TL;DR:

- The role of compliance in Texas contractor insurance requires active management of coverage, endorsements, and proof at every project stage.

- Non-compliance can lead to bid disqualification, contract termination, license suspension, and increased liability.

- Proactive oversight, proper documentation, and understanding project-specific requirements give contractors a competitive advantage.

Mastering the role of compliance in Texas contractor insurance. Most Texas contractors assume they’re covered just because they bought a policy. That assumption has cost businesses everything. Insurance compliance isn’t a checkbox you handle once and forget. It’s an active, ongoing responsibility that determines whether you get paid, keep your license, and win the next contract. Texas has some of the most flexible contractor insurance rules in the country, but that flexibility cuts both ways. Without a clear understanding of what compliance actually requires, including the right limits, endorsements, and proof documents, you can lose a bid before the first tool is unpacked.

Table of Contents

- What does insurance compliance mean for Texas contractors?

- Standard insurance requirements and how compliance is verified

- What happens when you’re not compliant?

- Best practices for staying compliant (and competitive)

- Why real compliance is the contractor’s secret edge in Texas

- Simplify compliance, protect your business, and win more contracts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Compliance isn’t optional | Most Texas contracts require meeting specific coverage limits, even if state law doesn’t. |

| Proof is everything | Always provide up-to-date COIs and policy endorsements to secure jobs and protect your business. |

| Non-compliance is costly | Missed compliance can lead to lost income, revoked licenses, and personal liability. |

| Stay proactive | Review requirements, check your documentation, and monitor renewals to avoid preventable problems. |

| Expert help pays off | Insurance specialists can make compliance straightforward and help you win more contracts. |

What does insurance compliance mean for Texas contractors? (mastering the role of compliance in Texas contractor insurance)

Now that you know why compliance matters, let’s break down what it really means in Texas.

“Compliance” sounds straightforward, but it’s more layered than most contractors expect. Contractor insurance compliance involves obtaining specified coverages at minimum limits, naming certain parties as additional insureds, and providing proof via Certificates of Insurance (COI) before work begins. That proof is then verified through pre-qualification, contract execution, and ongoing monitoring throughout the project.

In other words, you need the right coverage, at the right limits, documented correctly, and updated whenever anything changes. Getting one element wrong can still mean non-compliance, even if you’ve been paying premiums for years.

Texas has a reputation for regulatory independence, and the role of compliance in Texas contractor insurance is no exception. Most states mandate workers’ compensation across the board. Texas does not. Private employers in Texas are not required by state law to carry workers’ comp, but here’s where contractors get into trouble: most commercial contracts, public works projects governed by Government Code Chapter 2253, and licensing boards like the Texas Department of Licensing and Regulation (TDLR) require it anyway. So the law won’t force your hand, but your clients and the state boards that control your license will.

It’s also worth understanding how requirements shift based on project type and the license you hold. For a helpful look at how this plays out in specialized trades, check out the insurance rules for HVAC contracts in Texas.

