Specialty Insurance for Texas Homeowners

Texas weather does not play fair. Hail storms roll through Lubbock without warning, wildfires push across West Texas grasslands, and wind events can strip a roof in minutes. Standard homeowners insurance policies often fall short when your home sits in a high-risk zone or when a carrier decides the risk is too great to cover at all. This guide walks you through exactly what specialty insurance is, what you need to qualify, how to apply, and how to verify you are actually protected before the next storm season arrives.

Table of Contents

- Understanding specialty insurance options in Texas

- What you need before applying: Eligibility and requirements

- Steps to get specialty insurance in Texas

- Verifying your coverage and avoiding common mistakes

- Get help navigating specialty insurance in Texas

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Shop multiple carriers | Comparing at least three insurers helps optimize coverage and cost for specialty risks in Texas. |

| Know eligibility requirements | Prepare proof of denial and property documentation before applying for FAIR or TWIA coverage. |

| Expert agents simplify the process | Working with independent agents helps avoid limited plans and ensures you get replacement cost protection. |

| Review coverage carefully | Always check for exclusions and gaps after your policy is issued to avoid surprises during a claim. |

| Local help is available | Insurance agencies in Lubbock and surrounding areas offer guidance tailored to Texas weather risks. |

Understanding specialty insurance options in Texas

Specialty insurance refers to coverage designed for risks that standard homeowners policies either exclude or severely limit. Think of it as a targeted layer of protection built for situations where a typical policy leaves gaps. In Texas, those gaps show up fast.

Standard homeowners policies cover a broad range of perils, but they often exclude or cap coverage for wind, hail, wildfire, and flood. Specialty coverage fills those specific holes. Here is a quick comparison:

| Coverage type | What it covers | Who typically needs it |

|---|---|---|

| Standard homeowners | Fire, theft, liability, some weather | Most homeowners in low-risk areas |

| Windstorm (TWIA) | Wind and hail for coastal Texas | Homeowners in TWIA-eligible coastal counties |

| Texas FAIR Plan | Basic named-peril coverage | High-risk homes denied by standard carriers |

| Wildfire endorsement | Fire damage in high-risk zones | West Texas and rural homeowners |

| Flood insurance | Rising water damage | Flood-prone areas statewide |

Several situations trigger the need for specialty coverage:

- Your home has been denied by one or more standard carriers

- You live in a wildfire-prone or wind-heavy region

- Your property has prior claims that make standard insurers nervous

- You own an older home with outdated systems or materials

- You are in a coastal county where windstorm is excluded from standard policies

For Lubbock homeowners, wind and hail coverage is typically included in standard inland policies but often comes with separate, higher deductibles. Coastal Texas is a different story, where a separate Texas Windstorm Insurance Association (TWIA) policy is required. If you have been denied by two or more carriers, you may qualify for the Texas FAIR Plan, which provides basic named-peril coverage as a last resort.

Important: FAIR Plan and TWIA policies are safety nets, not ideal solutions. They offer limited coverage compared to standard market options. Always explore specialty homeowners policies in the private market first.

What you need before applying: Eligibility and requirements

Now that you know the types, here is what you will need before applying for specialty coverage.

Eligibility requirements vary depending on which program or carrier you are pursuing. The documents and steps below apply broadly, but your specific situation may require additional items.

| Document or requirement | Why it matters |

|---|---|

| Proof of denial from two insurers | Required to apply for Texas FAIR Plan |

| Proof of home ownership | Verifies insurable interest |

| Home inspection report | Required for TWIA coastal certification |

| Prior claims history | Affects eligibility and pricing |

| Home condition details | Age, roof type, construction materials |

Key eligibility facts to know:

- FAIR Plan policies grew to 41,000 in 2024, showing how many Texas homeowners are being pushed out of the standard market

- TWIA coverage averages $2,300 per year and requires a 30-day waiting period plus a home inspection and windstorm certification

- You must apply through a licensed Texas agent for both FAIR Plan and TWIA

- Wildfire coverage eligibility depends on your home’s proximity to brush, construction type, and local fire protection resources

- Review storm insurance requirements before storm season, not after a loss

Pro Tip: Do not wait until a storm is in the forecast to start this process. TWIA has a 30-day waiting period, and FAIR Plan applications take time to process. Start early.

