TL;DR:

- A Business Owners Policy combines essential coverages but requires customization for Texas risks.

- Eligibility depends on revenue, industry, size, and risk level, with high-risk sectors needing special endorsements.

- Standard BOPs typically exclude flood, earthquake, and pandemics, making additional policies or endorsements necessary.

Many Texas small business owners assume that buying a bundled insurance policy means they’re covered for everything. That assumption can be costly. A Business Owners Policy, or BOP, combines general liability, commercial property, and business interruption insurance into one package, often at a 15-30% discount compared to buying each policy separately. But bundled does not mean blanket. Texas businesses face unique risks, from hailstorms to flooding, that a standard BOP may not cover at all. This guide breaks down exactly what a BOP includes, who qualifies, what’s excluded, and how to customize your coverage so you’re not caught off guard when a claim hits.

Table of Contents

- What is a business owners policy?

- Who qualifies for a business owners policy in Texas?

- Core coverages and exclusions

- Texas business risks: Customizing your BOP

- A fresh perspective: Avoiding gaps most Texas businesses miss

- Find the right business owners policy for your Texas business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| BOP saves money | Bundling coverages in a BOP typically provides a 15-30% discount over separate policies. |

| Eligibility varies by risk | Low-risk Texas businesses usually qualify for BOP, but construction and high-risk sectors often need special solutions. |

| Texas exclusions matter | Flood, hail, and other local risks require additional endorsements or separate policies. |

| Review coverage annually | Annual insurance reviews help spot gaps from evolving Texas laws and weather risks. |

| BOP isn’t one-size-fits-all | Customize your policy to protect against specific dangers faced by your Texas business. |

What is a business owners policy?

A Business Owners Policy is a packaged insurance solution designed specifically for small to medium-sized businesses. Instead of managing three separate policies, you get one streamlined package that addresses your most common exposures. That simplicity saves time and money.

Here’s what a standard BOP includes:

- General liability: Covers third-party bodily injury, property damage, and advertising injury claims. If a customer slips and falls in your restaurant or a contractor damages a client’s property, this is the coverage that responds.

- Commercial property: Protects your building, equipment, inventory, and business personal property from covered perils like fire, theft, vandalism, and wind damage.

- Business interruption: Pays for lost income and ongoing operating expenses if your business has to shut down temporarily due to a covered loss.

For Texas businesses, the value of bundling is especially clear. West Texas hailstorms, high theft rates in urban corridors, and the sheer cost of rebuilding after a fire make each of these three coverages critical. Buying them separately means paying more and managing more. A BOP simplifies both.

| Coverage | What it protects | Typical standalone cost |

|---|---|---|

| General liability | Third-party injury and damage | $500-$1,500/year |

| Commercial property | Buildings, inventory, equipment | $1,000-$3,000/year |

| Business interruption | Lost income during closure | $750-$2,000/year |

| BOP (bundled) | All three combined | Often 15-30% less |

One area Texas business owners sometimes overlook is how certain business activities can affect their coverage. For example, understanding open carry insurance impacts on your liability exposure is worth a conversation with your agent before you finalize your policy.

For comprehensive BOP details including how each coverage layer works together, reviewing a full policy breakdown is a smart starting point.

Pro Tip: When bundling into a BOP, ask your agent about multi-policy discounts. If you also carry workers’ compensation or a commercial auto policy, stacking those with a BOP through the same carrier can produce additional savings beyond the standard bundle discount.

Who qualifies for a business owners policy in Texas?

Not every business is eligible for a standard BOP. Insurers use specific criteria to determine whether your business fits the profile. Understanding these thresholds upfront saves you time and helps you plan for alternatives if you don’t qualify.

Standard BOP eligibility generally requires:

- Revenue under $5 million annually. Businesses with higher revenues typically need a more customized commercial package.

- Fewer than 100 employees. Larger workforces introduce more complex exposures that go beyond what a standard BOP is designed to handle.

- Premises under 25,000 to 35,000 square feet. Larger facilities usually require standalone commercial property policies.

- Low-risk industry classification. Retail shops, small offices, restaurants, and service businesses are generally considered low-risk and are good BOP candidates.

- No significant contractual liability. If your business regularly signs contracts that shift liability to you, that can complicate standard BOP eligibility.

Here’s how common Texas industries stack up:

| Industry | BOP eligibility | Notes |

|---|---|---|

| Retail | Generally eligible | Good candidate for standard BOP |

| Hospitality/restaurants | Often eligible | Review liquor liability needs |

| Small offices | Eligible | Straightforward coverage |

| Construction | Often ineligible or limited | May need endorsements or CPP |

| Manufacturing | Limited | Depends on operations and revenue |

For construction businesses in Texas, this is a critical point. Standard BOP policies frequently exclude or limit coverage for contractors and subcontractors due to the elevated risk profile of the work. If you’re in construction, you may need to add specific endorsements or move to a Customized Property Policy (CPP), which is a more flexible commercial package built for higher-risk operations.