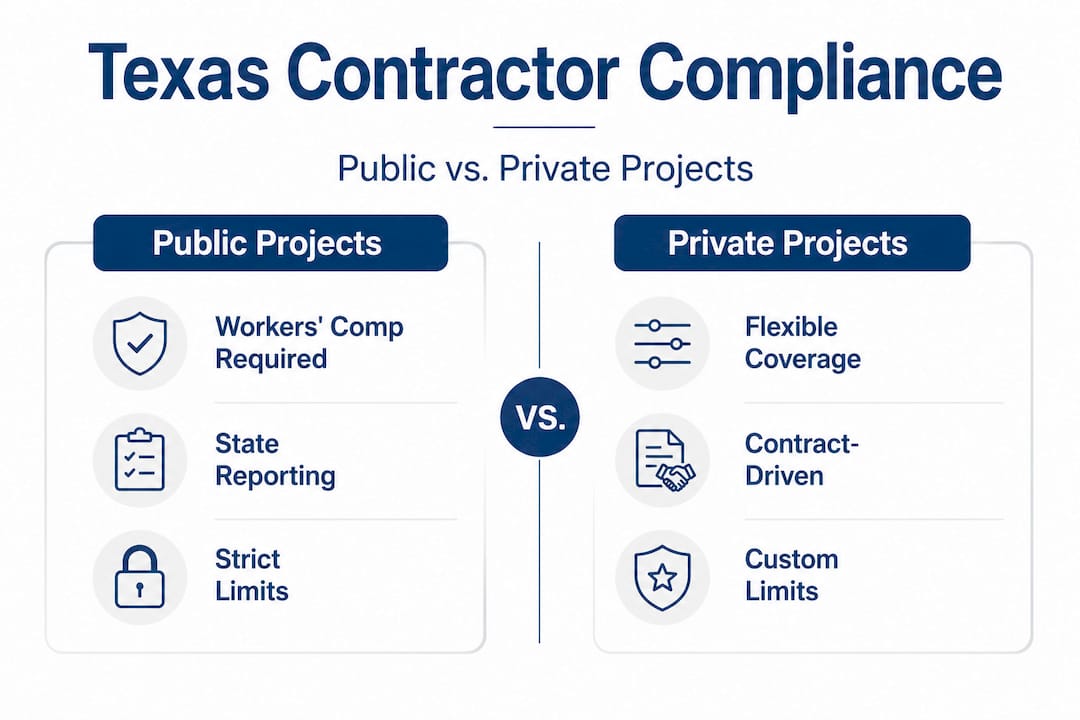

How Texas compliance differs: Public vs. private projects

| Factor | Public projects | Private projects |

|---|---|---|

| Workers’ comp required | Yes, typically mandated | Set by contract, not law |

| Minimum CGL limits | Often $1M or higher by statute | Varies by client or GC |

| Bonding requirements | Statutory bonds required over $25k | Depends on contract terms |

| Additional insured status | Almost always required | Commonly required |

| COI monitoring | Strict and ongoing | Varies by owner/GC |

This table makes one thing clear: public and private projects operate by different rules. You can’t assume one coverage setup works for both.

Key compliance elements every Texas contractor needs to know:

- Coverage type: You must have the right policy type, not just any policy.

- Coverage limits: Minimum limits must match or exceed what the contract specifies.

- Endorsements: These are additions to your policy that modify or extend coverage. A COI alone won’t confirm these exist.

- Additional insured status: Your client or general contractor (GC) may need to be listed on your policy directly.

- Proof documents: A COI is the standard proof, but endorsement copies are often required too.

Standard insurance requirements and how compliance is verified

With the definition covered, here are the coverage specifics and how compliance checks work in practice for Texas contractor insurance.

Typical minimum limits across Texas commercial contracts include Commercial General Liability (CGL) at $1 million to $2 million per occurrence, Workers’ Compensation at statutory limits where required, and Commercial Auto at $1 million combined single limit (CSL). These aren’t suggestions. They’re floors.

For licensed trades, the numbers are set by the state licensing board. TDLR mandates that licensed electricians and HVAC contractors carry at least $300,000 per occurrence in CGL coverage with a $600,000 aggregate, and licensed plumbers must carry $300,000 in CGL. If your policy doesn’t hit those numbers, your license is at risk. Full stop.

Compliance is verified at multiple points during any project:

- Pre-bid or pre-qualification: Before you even submit a bid, many GCs and government agencies require proof of current coverage. No COI, no bid.

- Contract execution: When a contract is signed, the hiring party will typically collect updated COIs and may require endorsement copies confirming additional insured status and waiver of subrogation.

- Project start: Some projects require confirmation that coverage is active before mobilization. A lapsed policy discovered on day one can shut you down immediately.

- Ongoing monitoring: Long-term projects may require updated COIs at policy renewal intervals. If your policy renews mid-project, you need to send updated documentation without waiting to be asked.

- Post-project closeout: Completed operations coverage may be required, especially for trade contractors whose work could cause latent damage discovered months or years later.

Pro Tip: Never rely solely on the COI to confirm compliance. Make sure to know the role of compliance in Texas contractor insurance. A COI is a snapshot of what your insurance agent reported at that moment. It doesn’t guarantee the endorsements are actually attached to your policy. Always request endorsement documents directly from your insurer and verify that the language in those endorsements matches what the contract requires. This one habit has saved contractors from costly disputes.

