TL;DR summary:

- Commercial auto insurance is essential for Texas businesses using vehicles for work purposes.

- Regular policy reviews and updates are vital as business operations change to prevent coverage gaps.

- Using bundling, higher deductibles, and telematics can significantly reduce ongoing insurance costs.

One uninsured accident involving a company truck can wipe out months of profit, expose your business to a lawsuit, and leave you scrambling to cover costs your personal auto policy simply will not touch. Texas law requires commercial coverage for vehicles used in business operations, and the penalties for getting it wrong range from license suspensions to six-figure liability judgments. If your business relies on vehicles, whether that is one service van or a full fleet, getting the right commercial auto insurance is not optional. This guide walks you through every step.

Table of Contents

- What is commercial vehicle insurance and who needs it?

- What you need to get started: information, documents, and requirements

- Step-by-step: how to insure your commercial vehicles in Texas

- Smart ways to save on commercial vehicle insurance

- Our perspective: what most Texas business owners miss about insuring commercial vehicles

- Get expert help insuring your Texas commercial vehicles

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Texas business vehicles require special insurance | Most vehicles used mainly for business in Texas must have commercial auto insurance for full legal and financial protection. |

| Gather documents before shopping | Have your business ID, vehicle details, and driver data ready to get accurate insurance quotes quickly. |

| Compare and customize for savings | Working with independent agents and using discounts like bundling or telematics can lower your premiums by up to 30 percent. |

| Review coverage annually | Your business grows and changes, so update your policy each year to avoid costly coverage gaps. |

What is commercial vehicle insurance and who needs it?

Commercial vehicle insurance covers vehicles used for business purposes. It is not the same as your personal auto policy, and the difference matters more than most business owners realize. A personal auto policy is written assuming the vehicle is used for commuting and personal errands. The moment you use that vehicle to haul equipment, transport clients, make deliveries, or represent your company, you are likely operating in a coverage gap.

What counts as a commercial vehicle in Texas?

Texas insurers and regulators use a practical three-part test to determine whether a vehicle needs commercial coverage. According to the process to get commercial auto insurance in Texas, you need to determine whether:

- The vehicle is used more than 50% of the time for business purposes

- The vehicle is titled in the business name (an LLC, corporation, or partnership)

- The vehicle transports goods, equipment, or people for hire

If any of those three conditions apply, you need commercial vehicle coverage. Period.

Which businesses are most commonly affected?

Any Texas business that operates, owns, or regularly uses a vehicle for work owes it to itself to verify coverage status before the next trip off the lot.

The list is longer than most owners expect:

- Contractors and tradespeople (plumbers, electricians, HVAC technicians, roofers)

- Landscaping and lawn care companies

- Food delivery and catering services

- Real estate agents who drive clients to showings

- Medical or home health care providers making house calls

- Retail businesses that make product deliveries

- Trucking and logistics companies

- Cleaning and janitorial service providers

Even part-time side businesses that use a personal truck to haul materials can fall into this category. If you also use your vehicle for rideshare insurance limits situations like driving for Uber or Turo, your standard auto policy has specific exclusions you need to understand.

What happens without proper coverage?

The financial consequences are direct and serious. If a driver in a company vehicle causes an accident while on the job and only a personal policy is in place, the insurer can deny the claim entirely. That leaves your business exposed to medical costs, property damage, lost wages claims, and legal fees. Proper fleet vehicle maintenance reduces accident risk, but it does not replace the need for coverage. And if your business is seeking financing, lenders offering business lending options typically require proof of commercial insurance on all company vehicles before approving a loan.

What you need to get started: information, documents, and requirements

Once you know your vehicles require commercial coverage, gathering the right information before you contact an agent will save you time and prevent quoting delays. Incomplete or inaccurate information leads to quotes that do not reflect your real risk, which means you could end up either overpaying or underinsured.