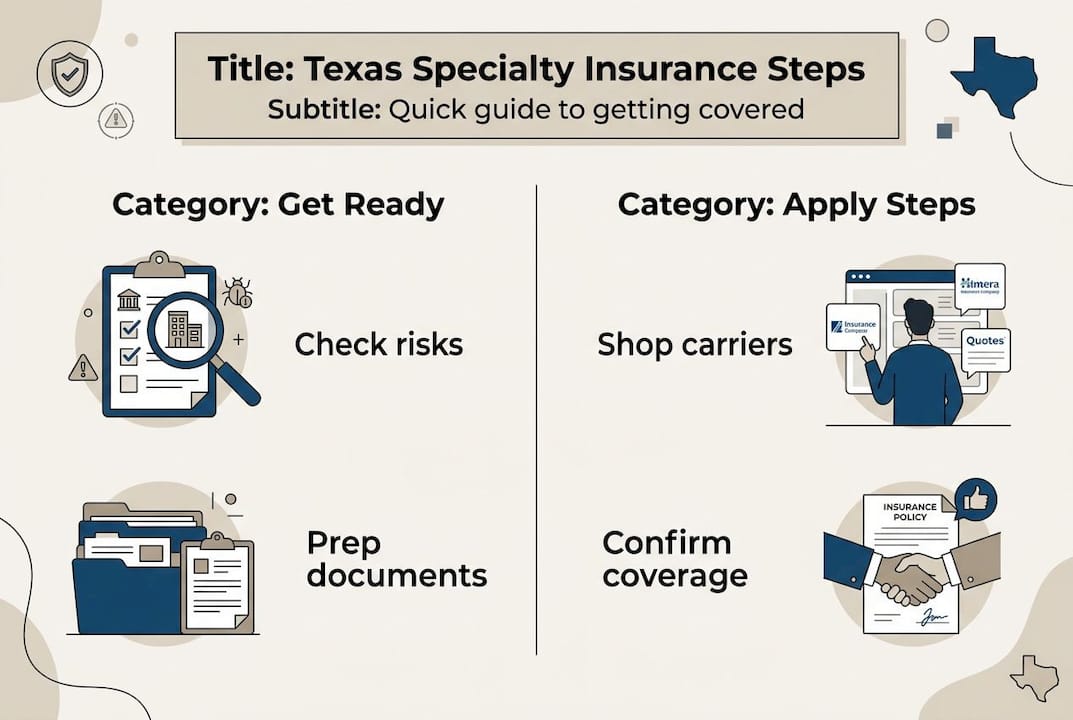

Steps to get specialty insurance in Texas

With documents ready, you are prepared to start the process. Here is how to make your specialty insurance happen.

Step 1: Assess your actual risk

Look at your location, your home’s age and construction, and your claims history. Be honest about what risks you face. Lubbock homeowners should focus on hail and wind. Rural West Texas homeowners need to think about wildfire. Coastal homeowners need windstorm coverage.

Step 2: Contact an independent insurance agent

This is the most important step. An independent agent works with multiple carriers, not just one. Working with independent agents means someone is shopping the market on your behalf, comparing options, and explaining the differences clearly.

Step 3: Shop at least three carriers

Independent Texas agents recommend comparing at least three carriers before committing. Rates, exclusions, and deductibles vary significantly. Do not accept the first quote.

Step 4: Verify replacement cost coverage

Make sure your policy covers the actual cost to rebuild your home, not just its market value. These two numbers can be very different, especially in today’s construction market. Choosing the right carrier means verifying this detail before you sign.

