TL;DR summary:

- Texas restaurants face significant risks from slips, fires, and liquor liability that require proper insurance coverage. Many owners underestimate the importance of comprehensive policies beyond minimum legal requirements to protect against costly claims. Working with an experienced broker and regularly reviewing coverage is essential for full protection.

Running a restaurant in Texas means managing kitchen chaos, staffing challenges, and razor-thin margins every single day. What many owners underestimate is that a single insurance claim can cost far more than a bad week of sales. Restaurants average $9,000 per insurance claim, with slip-and-falls and fires carrying especially high payouts. In Texas, the stakes are even higher because regional weather, liquor liability laws, and lease requirements create a layered set of exposures most owners don’t fully see until something goes wrong. This guide walks you through every coverage type, common pitfalls, and a step-by-step approach to building a plan that actually protects your business.

Table of Contents

- Understanding insurance risks and requirements in Texas

- Types of insurance every Texas restaurant should consider

- How to build your Texas restaurant insurance plan

- Common gaps, exclusions, and mistakes to avoid

- Why most Texas restaurants miss out on full protection

- Connect with Texas restaurant insurance specialists

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Major risks and claims | Slip-and-falls, fires, and employee injuries are the most frequent and costly claims for Texas restaurants. |

| Essential coverage types | General liability, workers’ comp, liquor liability, property, and specialty endorsements are vital for robust protection. |

| Regional nuances matter | Gulf Coast restaurants need windstorm and flood coverage; urban and alcohol-serving venues require extra liability. |

| Checklist for building your plan | Evaluate risks, gather quotes from Texas carriers, and review policies for hidden exclusions and gaps. |

| Avoid common mistakes | Undervaluing property, missing endorsements, or neglecting flood/windstorm exclusions can leave you exposed. |

.

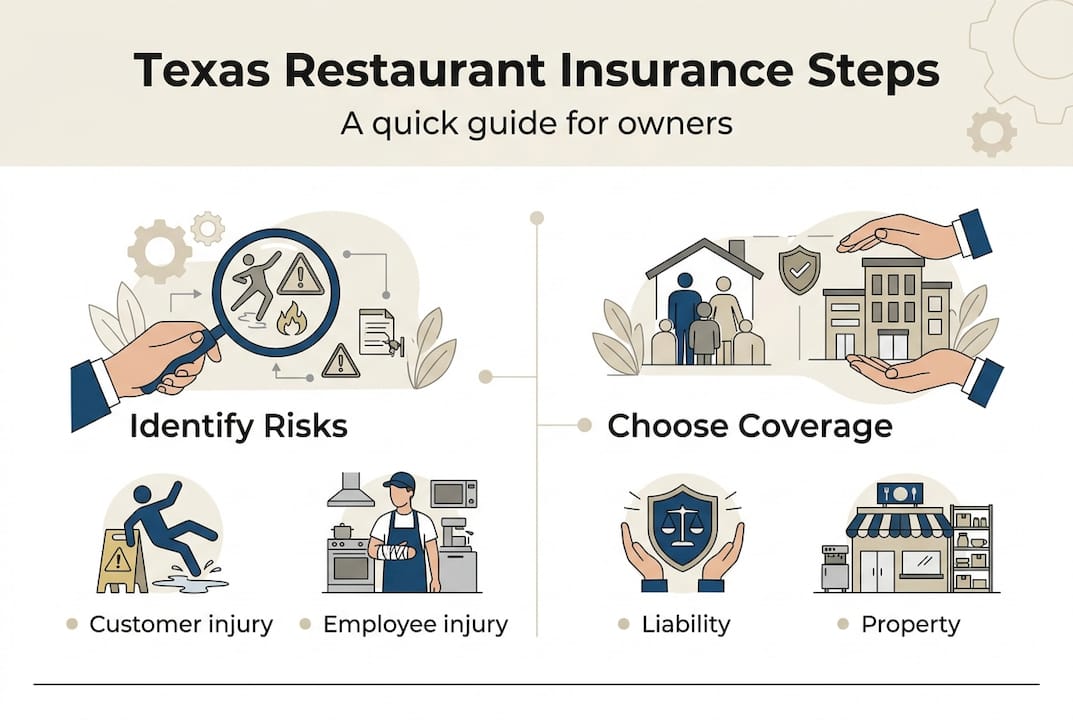

Understanding insurance risks and requirements in Texas

Texas restaurants face a specific set of risks that go well beyond what most owners initially plan for. The most frequent claims involve slip-and-fall injuries on wet floors, kitchen fires, equipment breakdowns, and employee injuries. Each of these can trigger a claim that shuts your doors for days or weeks while costs pile up fast.