Hospitality businesses, like hotels and restaurants, often qualify for a BOP but should pay close attention to liquor liability. That coverage is usually not included in a standard BOP and needs to be added separately.

When you’re evaluating carriers, choosing Texas carriers that understand the state’s regulatory environment and weather risks can make a real difference in how your claims are handled.

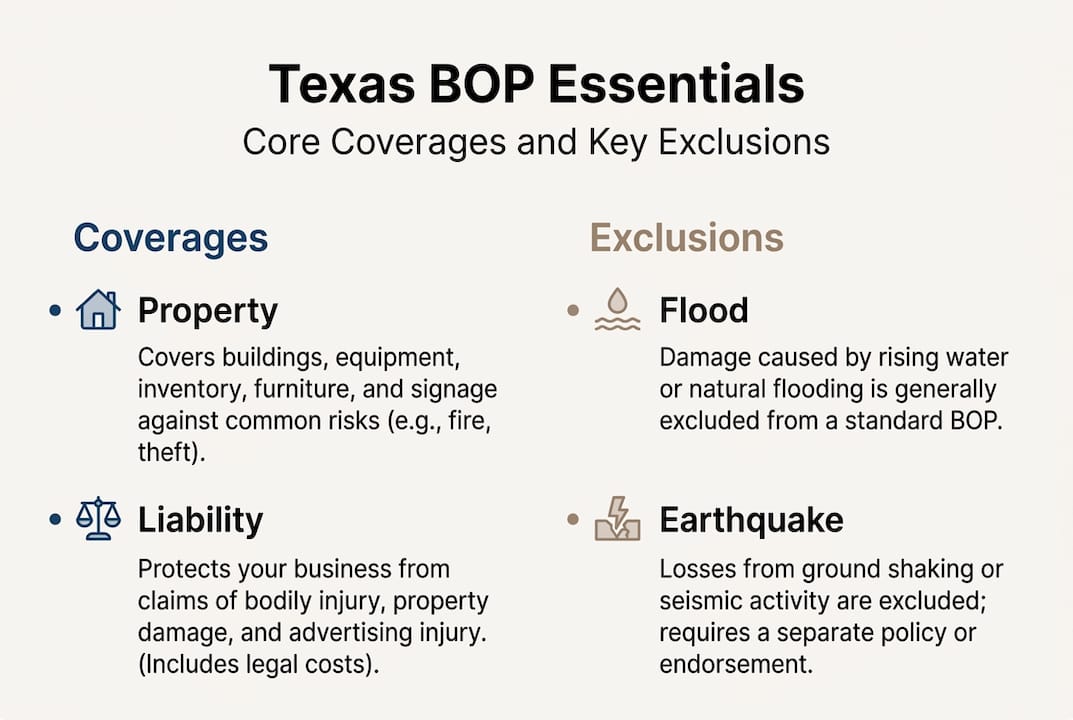

Core coverages and exclusions

Knowing what your BOP covers is only half the job. Knowing what it does not cover is equally important, and for Texas businesses, the exclusions list deserves serious attention.

What BOP covers:

- Third-party bodily injury and property damage claims (general liability)

- Damage to your building, equipment, and inventory from fire, theft, vandalism, and certain wind events (commercial property)

- Lost income and fixed operating expenses during a covered shutdown (business interruption)

- Advertising injury, including copyright infringement or defamation claims tied to your marketing

What BOP typically excludes:

- Workers’ compensation (required separately in Texas for most employers)

- Commercial auto insurance

- Professional liability, also called errors and omissions insurance

- Flood damage

- Earthquake damage

- Employee dishonesty (sometimes available as an add-on)

- Pandemics and communicable disease-related shutdowns

- Utility outages that cause business interruption

Texas-specific exclusion alert: Flood damage is one of the most common gaps for Texas businesses. Standard BOP policies do not cover flooding, even though Texas ranks among the highest-risk states for flood events. Hail damage coverage may also have limitations depending on your carrier and location. If your business is in a flood-prone area, a separate flood policy or endorsement is not optional, it’s essential.

Texas weather is genuinely unpredictable. The climate risks facing businesses in this state are growing, and standard BOP policies were not designed with West Texas hailstorms or Gulf Coast flooding in mind. Similarly, businesses in high-traffic areas should consider whether terrorism insurance is worth adding, since it’s another common BOP exclusion.

For the full BOP exclusions list and how they apply to different business types, reviewing the policy language carefully before you sign is always the right move.

Texas business risks: Customizing your BOP

Once you understand what’s excluded, the next step is filling those gaps with endorsements. An endorsement is an add-on to your existing policy that extends coverage to specific risks not included in the base package.