Step 5: Check the carrier’s financial strength

A policy is only as good as the company behind it. Look for carriers rated A or better by AM Best. A financially strong carrier is more likely to pay claims quickly and fully.

Step 6: Submit your application and review the policy

Once you select a carrier, submit your application with all required documents. When the policy arrives, read it. Check the declarations page for coverage limits, deductibles, and any exclusions.

Step 7: Confirm your coverage is active

Do not assume coverage starts immediately. Confirm the effective date, especially if you are switching carriers or adding a new policy.

Pro Tip: Ask your agent to walk you through the declarations page line by line. Understanding what you have before a claim is far better than discovering gaps after one.

Verifying your coverage and avoiding common mistakes

After your policy is issued, it is crucial to double-check what you are really getting so you avoid regret later.

Reviewing your policy is not optional. It is the step most homeowners skip, and it is the one that costs them the most when a claim is denied.

Here is what to look for when reviewing your specialty policy:

- Coverage limits: Are they high enough to fully rebuild your home? Review insuring for replacement cost to understand why this number matters.

- Deductibles: Specialty policies often have separate, higher deductibles for wind and hail. Know your out-of-pocket exposure before a storm hits.

- Exclusions: Read every exclusion carefully. Common ones include flood, mold, and certain types of water damage.

- Endorsements: These are add-ons that expand coverage. Ask your agent if any apply to your situation.

- Renewal terms: Know when your policy renews and whether rates or terms can change.

Common mistakes Texas homeowners make:

- Assuming a standard policy covers all weather events

- Skipping the FAIR Plan or TWIA application because it feels complicated

- Overpaying by not comparing carriers

- Missing application deadlines before storm season

- Ignoring exclusions until a claim is denied

Remember: FAIR Plan and TWIA are last-resort options with limited coverage. If you can qualify for a private market specialty policy, that is almost always the better choice. Use these programs only when no other option exists.

Get help navigating specialty insurance in Texas

If managing specialty insurance feels overwhelming, know that local help is available. At Hettler Insurance Agency, we have been helping Texas homeowners find the right coverage since 1992. We represent over 30 top-rated carriers, which means we shop the market for you and find options that actually fit your home, your risk, and your budget.

Our team understands West Texas weather risks firsthand. Whether you need homeowners insurance advice for a new home in Lubbock or want to explore unusual insurance types that could fill gaps in your current coverage, we are here to guide you without pressure. Visit Hettler Insurance or call our Lubbock office to get started. Get Hettler, Get Better.

Frequently asked questions

What is specialty insurance, and who needs it in Texas?

Specialty insurance covers risks standard policies exclude, such as windstorm, hail, or wildfire, and is often needed by homeowners who have been denied by standard carriers or who live in high-risk areas across Texas.

How much does specialty insurance cost in Texas?

The Texas FAIR Plan averages roughly $1,440 per year, while TWIA windstorm coverage averages about $2,300 per year; your actual rate depends on your home’s location, age, and risk profile.

What documents are needed to apply for specialty insurance?

You will typically need proof of denial from two standard insurers, proof of home ownership, a recent home inspection report, and details about your home’s construction and prior claims history.

Should I use an independent agent to shop for specialty insurance?

Yes. Independent Texas agents compare multiple carriers, verify that your replacement cost coverage is accurate, and help you avoid limited last-resort plans like FAIR Plan or TWIA unless no better option exists.

What mistakes should I avoid when buying specialty insurance?

Avoid skipping carrier comparisons, ignoring policy exclusions, and waiting until storm season to apply. FAIR and TWIA plans are limited by design, so always pursue private market options first and review your policy details before a claim occurs.

Recommended

- Choosing a Texas Insurance Carrier | Hettler Insurance Agency

- Tips About Auto Insurance From Lubbock Texas [Infographic] – Hettler Insurance Agency

- Should You Add Windshield Coverage to Your Auto Policy in West Texas? – Hettler Insurance Agency

- Child only Health Insurance – Hettler Insurance Agency

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com