Here is a quick look at the top risk categories for Texas restaurants:

- Slip-and-fall injuries: One of the most common liability claims, especially in high-traffic dining areas and commercial kitchens

- Fire damage: Grease fires and electrical failures are leading causes of property loss in food service businesses

- Equipment breakdown: A failed walk-in cooler or commercial oven can mean thousands in spoiled inventory and lost revenue

- Employee injuries: Burns, cuts, and repetitive strain injuries are routine in restaurant environments

- Liquor liability: If you serve alcohol, you face exposure under Texas’s Dram Shop laws, which hold establishments liable for damages caused by intoxicated patrons

From a regulatory standpoint, Texas has minimal insurance mandates compared to many other states. There is no statewide requirement for general liability or commercial property insurance for restaurants. However, that does not mean you can skip coverage. Landlords routinely require proof of liability insurance in lease agreements. The Texas Alcoholic Beverage Commission (TABC) strongly encourages liquor liability coverage for establishments serving alcohol. Lenders and franchise agreements often demand specific coverage limits as well.

The practical reality is that your legal minimum and your actual protection needs are two very different numbers. Choosing the right Texas insurance carriers matters because not every carrier understands the specific exposures of a food service business in this state. Working with an independent agent who knows Texas restaurants gives you a meaningful advantage when it comes to matching coverage to your actual risk profile.

Types of insurance every Texas restaurant should consider

Now that you know what risks the state recognizes, let’s break down the exact types of insurance you should evaluate, plus what each policy typically covers.

| Coverage type | Average annual cost | What it covers |

|---|---|---|

| General liability | $500 to $1,500/yr | Slip-and-falls, food-related illness, third-party property damage |

| Workers’ compensation | ~$22/mo per employee | Employee injuries, medical costs, lost wages |

| Business owner’s policy (BOP) | ~$73/mo | Bundles general liability and commercial property |

| Liquor liability | $800 to $2,000/yr | Claims tied to alcohol service under TABC rules |

| Commercial property | Varies by location | Building, equipment, inventory (excludes flood/wind in some areas) |

| Cyber liability | $500 to $1,500/yr | Data breaches, POS system attacks, customer data exposure |

| Business interruption | Included in BOP or added separately | Lost income during covered closures |

| Food spoilage/contamination | Endorsement, varies | Spoiled inventory, recall costs |

.

Key coverage types for Texas restaurants include general liability, workers’ comp, BOP, liquor liability, commercial property, auto, cyber, spoilage, and interruption. Each one addresses a different slice of your total risk.

A Business Owner’s Policy (BOP) is often the smartest starting point for smaller restaurants. It bundles general liability and commercial property into one policy, usually at a lower combined rate than buying each separately. Think of it as a foundation you build on with endorsements (add-ons that expand coverage for specific risks).

Liquor liability deserves special attention. If your restaurant serves beer, wine, or spirits, Texas’s Dram Shop Act creates real legal exposure. A patron who leaves your establishment intoxicated and causes an accident can result in a lawsuit naming your business. This coverage is not optional if you hold a TABC permit.

Pro Tip: If you use delivery drivers, commercial auto coverage is critical. Personal auto policies almost always exclude business use, meaning a driver in an accident while delivering orders could leave your business exposed.

When you are protecting your business finances, the goal is not to buy every policy available. It is to identify which risks are most likely and most costly for your specific operation, then fill those gaps first.

How to build your Texas restaurant insurance plan

With an overview of each coverage, let’s show exactly how to map your risks to the right protection using a proven step-by-step approach.

Step 1: Gather your business information

Before you contact any agent or carrier, pull together the following:

- Square footage and construction type of your building

- Estimated value of equipment, furniture, and inventory

- Number of employees and their roles

- Whether you serve alcohol and your TABC permit type

- Any delivery vehicles owned or used by employees

- Your lease agreement (look for insurance requirements from your landlord)

Step 2: Get multiple quotes from Texas carriers

Never accept the first quote you receive. Rates vary significantly between carriers for the same coverage. An independent agent can shop your risk across multiple insurers and present real comparisons. This is especially important in Texas, where regional nuances and cost factors like Gulf Coast flood exposure, Dallas-area hail and tornado risk, and TABC liquor liability requirements all affect pricing.

Step 3: Map your coverage to your specific risks

| Your risk | Coverage needed |

|---|---|

| Customer injuries on premises | General liability |

| Employee injuries | Workers’ compensation |

| Kitchen fire or equipment loss | Commercial property or BOP |

| Alcohol service claims | Liquor liability |

| Delivery operations | Commercial auto |

| Power outage and spoiled food | Food spoilage endorsement |

| Cyber attack on POS system | Cyber liability |

.

Step 4: Review limits, exclusions, and endorsements

Pay close attention to your policy limits (the maximum the insurer will pay per claim) and exclusions (what is not covered). Ask your agent specifically about open carry and business insurance implications and whether terrorism insurance in Texas applies to your location.

Pro Tip: Update your property valuations every year. Undervaluing your building or equipment can trigger a coinsurance penalty, meaning the insurer pays only a fraction of your claim even if you have coverage.