For Texas businesses, these endorsements are worth serious consideration:

- Flood endorsement or separate flood policy: Critical for businesses near rivers, bayous, or in low-lying areas. Standard BOP flood exclusions leave businesses fully exposed.

- Equipment breakdown endorsement: Covers mechanical or electrical failure of key equipment, like HVAC systems, commercial refrigerators, or manufacturing machinery, that isn’t covered under standard property damage.

- Cyber liability endorsement: Covers data breaches, ransomware attacks, and notification costs. If you store customer data or process payments digitally, this is not optional in 2026.

- Employee dishonesty endorsement: Protects against theft or fraud committed by employees, which is more common than most business owners expect.

- Hail and wind endorsement: In West Texas especially, standard wind coverage may carry high deductibles or sublimits. Review this carefully.

For Texas weather risks like hail, wind, and flood, adding endorsements proactively is far cheaper than paying out of pocket after a loss.

If you’re in construction or another high-risk industry, a Customized Property Policy (CPP) may be a better fit than a BOP. A CPP lets you build a policy from individual coverage components, giving you more flexibility to address the specific exposures your business faces. It’s more complex to set up, but for contractors and manufacturers, it’s often the right tool.

Hospitality businesses should also look at adding food spoilage coverage, equipment breakdown for commercial kitchen equipment, and liquor liability as standalone endorsements.

Pro Tip: Review your business interruption coverage exclusions closely every year. Many Texas business owners discovered during recent disruptions that their interruption coverage did not respond to utility outages or government-ordered closures. Knowing your gaps before a loss occurs gives you time to address them. Learning how to protect your business finances starts with understanding exactly what your policy does and does not cover.

A fresh perspective: Avoiding gaps most Texas businesses miss

After more than three decades of advising Texas businesses on commercial insurance, we’ve seen one mistake repeat itself more than any other: business owners confuse “bundled” with “covered for everything.” It’s an understandable assumption. One policy, one premium, one renewal date. It feels complete. It often isn’t.

The gaps that hurt businesses most are the ones they never thought to ask about. Flood exclusions catch restaurant owners off guard after a heavy rain event. Cyber exclusions blindside retail shops after a point-of-sale breach. Employee dishonesty claims surface in businesses where the owner trusted a long-term employee without question.

The businesses that avoid these painful surprises share one habit: they review their coverage annually with an agent who asks hard questions. Not just “did anything change?” but “what new risks did you take on this year?”

Understanding the minimum insurance requirements for Texas entrepreneurs is a starting point, not a finish line. A BOP is a strong foundation, but it needs to be built on, adjusted, and reviewed as your business grows and as Texas weather patterns evolve. Don’t wait for a claim to find your gaps.

Find the right business owners policy for your Texas business

You now know what a BOP covers, who qualifies, what’s excluded, and how to customize it for Texas risks. The next step is making sure your specific business has the right coverage in place before something goes wrong.

At Hettler Insurance Agency, we’ve been helping Texas small business owners navigate commercial insurance since 1992. As an independent agency representing over 30 top-rated carriers, we shop the market to find the right BOP or commercial package for your business at the best available price. Whether you’re a restaurant owner in Lubbock or a contractor in Midland-Odessa, we’ll make sure you understand exactly what you’re buying. Start with our guide on minimum insurance for entrepreneurs, then connect with our team at Hettler Insurance Agency for a no-pressure consultation.

Frequently asked questions

What risks aren’t covered by a standard business owners policy in Texas?

Flood, earthquake, pandemics, and utility outages are typically excluded from a standard BOP and require separate endorsements or standalone policies to fill those gaps.

How can Texas construction companies secure BOP coverage?

Most construction businesses need to add special endorsements or move to a Customized Property Policy, since standard BOP eligibility often excludes high-risk contracting operations.

Does business interruption insurance within BOP cover pandemic-related shutdowns?

No. Business interruption coverage in a standard BOP excludes pandemics and utility outages, so additional policies or endorsements are needed for those specific scenarios.

Can I add flood coverage to my BOP for my Texas business?

Flood is excluded from standard BOP, but you can add a flood endorsement or purchase a separate policy through a specialized insurer to cover that Texas weather risk.

What’s the main advantage of BOP for small businesses?

Bundling general liability, commercial property, and business interruption into one policy delivers a 15-30% discount compared to buying each coverage separately, while simplifying your policy management.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: What risks aren’t covered by a standard Business Owners Policy in Texas?

Q2 ?: Who qualifies for a Business Owners Policy in Texas?

Q3 ?: How can Texas construction companies secure BOP coverage?

Q4 ?: Does business interruption coverage in a BOP cover pandemic-related shutdowns?

Q5 ?: What’s the main advantage of a BOP for Texas small businesses?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com