small claims, and that figure does not include lost time, damaged reputation, or the cost of hiring legal counsel. You pay every dollar out of pocket without a policy in place.

You can review state insurance rules directly through TDI to understand what oversight exists at the regulatory level. But do not rely on state minimums alone to guide your coverage decisions.

Pro Tip: Always confirm with project owners or clients what insurance proofs are needed before you sign any contract. Ask for the specific coverage type, limit amount, and any endorsements they require in writing.

For a closer look at how Texas business insurance requirements apply across different industries, reviewing your specific sector’s norms is a smart starting point.

| Scenario | State law requirement | Contract or permit requirement |

|---|---|---|

| General contractor | Not required by state | Almost always required by clients |

| Retail storefront | Not required by state | Often required by commercial landlords |

| Food truck operator | Not required by state | Required for most city permits |

| Daycare provider | Required by state | Required by parents and licensing boards |

| IT consultant | Not required by state | Frequently required by corporate clients |

| Plumber | Required in some municipalities | Required by most general contractors |

Who must have liability coverage in Texas?

So, which businesses actually must show proof of liability in Texas, and what counts as required? The answer depends on your industry, your clients, and whether you work on public or government projects.

Some industries carry statutory or regulatory insurance requirements in Texas:

- Construction and general contracting: Most municipalities and general contractors require proof of liability before work begins.

- Electrical and HVAC contractors: Licensing boards and project owners routinely require coverage.

- Plumbing: Specific industries in Texas such as construction and plumbing have liability mandates tied to licensing.

- Daycare and childcare providers: State licensing requires liability coverage as a condition of operation.

- Oil and gas contractors: Operators and project owners require liability coverage, often at high limits.

- Event vendors and food trucks: City permits in Lubbock and other Texas municipalities require proof of insurance.

When it comes to permit and government contract requirements, the numbers get specific. Permit limit requirements usually range from $500,000 to $2 million depending on the project type and the issuing authority. A city sidewalk repair contract will look very different from a state highway project in terms of required limits.

Edge cases exist too. A freelance graphic designer working from home may never face a liability requirement. A sole proprietor doing occasional handyman work may only need coverage when bidding on a specific job. Voluntary coverage in these cases still makes financial sense, even without a mandate.

| Industry | Requirement type | Typical minimum limit |

|---|---|---|

| General contractor | Contract and permit | $1,000,000 per occurrence |

| Daycare provider | Statutory | $300,000 minimum |

| Oil and gas contractor | Contract | $1,000,000 to $2,000,000 |

| Food truck operator | Municipal permit | $500,000 |

| IT consultant | Contract only | Varies by client |

| Retail business | Landlord contract | $1,000,000 general aggregate |

How Texas businesses stay compliant

Once you identify if your business falls into a required category, maintaining compliance is the next step. Compliance is not just about having a policy. It is about having the right documentation ready when it is needed.

Here are the key compliance steps every Texas small business owner should follow:

- Obtain a Certificate of Insurance (COI). A COI is a one-page document that summarizes your coverage. Clients, landlords, and permit offices will ask for this. Your insurer provides it at no charge.

- Add additional insureds when required. An additional insured is a person or organization added to your policy who also receives protection. Many contracts require this before work begins.

- Include waivers of subrogation when requested. This endorsement prevents your insurer from pursuing a third party for reimbursement after paying a claim, which some clients require.

- Review your policy limits annually. Business growth, new contracts, and changing permit requirements can all affect how much coverage you need.

- Track COI expiration dates. An expired COI can halt a project or void a contract. Set calendar reminders 60 days before renewal.

- Confirm municipal requirements before applying for permits. Each city in Texas may have different insurance requirements for the same type of work.

Key compliance practices include providing Certificates of Insurance, adding additional insureds, and meeting municipal requirements. TDI oversees insurer conduct and policy fairness in Texas, but it does not set minimum liability limits for most private contracts.

Common pitfalls include forgetting to update COIs after a policy renewal, missing permit deadlines because coverage lapsed, and failing to add the correct additional insured language. These mistakes can cost you a contract or delay a project by weeks.

Pro Tip: Always check for unique insurance wording in contracts with local governments or major clients. Some require specific endorsements or policy language that a standard policy may not include. Call your agent before you sign.

You can review TDI compliance requirements directly to understand what the state expects from insurers and policyholders alike.