Common gaps, exclusions, and mistakes to avoid

Even with a solid plan, hidden exclusions or overlooked gaps can be costly. Here are the most common mistakes Texas restaurant owners make and how to avoid them.

Flood and windstorm exclusions

Standard commercial property policies in Texas almost always exclude flood and windstorm damage. If your restaurant is near the Gulf Coast or in a flood-prone area, you need separate coverage. Floods and wind are excluded in coastal Texas, meaning separate FEMA or Texas Windstorm Insurance Association (TWIA) policies are required. Do not assume your property policy covers a hurricane or flash flood.

Business interruption limits

Business interruption insurance (which replaces lost income while your restaurant is closed for a covered event) has a restoration period limit. Most policies cover 12 months of lost income, but rebuilding after a major fire can take longer. Review this limit carefully and ask about extended period endorsements.

Food contamination and recall

A norovirus outbreak or a supplier recall can shut you down for days and generate significant liability. Standard policies often exclude food contamination and recall costs. You need a specific endorsement to cover this exposure, and it is one of the most overlooked gaps in restaurant insurance.

Critical reminder: If you skip the food contamination endorsement and a health department closure costs you $30,000 in lost revenue and legal fees, your standard policy will not pay a cent of it. Ask your agent about this endorsement before you assume you are covered.

Here are additional gaps to watch for:

- Cyber and data breach: POS systems are frequent targets; a breach exposing customer payment data can trigger costly notifications and lawsuits

- Off-premises delivery: Drivers using personal vehicles for delivery are often not covered under your commercial auto or general liability policy

- Employee dishonesty: Theft by employees is a real risk in cash-heavy restaurant environments; a crime endorsement can cover this

Review your policy against common restaurant cooking risk factors annually, not just at renewal.

Why most Texas restaurants miss out on full protection

Here is the uncomfortable truth we see repeatedly: most Texas restaurant owners choose minimal coverage because it feels like the financially responsible move. Premiums are a known cost. Claims feel like a remote possibility. So owners cut coverage to save a few hundred dollars a year, and then a grease fire or a slip-and-fall lawsuit reminds them what real financial exposure looks like.

The other factor is misconception. Many owners believe a Business Owner’s Policy covers everything. It does not. Food contamination, flood, cyber attacks, and liquor liability are all separate conversations. Buying a BOP and stopping there is like locking the front door but leaving the back wide open.

What we have learned from years of working with Texas businesses is this: the owners who fare best after a major claim are the ones who reviewed their risk management insights annually, updated their property valuations, and trained their staff on TABC compliance to keep liquor liability rates in check. Investing a bit more in the right coverage now is almost always cheaper than absorbing even one major uninsured loss.

Connect with Texas restaurant insurance specialists

Building the right insurance plan for your Texas restaurant takes more than a quick online quote. It takes someone who understands your specific risks, your region, and the coverage options available across multiple carriers.

At Hettler Insurance Agency, we have been helping Texas business owners navigate commercial insurance since 1992. As an independent agency representing over 30 top-rated carriers, we shop your coverage across the market to find the right fit at the right price. Whether you are starting fresh or need a review of your current plan, we can help. Start by reviewing minimum insurance requirements for Texas businesses, then connect with our team at hettlerinsurance.com for a no-pressure consultation tailored to your restaurant.

Frequently asked questions

Is workers’ compensation insurance mandatory for Texas restaurants?

Workers’ comp is optional in Texas but strongly recommended. Without it, your restaurant faces direct liability for employee medical costs and lost wages, and you may not qualify for certain contracts.

What insurance is required for serving alcohol in Texas restaurants?

Liquor liability insurance is critical under TABC Dram Shop laws, protecting your business against claims tied to alcohol service. Many landlords and lenders also require it by contract.

How much does restaurant insurance cost in Texas?

General liability averages $500 to $1,500 per year, workers’ comp runs about $22 per month per employee, and liquor liability costs $800 to $2,000 annually. Keep in mind that claims average $9,000 per incident, making adequate coverage a sound financial decision.

Are floods and windstorms covered under typical restaurant property insurance in Texas?

No. Flood and windstorm coverage must be purchased separately in coastal Texas through TWIA or FEMA programs. Standard commercial property policies exclude these perils in most high-risk Texas regions.

Recommended

- Choosing a Texas Insurance Carrier | Hettler Insurance Agency

- How Does Open Carry Affect Insurance for Texas Businesses?

- 3 Common Homeowners Insurance Mistakes | Lubbock TX Homeowners Guide – Hettler Insurance Agency

- Tips About Auto Insurance From Lubbock Texas [Infographic] – Hettler Insurance Agency

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: Is workers’ compensation insurance mandatory for Texas restaurants?

Q2 ?: What insurance is required to serve alcohol in a Texas restaurant?

Q3 ?: How much does restaurant insurance typically cost in Texas?

Q4 ?: Are floods and windstorms covered under typical restaurant property insurance in Texas?

Q5 ?: What gaps and endorsements do Texas restaurant owners most often miss?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com