When edge cases create unexpected exposure

Texas construction compliance creates several tricky situations that catch contractors off guard. Non-subscribing employers (those who opt out of workers’ comp) face unlimited liability in workplace injury lawsuits and cannot use common-law defenses like contributory negligence. Public projects require statutory payment and performance bonds for contracts over $25,000. TxDOT projects come with their own specific requirements, including mandatory WC, CGL, and auto coverage along with a waiver of subrogation. Self-insured contractors must submit financial proof to substantiate their self-insured status. And if your coverage lapses for even a single day, you risk license suspension or revocation from the applicable state board.

That last point deserves extra weight. A one-day coverage gap during renewal season can trigger consequences that take months to resolve, even if you had coverage the day before and the day after.

What happens when you’re not compliant?

Now you know the requirements concerning the role of compliance in Texas contractor insurance, next comes understanding the potential fallout from falling short.

Non-compliance isn’t just a paperwork headache. It directly affects your ability to work, get paid, and stay in business. Consequences of non-compliance for Texas contractors include bid disqualification, contract termination, payment withholding, and licensing suspension. When a subcontractor is uninsured or underinsured, the GC or project owner often absorbs that liability directly. That means GCs are highly motivated to enforce compliance requirements and will cut ties fast with subs who can’t prove coverage.

Common consequences of non-compliance include:

- Bid disqualification: You lose the job before it starts.

- Contract termination: You lose the job after work has already begun.

- Withheld payments: Owners and GCs can legally withhold payment until compliance is confirmed.

- License suspension or revocation: Lapsed coverage leads directly to action by TDLR or the applicable state board.

- Direct liability exposure: Without workers’ comp, one workplace injury can result in an unlimited judgment against your business.

- Increased premiums or uninsurability: A compliance failure on record can make it harder and more expensive to get coverage later.

- Reputation damage: Word travels fast in the Texas contracting world. Losing a contract over insurance issues follows you.

“When a subcontractor lacks required insurance, the liability exposure shifts directly to the general contractor or project owner. That creates an immediate incentive to terminate the non-compliant party, regardless of how far along the project is.”

The risks related to insurance and contract obligations extend further than most contractors initially realize. A vehicle used on a job site and not listed on a commercial auto policy can also create compliance gaps. Understanding how auto liability intersects with contract work is just one more reason every coverage type matters when you’re working under contract.

Consider a real-world scenario: A small HVAC subcontractor in West Texas wins a commercial retrofit job. Midway through, the GC audits subcontractor COIs and discovers the HVAC company’s general liability policy renewed two weeks prior but the updated COI was never submitted. The GC stops work, withholds two progress payments, and requires written confirmation from the insurer before allowing the crew back on site. The delay costs the subcontractor more in lost labor and overhead than the two payments combined. This kind of situation happens constantly, and it’s entirely preventable.

Best practices for staying compliant (and competitive)

After highlighting risks, here’s how proactive, smart contractors can stay protected, contract-ready, and ahead of the competition.

Staying compliant requires more than buying the right policy. It requires actively managing your coverage, your documentation, and your relationships with both clients and your insurance agent. Always verify that your endorsements match your policy, not just the COI. Work with carriers rated at least B+ by A.M. Best, which is an independent financial strength rating system. For small businesses, bundling coverages through a Business Owners Policy (BOP) is a smart, cost-effective approach, though flood coverage is typically excluded and should be addressed separately if needed.

Texas’s no-WC-mandate structure can feel like freedom, but it actually increases risk compared to states where coverage is forced. Contractors who proactively carry workers’ comp even when not legally required are better positioned for contract awards and better protected if something goes wrong.

Here is a step-by-step compliance checklist for Texas contractors:

- Review every contract before signing. Look specifically for the insurance requirements section. Note required coverage types, minimum limits, additional insured language, and endorsement requirements.

- Confirm your existing policy meets those requirements. Don’t assume. Call your agent and walk through the specifics.

- Request endorsements in writing. If the contract requires additional insured status or a waiver of subrogation, get those endorsements added before the project starts.