According to the Texas commercial auto insurance process, agents need your EIN, VINs, driver records, and annual mileage estimates to prepare accurate quotes. Here is a breakdown of what to collect:

Required information:

- Business legal name and Employer Identification Number (EIN)

- Vehicle Identification Numbers (VINs) for all vehicles

- Current vehicle registrations

- Year, make, model, and gross vehicle weight rating (GVWR) for each vehicle

- Names, dates of birth, and driver’s license numbers for all drivers

- Motor vehicle records (MVRs) for each driver

- Estimated annual mileage per vehicle

- Primary use description (delivery, service calls, hauling, etc.)

- Coverage currently in place, if any

Helpful but not always required:

| Document | Why it helps |

|---|---|

| Previous loss runs (3-5 years) | Shows claim history, affects pricing |

| Safety training certifications | Can qualify you for premium discounts |

| DOT number (if applicable) | Required for commercial trucking compliance |

| Lease or financing agreements | May require specific coverage minimums |

| List of named drivers with MVRs | Speeds up underwriting approval |

Pro Tip: Gather all your driver information before your first call to an agent. Insurers scrutinize driver history closely. A single driver with multiple violations can significantly raise your premium across the entire policy, so knowing that in advance gives you time to address it.

Accurate mileage estimates also affect your rate more than many business owners expect. Underestimating mileage to lower your premium is a common mistake. If you file a claim and the insurer discovers the discrepancy, they can reduce or deny your payout. For auto insurance tips that apply to both personal and commercial vehicles, keeping your information current and honest is always the best strategy.

