TL;DR:

- Texas minimum auto insurance often leaves critical coverage gaps, increasing financial risk.

- Comprehensive coverage is vital in Texas due to frequent hailstorms and weather-related damages.

- Understanding policy exclusions and proper coverage limits helps Texas drivers avoid costly mistakes.

Most Texas drivers assume their auto insurance has them covered — until a hailstorm totals their car or a fender-bender leaves them with a five-figure bill they didn’t expect. The truth is, the minimum policy required by Texas law often leaves significant gaps, and those gaps get expensive fast. Whether you’re buying your first policy or reassessing what your family carries, understanding what a personal auto policy actually covers — and what it doesn’t — is one of the most important financial decisions you’ll make as a Texas driver.

Table of Contents

- What is a personal auto policy?

- Texas insurance requirements: Understanding your minimums and more

- Coverage options to protect your family and finances

- What first-time buyers and Texas families should expect

- Common policy exclusions and costly mistakes to avoid

- Why following the crowd on auto insurance can cost Texans dearly

- Find the right auto policy for your needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Texas minimum coverage explained | State law sets liability minimums, but more coverage is often smart for full protection. |

| Weather risks require comprehensive | Texas drivers face high hail and flood risk, making comprehensive coverage essential. |

| First-time buyers checklist | Be prepared with ID, vehicle info, and know that lenders usually require full coverage. |

| Watch out for common exclusions | Business use and personal property are not covered under standard personal policies. |

| Smart coverage saves money and stress | Choosing the right limits and add-ons can prevent costly out-of-pocket surprises. |

What is a personal auto policy?

A personal auto policy (PAP) is a contract between you and your insurance company that covers private, non-commercial use of your vehicle. It protects you financially if you’re in an accident, your car is damaged, or someone is injured while you’re driving. The key word here is “personal.” This policy is designed for everyday driving, not business errands, delivery runs, or rideshare trips.

A standard PAP includes several types of coverage, each serving a different purpose:

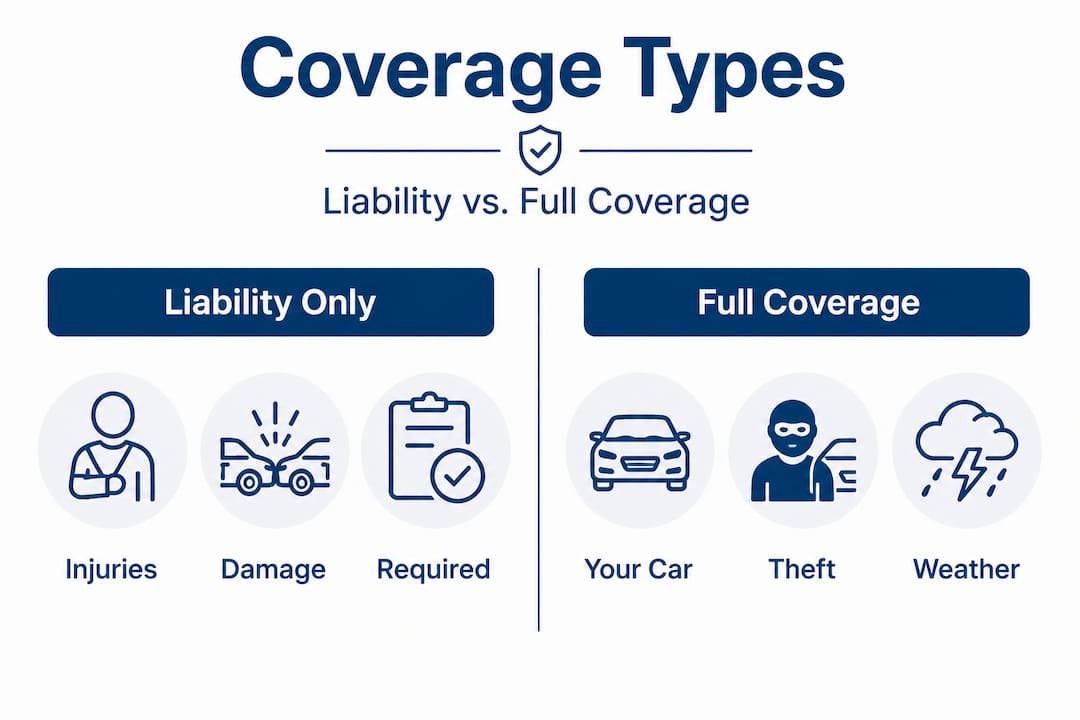

- Liability coverage: Pays for injuries or property damage you cause to others in an accident.

