TL;DR summary:

- Young Texas families average just 3.5x their income in life insurance — experts recommend 10 to 15 times to protect a mortgage, dependents, and long-term family security.

- Term life is the workhorse for Texas homeowners — a 40-year-old can lock in $500,000 of coverage for roughly $25–$45 a month, while whole life costs 8 to 15 times more and serves estate-planning roles.

- Employer group plans, mortgage protection products, and skipping the stay-at-home parent leave dangerous gaps — an independent agent can right-size coverage that pairs with your homeowners, windstorm, and flood policies.

Many Texas homeowners assume their insurance policies cover every major financial threat, including storm damage, flooding, and even mortgage payoff after a disaster. That assumption can leave families dangerously exposed. Young families are underinsured, carrying only about 3.5 times their income in coverage when experts recommend 10 to 15 times. Life insurance is not a property protection tool. It is a financial safety net for the people who depend on your income. This guide breaks down exactly what life insurance covers, how it works alongside homeowners insurance, and what Texas families need to know to avoid costly gaps.

Table of Contents

- What does life insurance actually cover?

- Types of life insurance: Which fits Texas homeowners and families?

- How life insurance complements homeowners and property coverage in Texas

- Common gaps, mistakes, and Texas nuances

- Take the next step: Protect your Texas family

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Life insurance purpose | It protects your family’s financial security by replacing lost income, paying off debts, and covering critical expenses. |

| Policy options | Term life is affordable and fit for temporary needs; whole life is expensive but suited for estate planning in Texas. |

| Texas-specific gaps | Homeowners insurance covers property risks, but high property taxes and underinsurance are unique local challenges. |

| Common mistakes | Most young Texas families are underinsured and overlook stay-at-home parent coverage. |

| Action step | Pair the right life insurance with your homeowners and specialty policies for complete protection. |

What does life insurance actually cover?

Now that we’ve addressed common confusion, let’s clarify what life insurance covers and what Texas homeowners should expect.

Life insurance has one core job: replace your income when you are gone. It is not designed to repair your roof after a hailstorm or reimburse flood damage to your foundation. Those risks belong to homeowners and flood insurance policies. Life insurance steps in for your family’s financial survival after you pass away.

Here is what a life insurance payout can cover:

- Mortgage payoff: Your family keeps the home without scrambling for monthly payments.

- Outstanding debts: Car loans, credit cards, and personal loans do not transfer to your survivors automatically, but the estate must settle them.

- Education costs: College tuition and school expenses for your children.

- Final expenses: Funeral and burial costs average $7,000 to $12,000 in Texas.

- Daily living expenses: Groceries, utilities, and childcare for years after your death.

As the life insurance statistics confirm, life insurance provides financial support for dependents and pays off debts, education, and funeral costs. It is a replacement for your earning power, not your property.

Important: Life insurance does not cover property risks like hurricanes and floods. If a storm destroys your home, your homeowners policy and a separate flood policy handle that loss. Life insurance handles what happens to your family’s finances if you are no longer there.

When you think about life insurance for loved ones, the question is simple: if your income disappeared tomorrow, could your family pay the mortgage, keep the lights on, and plan for the future? If the answer is no, you need coverage. Use a structured approach to calculating life insurance needs based on your income, debts, and dependents before choosing a policy.

Types of life insurance: Which fits Texas homeowners and families?

| Feature | Term life | Whole life |

|---|---|---|

| Coverage period | 10, 20, or 30 years | Lifetime |

| Monthly cost (age 40, $500k) | $25 to $45 | $300 to $500 |

| Cash value | No | Yes |

| Best for | Mortgage and income protection | Estate planning, wealth transfer |

| Complexity | Simple | More complex |

.

Understanding what life insurance covers leads us to choosing the right policy for your needs.

Two policy types dominate the market for Texas families: term life and whole life. Each serves a different purpose, and the wrong choice can cost you thousands of dollars over time.

Term life insurance is straightforward. You pay a fixed premium for a set number of years, and your family receives the death benefit if you pass away during that term. Term life is affordable and matches mortgage terms well, making it the practical choice for most Texas families raising children and paying down a home loan.

Whole life insurance costs significantly more, often 8 to 15 times higher than term. However, it builds cash value over time and lasts your entire life. Whole life is useful for estate planning in Texas because it bypasses probate, offers creditor protection, and can transfer wealth to heirs efficiently. If you own investment properties or have a high-value estate, whole life deserves a closer look.

Here is a quick breakdown of who benefits from each:

- Term life fits you if: You have a mortgage, young children, and want maximum coverage at the lowest cost.

- Whole life fits you if: You have estate planning goals, want lifelong coverage, or need a tax-advantaged savings vehicle.

- Universal life sits between the two, offering flexible premiums and some cash value growth.

