TL;DR summary:

- Business insurance audits verify that premiums accurately reflect current business operations and risks.

- Proper record-keeping and classification are essential to avoid costly errors and adjustments.

- Proactive audit readiness helps reduce surprises, save money, and streamline the process.

A business insurance audit is not an investigation into wrongdoing. That misconception causes more unnecessary stress than almost anything else in commercial insurance. The truth is simpler and more useful: an audit is a routine check to make sure your premium matches your actual business activity. If your payroll grew, your premium should reflect that. If your revenue shrank, you may be owed a refund. For Texas business owners in construction, trucking, manufacturing, or any high-risk industry, understanding this process is not optional. It is a core part of managing your costs and keeping your coverage intact.

Table of Contents

- Understanding business insurance audits: Purpose and basics

- How the insurance audit process works in Texas

- Workers’ compensation vs. general liability: Audit differences and requirements

- Common mistakes and how to avoid them during the audit

- How audit outcomes affect your premiums and coverage

- A fresh take: Why proactive audit readiness saves time and money

- Take the stress out of your next insurance audit

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Audit defines your true risk | Insurance audits ensure you pay only for the coverage your business actually needs. |

| Preparation is powerful | Keeping clear records and understanding audit steps can prevent costly errors or penalties. |

| Outcomes can go both ways | An audit may lead to either higher costs or a refund, depending on the accuracy of your business info. |

| Audit type impacts requirements | Workers’ comp and general liability audits have different documentation and focus areas. |

| Help is available | Expert guidance takes hassle out of audits and protects your business. |

Understanding business insurance audits: Purpose and basics

A business insurance audit is a formal review conducted by your insurance carrier to verify that the information used to calculate your premium still matches your actual operations. When you purchase a policy, your insurer estimates your exposure, meaning your payroll, revenue, or number of employees, and sets your premium based on those projections. At the end of the policy term, the insurer checks whether those estimates were accurate.

Insurance audits verify that the coverage and premium paid reflects your business’s actual risk. That single sentence captures the entire purpose. You are not being penalized. You are being recalibrated.

Common triggers for a business insurance audit include:

- End of the policy term (the most common trigger)

- A significant increase or decrease in payroll or revenue

- Adding new employees or subcontractors

- Expanding into new types of work or new locations

- A mid-term change in business operations

The policies most frequently subject to audits are workers’ compensation and general liability. Workers’ compensation premiums are calculated based on payroll and job classifications. General liability premiums are typically based on gross sales or total revenue. Both of these figures change year to year, which is exactly why audits exist.

Audits also serve a compliance function. In Texas, carriers and regulators need accurate data to assess industry-wide risk and set appropriate rates. If your books do not reflect reality, the entire pricing model breaks down. That is bad for everyone, including you.

Understanding the benefits of insurance audits for your business goes beyond just premium accuracy. Audits confirm that your coverage limits are still appropriate for your current size and scope of operations. A business that doubled in revenue but never updated its policy could be dangerously underinsured.

Pro Tip: Keep accurate payroll records, subcontractor certificates, and revenue reports organized throughout the year. Do not wait until the audit notice arrives to start pulling documents together. Year-round record-keeping cuts your audit response time significantly and reduces the chance of errors.

How the insurance audit process works in Texas

Once your policy term ends, the audit process begins. Knowing each step in advance removes the guesswork and helps you respond quickly and correctly.

Here is how a typical business insurance audit unfolds:

- Audit notification. Your insurer sends a notice, usually by mail or email, informing you that an audit is scheduled. This notice will specify the audit type: mail, phone, or in-person.

- Documentation request. The auditor requests specific records to verify your reported exposures. Required insurance audit documents vary by policy type but typically follow a standard list.

- Information review. The auditor compares your submitted documents against the estimates used to set your original premium.

- Premium adjustment. Based on the review, your insurer issues a final audit statement. You may owe additional premium, or you may receive a credit.

- Dispute window. If you disagree with the findings, most carriers allow a formal dispute or appeal period.

Auditors require specific documentation such as payroll records, certificates, and tax forms. Below is a breakdown of what you should have ready.

| Document type | Why it is needed |

|---|---|

| Payroll records (941 forms) | Verifies total wages paid to employees |

| State unemployment tax records | Confirms employee headcount and wages |

| Certificates of insurance for subcontractors | Proves they carried their own coverage |

| General ledger or income statements | Validates gross sales or revenue figures |

| 1099 forms for independent contractors | Clarifies contractor vs. employee classification |

| Job descriptions or duty records | Supports employee classification codes |

Audit timelines vary. Most mail audits require a response within 30 days of the notice. In-person audits are typically scheduled within 60 to 90 days after policy expiration. Phone audits fall somewhere in between.

Pro Tip: Designate one person in your organization as the audit point of contact. This person should know where all financial and payroll records are stored, understand your subcontractor relationships, and be authorized to speak with the auditor. Inconsistent or conflicting information from multiple staff members is a common cause of audit delays and errors.