- Collision coverage: Pays to repair or replace your vehicle after a crash, regardless of fault.

- Comprehensive coverage: Covers non-collision damage like hail, theft, flooding, or fire.

- Uninsured/underinsured motorist coverage: Protects you when the at-fault driver has no insurance or not enough.

- Medical payments (MedPay): Covers medical expenses for you and your passengers after an accident.

What your PAP does not cover is just as important. Personal belongings inside your car are not protected under auto insurance — that falls under your homeowners or renters policy. Business use of your vehicle, including delivery driving or transporting clients, is typically excluded. If you drive for Uber or Lyft, you need to understand rideshare policy limits because your personal policy may not protect you between rides.

Know this: Texas law sets the floor, not the ceiling. Meeting the minimum requirement means you’re legal — it doesn’t mean you’re protected.

Texas requires minimum liability of 30/60/25: $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. For many accident scenarios in Texas, those limits run out fast.

Texas insurance requirements: Understanding your minimums and more

With the basics in mind, it’s crucial to understand exactly what Texas law mandates and why many families and drivers go well beyond the bare minimum.

The 30/60/25 rule sounds like solid protection until you put it in context. A single trip to a Texas emergency room can easily exceed $30,000. If you rear-end another vehicle and injure two people, your per-accident limit of $60,000 may not cover both victims’ medical bills. And $25,000 in property damage won’t replace a newer truck or SUV. You could be personally responsible for the difference.

Texas average full coverage premiums run roughly $110 to $229 per month, with rates varying widely based on your age, ZIP code, driving record, and the carrier. Drivers with clean records in the 28 to 55 age range often find better rates. Here’s a general snapshot of what different drivers in Texas might pay:

| Driver profile | Liability only (est./mo) | Full coverage (est./mo) |

|---|---|---|

| Age 28, clean record, Lubbock | $75 to $110 | $130 to $180 |

| Age 40, one minor violation, Dallas | $100 to $145 | $175 to $230 |

| Age 55, clean record, Midland | $70 to $105 | $125 to $170 |

| Age 35, financed vehicle, West Texas | Required full coverage | $160 to $220 |

These are estimates, but they illustrate an important point: full coverage is often more affordable than people assume, especially when weighed against the cost of a total loss.

Here’s what affects your rate most:

- ZIP code: Hail-prone areas like Lubbock and Midland carry higher comprehensive premiums.

- Driving record: Accidents and violations raise your rate significantly.

- Vehicle type: Newer or more expensive vehicles cost more to insure.

- Coverage limits chosen: Higher limits mean higher premiums, but also far better protection.

If you have a financed vehicle, your lender will require full coverage. That’s non-negotiable. Understanding liability limit protection is critical before you decide what limits to carry.

Pro Tip: Review your liability limits every time you buy or finance a new vehicle. What made sense on a paid-off car from 2015 may leave you dangerously exposed when you’re driving something worth $40,000.

Explore your full coverage options before assuming you can’t afford them. You may be surprised.

Coverage options to protect your family and finances

Knowing what you’re legally required to carry is just the start. Here’s how different coverage options can make a huge difference, especially for Texas families facing weather risks.

Texas is not a gentle place for vehicles. Texas leads the nation in hail activity, with 878 hailstorms recorded in 2024 alone. That’s not a typo. Nearly 900 hailstorms in a single year. Lubbock, Midland, and Amarillo sit squarely in what storm chasers call “Hail Alley,” and if you’ve lived here long enough, you’ve seen what a single storm can do to a parking lot full of cars.