Special considerations: Industry edge cases and exceptions

Even after following the standard rules, there are industry-specific quirks and pitfalls every business owner should know about in Texas. Some of these can affect whether your coverage actually pays out when you need it most.

Texas Anti-Indemnity Act: This law limits how broadly one party can shift liability to another in construction contracts. Contracts in construction may be limited by the Texas Anti-Indemnity Act, which means a contract clause requiring you to cover another party’s negligence may not be enforceable. Know this before you agree to broad indemnification language.

Premises liability: If someone is injured on your property, Texas law distinguishes between what you actually knew about a hazard and what you should have known. This is the actual versus constructive knowledge standard. Premises liability clarification from Texas courts has reinforced that business owners must actively inspect and address hazards, not just react after an incident.

OSHA multi-employer policies: On job sites with multiple contractors, OSHA can hold more than one employer responsible for a safety violation. This creates overlapping liability exposures that a standard general liability policy may not fully address without specific endorsements.

Mechanics and auto repair shops: This is a category with unique exposure. Consider these specific risks:

- Misdiagnosis or faulty repair leading to a vehicle accident

- Damage to a customer’s vehicle while in your custody

- Deceptive trade practice claims under Texas law

- Test drives that result in accidents

Mechanics and garages must consider garage liability for custody of vehicles, with commercial auto required for business use. A standard general liability policy does not cover vehicles in your care. You need a garage liability policy specifically.

If your shop uses vehicles for business purposes, reviewing Texas auto insurance limits is a necessary step. And if you are in the auto repair space, understanding auto repair shop insurance options specific to Texas will help you avoid gaps in coverage that could be financially devastating.

Key takeaway: Industry-specific policies exist for a reason. A one-size-fits-all general liability policy may leave critical gaps depending on what your business actually does.

Work with an independent agent who knows Texas business

Navigating liability coverage in Texas is not a one-time task. Your coverage needs change as your business grows, takes on new clients, or enters new industries. Getting the right policy from the start, and keeping it current, is where an experienced independent agent makes a real difference.

At Hettler Insurance Agency, we have been helping Texas small business owners find the right commercial coverage since 1992. As an independent agency based in Lubbock, we represent over 30 top-rated carriers, which means we shop the market for you and find coverage that fits your industry, your contracts, and your budget. Ron Hettler and Meghan Hettler are both Certified Insurance Counselors (CIC), the gold standard credential in the industry, and they bring that expertise directly to your coverage review. Whether you need a general liability policy, a business owners policy, workers’ compensation, or a specialized garage liability plan, we can help. Call us or visit hettlerinsurance.com to get started today.

Frequently asked questions

Is general liability insurance required for all Texas businesses?

No, state law does not mandate general liability insurance for most small businesses, but certain industries and contracts may require it as a condition of doing business.

Who enforces business liability insurance in Texas?

Most enforcement comes from clients, landlords, and regulatory agencies through contract terms. Insurance is often contractually required by clients or for permits rather than mandated by state law.

What are the risks of having no liability coverage?

Businesses without liability insurance must pay out-of-pocket for lawsuits and claims. Lawsuit costs can exceed $50,000 even for small claims, not counting attorney fees or lost business.

Are there coverage minimums for Texas business liability insurance?

Permits and contracts often require limits ranging from $500,000 to $2 million. Permit requirements vary by industry and issuing authority, so always confirm the specific limit before applying.

Do auto repair shops in Texas need special business liability insurance?

Yes, garage liability insurance is essential for shops that handle customer vehicles, and commercial auto coverage is required for any vehicle used for business purposes.

Recommended

- Choosing a Texas Insurance Carrier | Hettler Insurance Agency

- Should You Add Windshield Coverage to Your Auto Policy in West Texas? – Hettler Insurance Agency

- Auto Insurance Limits In Plainview Texas – Hettler Insurance Agency

- Darwinian Insurance Underwriting = Extinct Dog Breeds? – Hettler Insurance Agency

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: Is general liability insurance required for all Texas businesses?

Q2 ?: Who actually enforces business liability insurance in Texas?

Q3 ?: What are the real-world risks of operating without liability coverage?

Q4 ?: What coverage limits do Texas permits and contracts typically require?

Q5 ?: Do Texas auto repair shops need a special kind of business liability insurance?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com