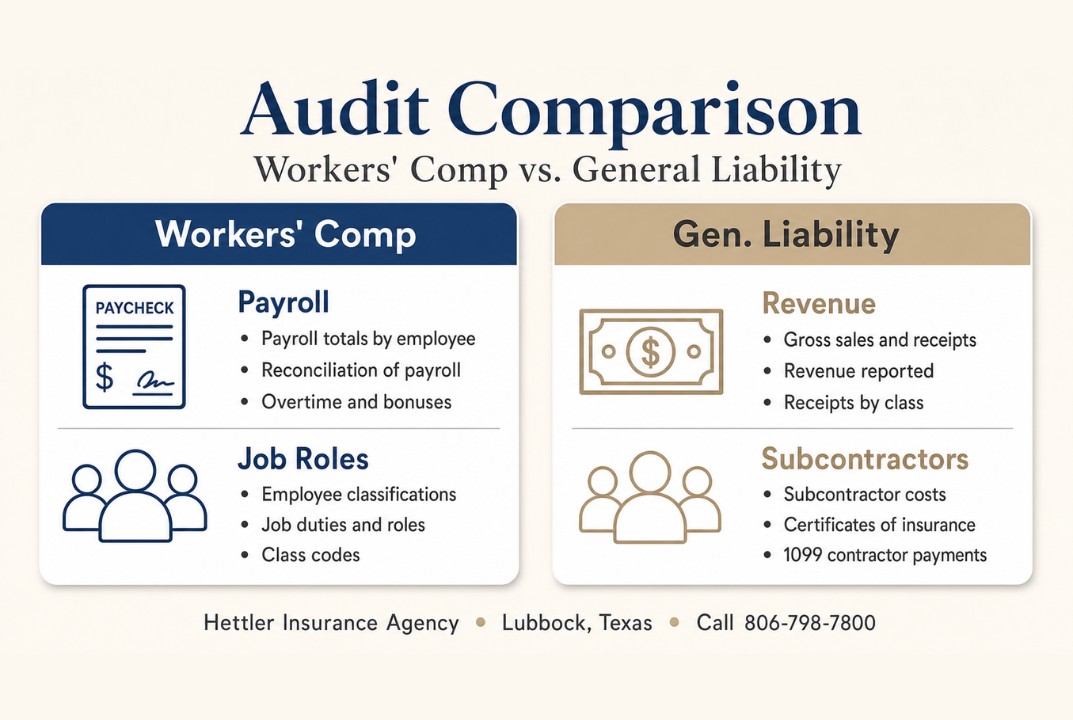

Workers’ compensation vs. general liability: Audit differences and requirements

Not all audits work the same way. The type of policy being audited determines what the auditor focuses on, what documents you need, and where errors are most likely to occur.

Workers’ compensation audits center on payroll. Your premium is calculated using payroll figures multiplied by a rate tied to each employee’s job classification code. A roofer carries a much higher rate than an office administrator. If your employees’ duties changed during the policy year, or if you hired new workers in higher-risk roles, the audit will catch that and adjust accordingly.

Workers’ compensation audit requirements are especially important for Texas employers because Texas is the only state where private employers are not required by law to carry workers’ compensation. That makes accurate classification and documentation even more critical for those who do carry it.

General liability audits focus on gross sales, total revenue, and subcontractor costs. Your general liability premium is typically tied to how much business you do, not just how many people you employ. If your revenue increased significantly, your exposure increased too.

Audit requirements and focuses differ between workers’ compensation and general liability policies in ways that catch many business owners off guard. See the audit comparison.

| Audit factor | Workers’ compensation | General liability |

|---|---|---|

| Primary basis | Payroll by job classification | Gross sales or revenue |

| Key documents | 941s, payroll journals, duty records | Income statements, subcontractor invoices |

| Subcontractor treatment | Must show proof of their coverage | Uninsured subs may be added to your exposure |

| Common error | Misclassifying employee duties | Underreporting revenue or sub costs |

| Potential outcome | Higher premium for reclassified workers | Additional premium for unreported sales |

Why classification accuracy matters in high-risk industries:

- A construction worker incorrectly classified as a general laborer instead of a framer can trigger a significant premium increase when corrected.

- A subcontractor without their own certificate of insurance may be treated as your employee for audit purposes, adding their payroll or costs to your exposure.

- Mixing clerical and field employee payroll into a single classification is one of the most expensive mistakes in workers’ compensation audits.

Keep job descriptions updated and make sure your payroll system separates employees by their actual duties, not just their job titles.

Common mistakes and how to avoid them during the audit

Even well-run businesses make avoidable errors during insurance audits. Most of these mistakes come down to poor record-keeping, inconsistent data, or a misunderstanding of how classification codes work.

The most common audit mistakes include:

- Missing or incomplete payroll records. If you cannot produce 941 forms or payroll journals, the auditor may estimate your exposure, almost always on the high end.

- Inconsistent data between tax filings and payroll records. If your W-2 totals do not match your 941 quarterly reports, the auditor will flag it.

- Employee misclassification. Assigning workers to lower-risk classification codes to reduce premium is a serious error that can result in back premiums and policy issues.

- No certificates of insurance for subcontractors. Without proof that your subs carried their own coverage, their costs may be added to your policy exposure.