Here’s how the three main coverage types compare in real-world terms:

| Coverage type | What it pays for | When you need it |

|---|---|---|

| Liability | Other people’s injuries and property damage | Required by Texas law |

| Collision | Your car after a crash (any fault) | Financed vehicles, newer cars |

| Comprehensive | Hail, flood, theft, fire, animal strikes | Strongly recommended in Texas |

Consider this scenario: A hailstorm rolls through Lubbock in May. Your neighbor has liability-only coverage. You carry comprehensive. Both vehicles take $8,000 in damage. Your neighbor pays out of pocket. You file a claim, pay your deductible, and drive to the repair shop. That’s the difference comprehensive makes.

Here’s how to think through your coverage decisions:

- Check your vehicle’s value. If your car is worth less than $4,000, dropping collision may make financial sense. Comprehensive is a different story — hail doesn’t care how old your car is.

- Consider your deductible. A higher deductible lowers your premium but raises your out-of-pocket cost when you file a claim. Find the balance that fits your budget.

- Ask about windshield and hail coverage add-ons. Some policies offer zero-deductible glass coverage, which is valuable in West Texas.

- Look at uninsured motorist coverage. Texas has a significant number of uninsured drivers. This coverage protects you when the other driver doesn’t have insurance.

- Bundle your policies. Insuring multiple vehicles or combining auto and home policies often unlocks meaningful discounts.

Pro Tip: Families with two or more vehicles should always ask about multi-car discounts. Safe driver discounts are also available through many carriers and can reduce your annual premium by 10% to 25%.

What first-time buyers and Texas families should expect

So how do you put all this into practice? Here’s what Texas families and new buyers should expect from start to finish and how to avoid the biggest mistakes.

Buying your first auto policy can feel overwhelming, but the process is straightforward when you know what to bring and what to ask. First-time buyers in Texas should expect liability-only coverage to run $95 to $250 per month, while full coverage typically ranges from $180 to $400 depending on your age, vehicle, and location. Lenders always require full coverage for financed vehicles.

Here’s a checklist to get started:

- Gather your documents. You’ll need a valid Texas ID or driver’s license, your vehicle’s VIN (Vehicle Identification Number), current odometer reading, and any prior insurance history.

- Know your vehicle’s value. This determines whether full coverage makes financial sense.

- Decide on your deductible. Most buyers choose $500 or $1,000. A higher deductible lowers your monthly premium.

- Ask about weather-related add-ons. Comprehensive coverage is the baseline, but ask specifically about hail, glass, and flood endorsements (add-ons that expand your coverage).

- Compare at least three quotes. Rates vary significantly between carriers. An independent agent can do this comparison for you at no extra cost.

- Review your policy documents. Read the declarations page — it summarizes your coverage, limits, and deductibles in plain language.

Remember: The cheapest policy is not always the best policy. A $20 monthly savings could mean a $10,000 out-of-pocket expense after a storm.

Families should also think about auto insurance tips specific to Texas, including how to handle teen drivers on your policy and when to add or remove vehicles. And if you’re trying to balance cost with protection, look into deductible savings strategies that let you carry strong coverage without overpaying.

Pro Tip: Shopping your policy at renewal every two to three years is one of the simplest ways to avoid overpaying. Loyalty doesn’t always pay in the insurance world. An independent agent shops multiple carriers on your behalf, which saves you time and often saves you money.

Common policy exclusions and costly mistakes to avoid

Before you shop for or adjust your coverage, be sure to understand the hidden gaps. These are where even careful buyers get caught off-guard.

Your personal auto policy is not a catch-all. Several situations fall outside standard coverage, and not knowing about them ahead of time can be a very expensive lesson.

Here are the most common exclusions Texas drivers encounter:

- Business use: If you use your personal vehicle to transport clients, make deliveries, or conduct business operations, your PAP likely won’t cover an accident that occurs during that use. You need a commercial auto policy.

- Rideshare and delivery apps: Driving for Uber, Lyft, DoorDash, or similar platforms creates a coverage gap. Your personal policy typically excludes this use, and the app company’s coverage has limits depending on what phase of the trip you’re in.

- Personal property inside your vehicle: A laptop stolen from your back seat is not an auto insurance claim. That goes through your homeowners or renters policy.

