TL;DR Summary:

- Texas homeowners insurance policies exclude flood damage, requiring separate flood insurance coverage.

- Texas weather risks like hail, hurricanes, and tornadoes affect policy coverage and deductibles.

- Regular policy reviews and additional endorsements are crucial to avoid coverage gaps and underinsurance.

Buying your first home in Texas is exciting, but assuming your homeowners insurance policy covers every disaster is a costly mistake many new homeowners make. Standard policies leave out flood damage entirely, and Texas-specific risks like hail, hurricanes, and tornadoes add layers of complexity that basic coverage cannot always handle. Homeowners insurance is a financial shield covering various perils and property types, but what those perils actually are depends heavily on your policy type and location. This guide walks you through coverage types, local weather risks, critical exclusions, and practical steps to find affordable protection that actually holds up when you need it most.

Table of Contents

- What homeowners insurance covers in Texas

- Texas weather hazards and how insurance responds

- Common exclusions, endorsements, and pitfalls

- How to shop smarter for homeowners insurance in Texas

- What most Texas homeowners miss about insurance and why it matters

- Your next steps with Texas homeowners insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Texas weather risks matter | Insurance policies need to address unique risks like hurricanes, hail, and flooding that are common statewide. |

| Know your policy | HO-3 is standard for Texas, but not all perils are covered—deductibles and exclusions can significantly affect your protection. |

| Flood and wind require extra | Flood insurance and windstorm coverage often need to be purchased separately, especially for coastal areas. |

| Annual review saves money | Reviewing and shopping your homeowners policy yearly helps maintain adequate coverage and find the best rates. |

| Special limits and endorsements | Valuables such as jewelry or collectibles may require separate endorsements due to low standard coverage limits. |

What homeowners insurance covers in Texas

Now that you know why misunderstanding coverage can be costly, let’s break down what a typical Texas homeowners policy actually includes.

The HO-3 policy is the most common option for Texas homeowners. It covers your dwelling on an open-peril basis, meaning damage is covered unless your policy specifically excludes it. Personal property, however, is covered only for named perils listed in the policy. If you are on a tighter budget, the HO-2 policy covers fewer risks because it only pays for damage caused by perils specifically named in the document.

Texas homeowners insurance policies are organized into six coverage types:

- Coverage A (Dwelling): Covers the structure of your home, including walls, roof, and built-in appliances.

- Coverage B (Other Structures): Covers detached garages, fences, and sheds.

- Coverage C (Personal Property): Covers furniture, electronics, and clothing inside your home.

- Coverage D (Loss of Use): Pays for temporary housing if your home becomes uninhabitable after a covered loss.

- Coverage E (Personal Liability): Protects you if someone is injured on your property and sues.

- Coverage F (Medical Payments): Pays medical bills for guests injured at your home, regardless of fault.

Texas adds specific wrinkles to standard coverage. Coastal areas often face wind and hail exclusions written directly into the policy. Inland homeowners in West Texas face frequent hail events that can directly affect policy premium influences over time. When you shop carriers, it also matters which company you choose, and choosing Texas insurance carriers wisely can determine whether claims are paid quickly or disputed.

| Policy Type | Dwelling Coverage | Personal Property Coverage |

|---|---|---|

| HO-3 | Open peril (broad) | Named perils only |

| HO-2 | Named perils | Named perils only |

| HO-5 | Open peril (broad) | Open peril (broad) |

Pro Tip: Always read the exclusions section of any policy before signing. That section tells you what your insurer will not pay for, which is just as important as what they will.

Texas weather hazards and how homeowners insurance responds

Understanding policy types is step one, but Texas weather risks create another layer of complexity.

Texas faces more severe weather events than nearly any other state. Hurricanes threaten the Gulf Coast, tornadoes sweep through the Panhandle, and hail claims make Texas the nation’s leader in hail-related insurance losses. Each of these events is treated differently by your insurance policy.

Wind and hail are typically covered under a standard HO-3 policy, but coastal homeowners may find these perils excluded. The Texas Windstorm Insurance Association (TWIA) exists specifically to provide wind and hail coverage for properties in designated coastal counties where private insurers will not write the coverage.

Flooding is a separate issue entirely. No standard homeowners policy covers flood damage. You need a policy through the National Flood Insurance Program (NFIP) or a private flood insurer. Hurricane Harvey caused an estimated $125 billion in flood damages, and a large portion of affected homeowners had no flood coverage at all. Understanding your flood risk and insurance needs is critical even in areas that have never flooded before.

Deductibles for wind, hail, and hurricane losses in Texas work differently than your standard deductible. Instead of a flat dollar amount, these are typically calculated as a percentage of your home’s insured value, often ranging from 1% to 5%. On a $300,000 home, a 2% wind/hail deductible means you pay $6,000 out of pocket before insurance kicks in. That is a significant number most first-time buyers do not anticipate.