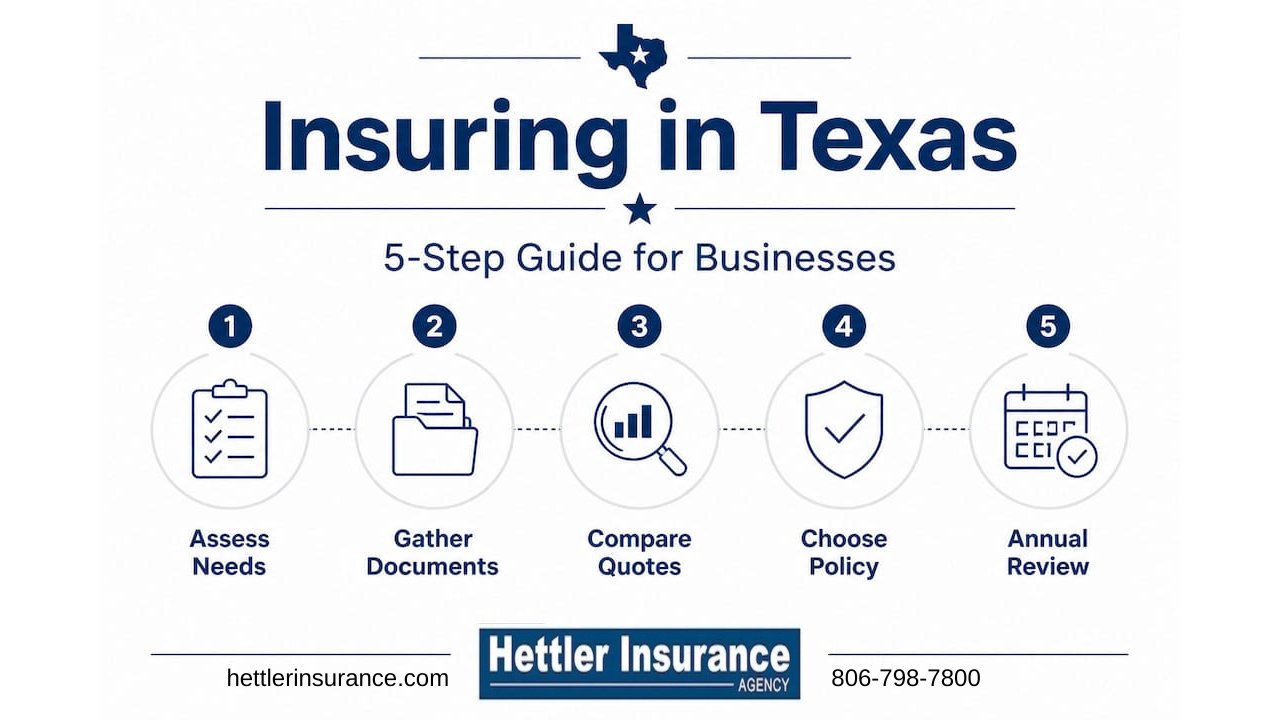

Step-by-step: how to insure your commercial vehicles in Texas

With your documents in hand, the next step is actively insuring your vehicles by following these core actions. The process is more structured than buying personal auto insurance, but it is straightforward when you know what to expect.

- Assess your coverage needs. Determine liability limits, physical damage coverage, and whether you need specialized endorsements (cargo coverage, hired/non-owned auto, etc.).

- Contact a licensed Texas independent insurance agent. An independent agent can compare insurance carriers across multiple companies, giving you more options than a single-company agent.

- Submit your documents. Provide all vehicle, driver, and business information gathered in the previous step.

- Receive and compare quotes. Review not just the price but also coverage limits, exclusions, deductibles, and carrier financial ratings.

- Underwriting review. The insurer reviews driver records, vehicle details, and business type before finalizing your rate. This can take 24 to 72 hours for straightforward accounts.

- Policy issuance and activation. Once approved, you receive your policy documents, certificates of insurance, and ID cards for each vehicle.

According to the step-by-step Texas guide from licensed attorneys familiar with Texas commercial law, shopping quotes through agents with access to licensed Texas insurers and completing underwriting before driving is the only way to ensure you are legally covered from day one.

Never assume coverage is active until you have a written binder or policy confirmation in hand. A verbal agreement is not a policy.

Agent vs. direct online quote: which is better for commercial coverage?

| Factor | Independent agent | Direct online quote |

|---|---|---|

| Access to multiple carriers | Yes, 10 to 30+ | Usually one carrier |

| Ability to customize coverage | High | Limited |

| Expert guidance on exclusions | Yes | Rarely |

| Speed of initial quote | 1 to 2 business days | Immediate |

| Best for complex fleets | Yes | No |

| Cost | No extra fee | No extra fee |

For most Texas small businesses, an independent agent is the better choice. The additional time is worth it when the coverage actually fits your operation.

Pro Tip: Schedule an annual policy review every year at renewal time. Your business changes, and your coverage needs to change with it. Adding a vehicle, hiring a new driver, or expanding into a new service area without updating your policy can create coverage gaps that only show up at the worst possible moment.

Smart ways to save on commercial vehicle insurance

Now that your coverage is active, consider these strategies for ongoing savings and smarter risk management. Commercial auto premiums are rising in Texas, but there are proven ways to reduce what you pay without sacrificing protection.

Bundling coverage

Combining your commercial auto policy with your general liability, commercial property, or business owners policy (BOP) with the same carrier can save 10 to 20% on your total premium. Carriers reward loyalty and consolidated accounts with meaningful discounts. Ask your agent specifically about bundle auto insurance options for your business accounts.

Adjusting your deductible

Raising your physical damage deductible from $500 to $1,000 or $2,500 can reduce your premium 20 to 30%. This strategy works well for businesses with strong cash reserves that can absorb a moderate out-of-pocket expense after a minor incident, rather than filing a claim that could raise future rates.

Technology and telematics

Telematics programs use GPS and driving behavior data to reward safe drivers with lower premiums. Many major Texas commercial insurers offer opt-in telematics discounts for fleets that demonstrate low-risk driving patterns. AI dashcams go further: according to insurance cost mitigation research, carriers are actively offering discounts to fleets that use AI dashcams, driver training programs, and telematics data sharing, all of which help control the rising cost of claims in 2026. Additionally, regular fleet servicing reduces the likelihood of breakdowns that lead to accidents and costly claims.