Pro Tip: Most Texas families with a mortgage and kids under 18 are better served by a 20 or 30-year term policy. Lock in your rate while you are young and healthy. Revisit whole life options once your mortgage is paid down and estate planning becomes a priority.

When choosing your Texas insurance carrier, compare financial strength ratings and policy flexibility. And remember, life insurance is separate from the replacement cost coverage on your homeowners policy. Both matter. Neither replaces the other.

How life insurance complements homeowners and property coverage in Texas

Once you’ve picked the right life insurance policy, it’s crucial to see how it fits with your other insurance protection.

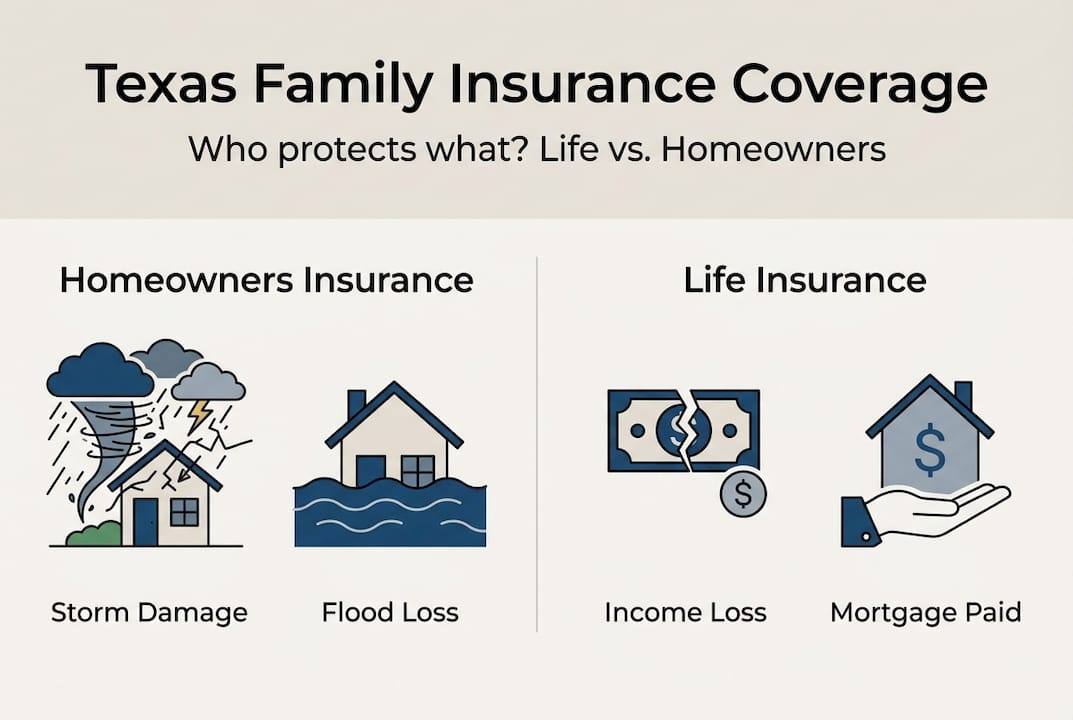

Texas homeowners carry two very different financial risks. The first is property damage from storms, hail, wind, and flooding. The second is income loss if the primary earner dies. These are separate problems that require separate solutions.

Here is how the two coverage types divide responsibilities:

Homeowners insurance covers property risks like hurricanes and floods, while life insurance supports liquidity for mortgage and property tax obligations if income is lost. In Texas, where average annual homeowners premiums run between $3,291 and $4,000 and life insurance averages $408 per capita annually, both are essential budget items.

Texas-specific factors make this pairing especially important:

- High property taxes: Texas has no state income tax, but property taxes average 1.6% to 2.5% of home value annually. If your income disappears, those bills do not stop.

- Coastal and storm exposure: Homes near the Gulf Coast need windstorm and flood riders that standard homeowners policies do not include.

- Rapid home value appreciation: As your home’s value grows, so does the financial burden on your family if you are gone.

Key point: Life insurance does not replace your home after a storm. But it can prevent your family from losing the home after losing you.

Review your homeowners policy increases annually to make sure your coverage keeps pace with your home’s value. And before you buy any policy, prepare for homeowners insurance by documenting your property and understanding what your current coverage actually includes.

| Risk | Covered by homeowners insurance | Covered by life insurance |

|---|---|---|

| Hurricane or windstorm damage | Yes (with endorsement) | No |

| Flood damage | Separate flood policy needed | No |

| Mortgage payoff after death | No | Yes |

| Income replacement for family | No | Yes |

| Property tax obligations | No | Indirectly (via death benefit) |

Common gaps, mistakes, and Texas nuances

Even with the right insurances, mistakes and local factors can leave families exposed. Here’s how to avoid those gaps.