- Intentional damage: Any damage you cause on purpose is excluded from coverage.

- Mechanical breakdown: Wear and tear, engine failure, and mechanical issues are not covered under auto insurance. That’s what a warranty or mechanical breakdown policy covers.

Regarding temporary vehicles, Texas Insurance Code provisions specify that temporary vehicles (like a loaner car) typically receive primary liability coverage from your policy, but not necessarily excess coverage or comprehensive and collision protection. This is a detail many drivers overlook when they’re in a rental or loaner situation.

Important: Always call your agent before you sign a car rental agreement or take a loaner vehicle. Ask specifically what your policy covers in that situation.

Choosing the wrong deductible is another costly mistake. A low deductible sounds appealing until you realize you’re paying significantly more in premiums every month. Run the math: if your deductible is $250 lower but your annual premium is $300 higher, you’re paying more for the privilege of a smaller out-of-pocket cost you may never use.

Why following the crowd on auto insurance can cost Texans dearly

With all the details covered, let’s step back and share some hard-won lessons from what we see at Hettler Insurance every year.

Here’s what we’ve observed after more than 30 years of serving Texas drivers: the people who get hurt financially are almost never the ones who made reckless decisions. They’re the ones who made reasonable-sounding decisions without full information. They dropped comprehensive on an older car to save $40 a month. Then a hailstorm totaled it, and they had no coverage. They chose minimum liability because the law only required it. Then a serious accident left them personally liable for damages that exceeded their limits.

Liability-only coverage is genuinely risky in a state that sees hundreds of hailstorms per year and has one of the highest rates of uninsured drivers in the country. The math on dropping comprehensive rarely works out the way people expect, especially in Lubbock and West Texas where hail season is a real annual threat.

We understand that budgets are real. Not everyone can afford the maximum coverage on every vehicle. But the decision of what to drop and when should be made with a clear understanding of the risks, not just the monthly savings. If you’re in a financed vehicle, you have no choice. If you own your car outright and it’s worth less than $6,000, dropping collision might be reasonable. But dropping comprehensive in Hail Alley? That’s a gamble most Texans lose eventually.

The weather damage risks in West Texas are not theoretical. They’re annual. Plan accordingly.

Find the right auto policy for your needs

If you’re ready to protect your family and your finances, expert help is just a click away.

At Hettler Insurance Agency, we’ve been helping Texas drivers find the right coverage since 1992. As an independent agency, we represent over 30 top-rated carriers, which means we shop the market for you and find the best fit at the best price. No pressure. No guesswork. Just real guidance from a team that knows Texas insurance inside and out.

Whether you’re a first-time buyer trying to understand Texas minimum insurance requirements, a family looking to add weather protection, or a driver who just wants to make sure they’re not overpaying, we’re here to help. Ron and Meghan Hettler are both Certified Insurance Counselors (CIC), the gold standard credential in the industry, and they bring that expertise to every client conversation. Visit Hettler Insurance Agency to get your free quote or call us to talk through your options today.

Frequently asked questions

What is the minimum coverage required for auto insurance in Texas?

Texas law requires at least 30/60/25: $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage liability.

Does personal auto insurance cover hail and flood damage in Texas?

Only comprehensive coverage protects you from hail and flood damage. Texas leads the nation in hailstorms, with 878 recorded in 2024, making comprehensive especially important for Texas drivers.

How much does auto insurance typically cost for a first-time buyer in Texas?

Monthly rates for first-time buyers range from $95 to $250 for liability-only coverage and $180 to $400 for full coverage, depending on age, location, and vehicle type.

Will my personal auto policy cover me if I use my car for Uber or delivery?

No. Most personal auto policies exclude rideshare and delivery use entirely. You need a commercial or rideshare-specific policy to fill that gap, as business use exclusions are standard in personal auto contracts.

What are common exclusions in a personal auto policy?

Standard exclusions include business and delivery use, personal belongings inside the vehicle, and certain temporary vehicle scenarios. Deductibles also apply to comprehensive and collision claims, which surprises many first-time buyers.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com