- Order a new COI that reflects all required parties. Make sure the certificate lists the correct project name, entity names, and coverage details.

- Set a renewal reminder at least 60 days before your policy expires. This gives you time to shop, update, and submit new documentation before any gap occurs.

- Submit updated COIs immediately after renewal. Don’t wait for the client to ask. Send it proactively.

- Keep digital copies of all COIs, endorsements, and policy pages. Organize them by project and year for fast access.

- Audit your coverage after any major business change. New employees, new equipment, new trade work, or new contract types all affect your coverage needs.

Pro Tip: Bundling your general liability, commercial auto, and property coverage under one carrier or a BOP can lower your overall premium while simplifying renewal management. Fewer renewal dates mean fewer opportunities for a coverage gap to slip through.

Why real compliance is the contractor’s secret edge in Texas

Here’s a perspective you won’t often hear in the standard conversation about the role of compliance in Texas contractor insurance: the contractors who struggle most in Texas are rarely the ones who lack skill. They’re the ones who treat insurance as an afterthought. And in a state where the law gives private employers unusual flexibility, that attitude quietly eliminates opportunity after opportunity.

The approach to exceeding minimum requirements is what separates the contractors who build lasting businesses from those who stay stuck chasing smaller, less desirable jobs. Here’s why. Large commercial clients, property managers, and institutional owners don’t just want the lowest bid. They want a contractor they can trust to show up clean on every compliance check, every time. When you proactively deliver properly endorsed COIs, carry higher limits voluntarily, and communicate changes without being asked, you become the easy choice. That trust compounds into repeat business.

Texas’s flexibility on workers’ comp is genuinely unusual. Most states remove the choice entirely. That means Texas contractors who opt in voluntarily signal something important to the market: they take risk seriously. They’re not looking for the bare minimum. They’re building a business that can absorb the unexpected. We’ve worked with hundreds of contractors across West Texas and Lubbock over the years at Hettler Insurance, and the pattern is consistent. The contractors growing their client lists and winning better contracts are almost never the ones cutting coverage corners.

The uncomfortable truth is that the “bare minimum” compliance strategy is actually more expensive over time. One withheld payment, one suspended license, one lawsuit from an injured uninsured worker, and you’ve spent far more than you ever saved on premiums. Compliance, done right and done proactively, is an investment in access to better jobs, better clients, and a more resilient business.

Simplify compliance, protect your business, and win more contracts

Ready to put compliance into action for your business?

Keeping up with contract insurance requirements takes real attention and the right guidance. You need someone on your side who knows the role of compliance in Texas contractor insurance. Whether you’re a solo HVAC technician, a growing electrical firm, or a general contractor managing multiple subs, understanding your minimum coverage obligations is the starting point for protecting everything you’ve built.

At Hettler Insurance Agency in Lubbock, we’ve been helping Texas contractors navigate exactly these situations since 1992. As an independent agency with access to over 30 top-rated carriers, we don’t push one product. We find the right fit. Our team reviews contract requirements, confirms your endorsements are properly structured, and makes sure every COI you submit is accurate and complete. When your policy renews, we’re already on it. Visit Hettler Insurance Agency to speak with a licensed agent who understands the role of compliance in Texas contractor insurance inside and out. Call before you sign. It’s the simplest risk management move you can make.

Frequently asked questions

Is workers’ comp required for all Texas contractors?

No, Texas does not require workers’ comp for private employers, but many contracts and public jobs demand it as a condition of compliance and contract award.

What’s the most common insurance minimum for commercial contracts?

Most Texas contracts require at least $1 million in commercial general liability (CGL) coverage per occurrence, though higher limits are common on larger commercial projects.

How often do contractors need to provide Certificates of Insurance?

You typically need to provide COIs before work begins, when contracts are signed, and any time your insurer, coverage type, or policy limits change during an active project.

What happens if coverage lapses during a contract?

Lapsed coverage can immediately trigger license suspension or revocation by the applicable state board and put all pending project payments at risk until compliance is restored. So, you gotta know the role of compliance in Texas contractor insurance.

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com