Increasing insurance costs in Texas are also linked directly to how climate change and coverage calculations are evolving, with carriers adjusting rates as storm frequency increases.

Key weather coverage points to remember:

- Hurricane and named storm deductibles are separate from your standard deductible.

- Hail damage to your roof may trigger a full claim or a depreciated payment depending on your policy’s valuation method.

- Tornado damage is generally covered under wind peril in most HO-3 policies.

- Flood damage requires a completely separate policy, always.

Pro Tip: Even if you live inland in West Texas, hail claims are rising sharply. Make sure your roof coverage reflects replacement cost value, not just actual cash value, which factors in depreciation.

Common exclusions, endorsements, and pitfalls

Weather isn’t the only source of surprises. Let’s look at some critical exclusions and endorsements often missed.

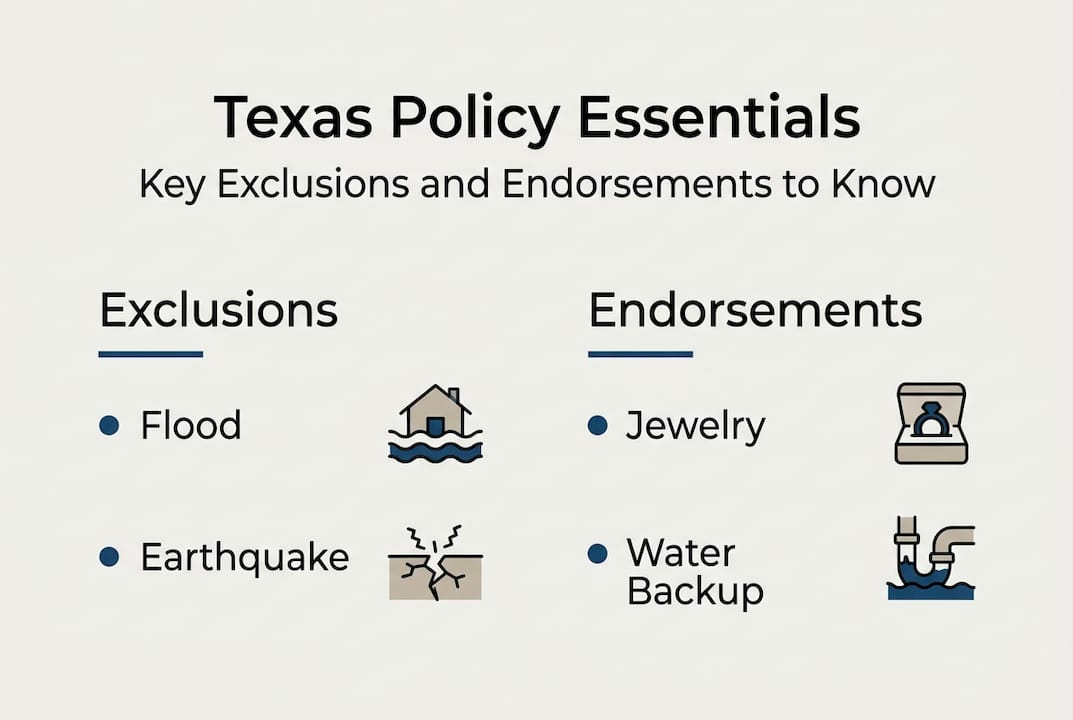

Standard policies exclude flood, earthquake, wear and tear, pest damage, and mold resulting from non-covered water sources. These are not oversights. They are deliberate policy design decisions that can leave you exposed if you assume too much.

Personal property coverage also has special limits for certain categories. Most policies cap coverage on:

- Jewelry and watches (often $1,500 limit)

- Money and bank notes (often $200 limit)

- Watercraft and trailers

- Business property kept at home

- Firearms

If you own valuables above these limits, you need an endorsement (also called a rider or floater) to cover them fully. Review your coverage limits and valuables carefully to know where gaps exist.

Another major pitfall is underinsurance. If you insure your home for its market value instead of its replacement cost (the actual cost to rebuild it from scratch), you may face a coinsurance penalty. This means your insurance company could reduce your claim payout because you were not insured for enough. Construction costs in Texas have risen sharply, making this problem more common.

Vacancy is another overlooked issue. Most policies reduce or eliminate coverage if your home sits vacant for more than 30 to 60 days. Renovation projects, extended travel, or a home between owners can trigger this clause.

Key insight: Not updating your insurance as your home’s value or contents change is one of the most common and expensive mistakes Texas homeowners make.

Your roof coverage changes can also affect your overall policy cost and claim eligibility. Older roofs often receive actual cash value payouts instead of full replacement cost, which can leave you thousands short after a hail event.

Pro Tip: Add an endorsement for water backup coverage. Standard policies typically exclude damage from sewer or drain backups, which is a surprisingly common and expensive claim type.