- Failing to separate payroll by job duty. Lumping all employees under one code when they perform different roles inflates your premium unnecessarily.

“Overlooking documentation and misclassifying employees are among the most frequent and costly mistakes to avoid during an audit, and both are entirely preventable with consistent record-keeping.”

The financial impact of these errors is real. A single misclassified employee in a high-risk trade can add hundreds or even thousands of dollars to your annual premium. Multiply that across a crew of ten workers, and the cost becomes significant.

Pro Tip: Conduct a brief internal review of your payroll records and subcontractor files every quarter. Verify that job classifications match actual duties, that all subcontractor certificates are current, and that your revenue figures are being tracked accurately. Treat this as part of your routine business operations, not as a one-time scramble before audit season.

Staying organized also protects you if you need to dispute audit findings. Clean, consistent records are your best defense.

How audit outcomes affect your premiums and coverage

The audit does not just close out your policy year. It sets the tone for your next renewal and can have a direct impact on your operating budget.

Two outcomes are possible:

If your actual exposures were higher than estimated, you will owe additional premium. This is called an audit balance due. If your actual exposures were lower, you will receive a credit or refund applied to your next policy term.

Audit findings can lead to increased premiums or, in some cases, refunds for overpayments. Either direction is possible, and both are legitimate outcomes of an accurate audit.

Here is how to respond to your audit results:

- Review the audit statement carefully. Check every classification code, payroll figure, and revenue total listed. Compare them against your own records.

- Identify discrepancies immediately. If a number does not match your records, flag it before paying or accepting the adjustment.

- Contact your agent. Do not go directly to the carrier alone. Your independent agent can review the audit findings with you and advocate on your behalf.

- File a formal dispute if needed. Most carriers have a structured dispute process. Submit your supporting documents, clearly identify the error, and request a revised audit statement.

- Update your next policy estimate. Use your actual audit figures to set more accurate projections for the upcoming policy year, reducing the chance of another large adjustment.

What amplifies audit costs:

- Lack of documentation forces the auditor to estimate, and those estimates rarely favor the business owner.

- Errors caught late in the process may result in retroactive premium charges with less time to plan for the payment.

- Repeated classification errors can trigger increased scrutiny on future audits.

Accurate records are not just about compliance. They are a direct cost control tool for your business.

A fresh take: Why proactive audit readiness saves time and money

Most business owners we speak with at Hettler Insurance view the audit as an annual inconvenience. Something to survive, not something to use. That mindset is costing them money.

Here is what we have seen over decades of working with Texas businesses: the owners who treat audit readiness as part of their ongoing risk management strategy consistently see fewer premium surprises. They are not scrambling to find records. They are not guessing at subcontractor classifications. They have clean books, current certificates, and a clear picture of their exposure.

The audit is not your insurer’s tool. It is yours. It tells you whether your coverage is still sized correctly for your business. It confirms whether your classifications are accurate. And it gives you a documented baseline for your next renewal conversation.

Reviewing your preparedness best practices throughout the year, not just at audit time, is the single most effective way to control your commercial insurance costs. Build the habit. Assign the responsibility. And call your agent before the audit notice arrives, not after.

Take the stress out of your next insurance audit

Navigating a business insurance audit is much easier when you have an experienced, independent agent in your corner. At Hettler Insurance Agency, we have been helping Texas business owners understand their coverage, prepare for audits, and avoid costly errors since 1992.

Whether you are facing your first audit or your fifteenth, our team reviews your documentation, explains your audit statement in plain language, and advocates directly with your carrier if something looks wrong. We also help you understand your minimum insurance requirements so your coverage stays properly aligned with your actual operations. Call us at Hettler Insurance Agency in Lubbock, Texas, and let us make your next audit straightforward, accurate, and stress-free.

Frequently asked questions

What triggers a business insurance audit in Texas?

Audits are generally triggered at the end of a policy term, after significant operational changes, or if your insurer notices discrepancies. Insurance audits verify that the coverage and premium paid reflects your business’s actual risk.

What documents are required for a business insurance audit?

You will typically need payroll records, tax forms, certificates of insurance for subcontractors, and business financial statements. Auditors require specific documentation such as payroll records, certificates, and tax forms to complete their review accurately.

Can my insurance premium decrease after an audit?

Yes, if your reported exposures were overestimated, you may receive a refund or a lower premium adjustment at renewal. Audit findings can lead to increased premiums or, in some cases, refunds for overpayments.

What happens if I don’t comply with an insurance audit?

Non-compliance can result in policy cancellation or an estimated premium billed by your insurer, which is typically calculated at the highest possible exposure rate.

How can I prepare for a business insurance audit?

Keep accurate, up-to-date records year-round and assign a dedicated point person for all communications with your insurer. Auditors require specific documentation including payroll records, certificates, and tax forms, so having these organized in advance saves significant time.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: What triggers a business insurance audit in Texas?

Q2 ?: What documents are required for a business insurance audit?

Q3 ?: How do workers’ compensation and general liability audits differ?

Q4 ?: Can my insurance premium decrease after an audit?

Q5 ?: How can I prepare for a business insurance audit?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com