Key savings strategies at a glance:

- Bundle commercial auto with general liability or a BOP for 10 to 20% off

- Raise deductibles strategically to lower premiums 20 to 30%

- Enroll drivers in certified defensive driving courses

- Install telematics or AI dashcam systems and share data with your carrier

- Remove drivers with poor records from vehicles they do not regularly use

- Review your policy customization options annually to eliminate unused coverage

Pro Tip: Independent agents have access to carrier-specific discount programs that are not always advertised publicly. Ask your agent directly: “What discounts am I currently not taking advantage of?” That single question can save you hundreds of dollars per year.

Our perspective: what most Texas business owners miss about insuring commercial vehicles

Here is something most guides will not tell you directly: the biggest risk to your commercial vehicle coverage is not the accident you did not prevent. It is the coverage gap you did not notice.

Most Texas business owners treat commercial insurance as a one-time purchase. They buy it, file it, and forget it until renewal. The problem is that businesses grow and change constantly. You hire a new driver in March. You add a second truck in July. You expand from residential to commercial service work in October. Each of those changes creates a new exposure. If your policy has not been updated, you may be driving those new risks uncovered without realizing it.

Annual reviews are essential specifically because business growth creates gaps that did not exist when the policy was originally written. This is especially true in West Texas, where businesses in construction, energy services, and agriculture regularly expand their vehicle operations faster than their insurance documentation reflects.

The other blind spot we see frequently involves hired and non-owned auto coverage. If an employee uses their personal vehicle for a business errand and causes an accident, your business can be held liable even though you do not own that vehicle. Most basic commercial auto policies do not include this coverage automatically. It is an endorsement (an add-on to your policy) that many business owners never think to ask for.

Understanding the future of auto insurance is also increasingly relevant: autonomous vehicles, telematics scoring, and usage-based policies are already changing how carriers underwrite risk. Businesses that adopt safety technology now will be better positioned for lower rates as those pricing models become standard. That is not just a prediction. It is already happening with telematics-based commercial accounts in Texas.

The bottom line from our experience: treat your commercial vehicle policy as a living document. Review it every year. Update it every time something changes. Call your agent before you make a major business decision involving vehicles, not after.

Get expert help insuring your Texas commercial vehicles

Navigating commercial vehicle insurance on your own is manageable, but the stakes are high enough that having an experienced agent in your corner makes a real difference. At Hettler Insurance Agency, we have been helping Texas business owners protect their vehicles, their teams, and their operations since 1992.

As an independent agency based in Lubbock, we represent over 30 top-rated carriers and shop your coverage across all of them to find the right fit at the best available price. You pay no extra fee for that service. Whether you need coverage for a single work truck or a multi-vehicle fleet, we know what Texas commercial policies should include and what they often leave out. If you are also evaluating the minimum business insurance your company legally needs, we can walk through that with you too. Call us, and we will handle the details.

Frequently asked questions

What types of vehicles need commercial insurance in Texas?

Vehicles used primarily for business (over 50% business use), titled in the business name, or used to transport goods or people for hire require commercial insurance in Texas.

How can I lower the premium for my company’s vehicle insurance?

You can save 10 to 30% by bundling coverage, raising deductibles, using telematics or driver safety technology, and reviewing your policy annually as your business grows.

Is a personal auto policy enough for business vehicles in Texas?

No. A personal auto policy typically excludes most business uses, which means claims involving business-related driving can be denied, leaving your company fully exposed to liability.

Why are commercial auto insurance costs rising in 2026?

Claims inflation and litigation are the primary drivers of rising commercial auto rates in 2026, but AI dashcams, driver training programs, and telematics data sharing can help offset those increases.

Can I get a quote from more than one insurance company at once?

Yes. Working with an independent agent gives you access to multiple Texas carriers simultaneously, so you can compare coverage options and pricing without contacting each insurer separately.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: When is commercial auto insurance required in Texas?

Q2 ?: Which Texas businesses most often need commercial vehicle insurance?

Q3 ?: What documents do I need to gather before getting a commercial auto quote?

Q4 ?: How long does the commercial auto quoting and issuance process take?

Q5 ?: How can a Texas business save on commercial auto premiums without losing coverage?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com