How to shop smarter for homeowners insurance in Texas

Understanding exclusions paves the way for finding the right policy. Here’s how you can apply this knowledge in your own search.

Shopping for homeowners insurance is not just about finding the lowest premium. It is about finding the right coverage at a fair price. Bundling, home hardening, and annual shopping can keep premiums manageable, but you need a strategy.

Here are practical steps to guide your search:

- Decide between HO-3 and HO-2. If your home is in a hail-prone area or you have significant assets, the broader coverage of an HO-3 is worth the higher premium.

- Compare multiple carriers. Rates vary significantly across companies. An independent agent shops dozens of carriers at once, giving you real options instead of a single quote.

- Ask about discounts. Installing a Class 4 impact-resistant roof can earn you meaningful discounts from many Texas carriers. Security systems, smoke detectors, and storm shutters may also reduce your premium.

- Bundle your policies. Combining home and auto insurance with the same carrier typically saves 10% to 25% on both policies.

- Check your credit score. In Texas, carriers can use your credit-based insurance score to set your rate. Poor credit can nearly double your annual premium compared to someone with excellent credit.

- Review your policy every year. Texas home insurance rates have risen dramatically over the past decade, and your coverage needs change as your home and possessions grow in value. Checking policy rate increases each year helps you stay ahead of gaps.

- Document your belongings. Keep a home inventory with photos and receipts. This speeds up claims and helps you verify you have enough personal property coverage.

Pro Tip: Add flood coverage even if you live outside a mapped flood zone. FEMA data consistently shows that more than 20% of flood claims come from properties in low to moderate risk areas. The premium is often under $500 per year and the protection is significant.

Texas homeowner reading insurance documents at kitchen table

What most Texas homeowners miss about insurance and why it matters

Shopping strategies help, but there is a bigger lesson most new Texas homeowners need to hear directly.

Most people treat homeowners insurance as a box to check at closing. They take the first quote that meets the mortgage lender’s minimum requirements and never look at the policy again. That approach works fine until it doesn’t.

Flood risk is almost universally underestimated. 15% of Harvey flood victims lacked flood insurance despite living outside designated flood zones, and many others were underinsured because of credit scoring effects and coinsurance miscalculations. Your address on a FEMA map is not a reliable indicator of your actual hidden flood risks.

Replacement cost versus market value is another concept most new homeowners confuse. Your home’s market value reflects what a buyer would pay today. Replacement cost reflects what it would actually cost to rebuild your home with current materials and labor. These numbers are often very different, and insuring for the wrong one can devastate your recovery after a major loss.

An annual review is not optional if you want real protection. Credit scores shift, home values rise, and your belongings accumulate. The policy you signed at closing in 2023 may leave you seriously underprotected by 2026 without any updates.

We see this pattern regularly at Hettler Insurance: homeowners who thought they were covered, only to discover gaps at the worst possible moment. Proactive communication with your agent is the single most effective way to avoid it.

Your next steps with Texas homeowners insurance

Having learned the nuances of Texas homeowners insurance, here’s how you can take practical action today.

Knowing what you need is only half the equation. The other half is connecting with someone who can actually get it for you at the right price. At Hettler Insurance Agency, we represent over 30 top-rated carriers, so we can compare coverage options and costs across the market to find what genuinely fits your home, location, and budget.

Whether you are figuring out your minimum coverage needs as a first-time buyer or want a full policy review, our team is ready to help. Visit Hettler Insurance to get started, or call our Lubbock office directly for personalized guidance at no extra fee. Get Hettler, Get Better.

Frequently asked questions

Does homeowners insurance in Texas cover flood damage?

No, standard policies exclude flood damage entirely. You need a separate NFIP or private flood policy to be properly protected.

What is the most common homeowners policy in Texas?

The HO-3 is most common in Texas, offering open-peril dwelling coverage and named-peril protection for personal property.

How do deductibles work for wind/hail and hurricane claims in Texas?

Texas hurricane and wind/hail deductibles are percentage-based, typically 1% to 5% of your home’s insured value, applied separately from your standard deductible.

Are valuables like jewelry fully covered by homeowners insurance?

Most policies apply special limits on valuables, so jewelry, money, and similar items may only be partially covered unless you add a specific endorsement.

How often should I review or update my homeowners insurance policy?

Annual shopping keeps coverage and pricing aligned with your current needs, especially as home values, construction costs, and carrier rates continue to shift in Texas.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Enhanced Frequently Asked Questions ?

Q1 ?: Does homeowners insurance in Texas cover flood damage?

Q2 ?: What is the most common homeowners policy in Texas?

Q3 ?: How do deductibles work for wind, hail, and hurricane claims in Texas?

Q4 ?: Are valuables like jewelry fully covered by a standard homeowners policy?

Q5 ?: How often should I review or update my Texas homeowners insurance policy?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com