Texas families make predictable mistakes when it comes to life insurance. Knowing them in advance puts you ahead of most homeowners in your neighborhood.

- Relying only on employer group life insurance. Most employer policies cover only 1 to 2 times your salary, which is not nearly enough for a family with a mortgage and children. It also disappears when you change jobs.

- Skipping coverage for stay-at-home parents. A stay-at-home parent contributes real economic value. Childcare, household management, and daily logistics cost real money to replace. Do not leave that gap open.

- Buying mortgage protection insurance instead of term life. Mortgage protection policies are narrowly designed and often cost more than a comparable term policy. Term life is more flexible and usually a better value.

- Underestimating coverage needs. Young Texas families average only 3.5 times their income in coverage. The recommended amount is 10 to 15 times. That gap is significant.

- Waiting too long to buy. Premiums rise with age and health changes. A 35-year-old pays far less than a 45-year-old for the same coverage.

Pro Tip: Pair your life insurance with flood and windstorm coverage on your home policy. Life insurance protects your family’s income. Flood and windstorm coverage protects the asset itself. Together, they close the two biggest financial gaps Texas homeowners face.

One often-overlooked statistic: employer group coverage at 1 to 2 times salary is inadequate for most Texas families with a mortgage and dependents. Use it as a supplement, not a foundation. A standalone term policy gives you control, portability, and the right coverage amount.

Use these tips to save on insurance to manage your overall insurance budget without cutting corners on coverage that actually matters.

Take the next step: Protect your Texas family

With a clearer view of insurance coverage and gaps, getting expert help can make all the difference for Texas families.

At Hettler Insurance Agency, we have been helping Texas families build the right protection since 1992. As an independent agency representing over 30 top-rated carriers, we shop the market so you get the best fit at the best price. Whether you need life insurance advice for your loved ones or want to understand the differences between types of mortgage insurance, our team is ready to walk you through every option without pressure.

Ron and Meghan Hettler are both Certified Insurance Counselors (CIC), the gold standard credential in the industry. That means you get expert guidance, not a sales pitch. We also provide Texas homeowners insurance advice tailored to local risks like hail, windstorm, and high property taxes. Call us today or visit hettlerinsurance.com to review your current coverage and close the gaps before they cost your family everything.

Frequently asked questions

Does life insurance cover hurricane or flood damage in Texas?

No, life insurance does not cover property damage from hurricanes or floods. You need a homeowners policy with windstorm coverage and a separate flood insurance policy for those specific property risks.

How much life insurance do I need as a Texas homeowner?

Experts recommend 10 to 15 times your annual income, enough to pay off your mortgage, settle debts, and provide for your dependents over the long term.

What are the main differences between term and whole life insurance?

Term life offers affordable, temporary coverage that matches your mortgage or child-rearing years, while whole life is permanent, costs significantly more, and builds cash value with estate planning advantages.

Is employer group life insurance enough for Texas families?

No. Most employer group policies cover only 1 to 2 times salary, which falls far short of what a family with a mortgage and dependents actually needs. Treat it as a supplement to a standalone policy.

Do stay-at-home parents in Texas need life insurance?

Yes. A stay-at-home parent provides real economic value in childcare and household management, and replacement costs can run $17,000 or more per year per child. That financial gap needs coverage too.

Recommended

About the Author

Ronald J. Hettler, CIC is a Certified Insurance Counselor (CIC) [the gold-standard credential in the independent insurance industry]. Ron has over 46 years of real-world experience in the insurance industry. He is the owner/president of Hettler Insurance Agency in Lubbock, Texas and is licensed by the Texas Department of Insurance (License #666862). (Why Trust Hettler Insurance Agency? It’s a Local independent insurance agency representing multiple carriers. Hettler Insurance Agency has established business roots going back to it’s predecessor in the late 1800’s. Local expertise in Lubbock Texas and West Texas risks. Focused on clarity before a claim occurs.) Ron and his daughter Meghan, also a CIC, lead a team that represents 30+ carriers and serves clients across Texas.

Ron specializes in helping individuals, families, and small business owners understand complex insurance concepts in clear, practical terms so they can make informed decisions about their coverage. He specializes in helping individuals and families understand coverage gaps, deductible structures, and real-world claim outcomes before a loss occurs. Ron helps you to understand how insurance policies respond in real-world claim situations.

License verification available through the Texas Department of Insurance.

Expanded Frequently Asked Questions ?

Q1 ?: Does life insurance cover hurricane or flood damage in Texas?

Q2 ?: How much life insurance do I need as a Texas homeowner?

Q3 ?: What are the main differences between term and whole life insurance?

Q4 ?: Is employer group life insurance enough for Texas families?

Q5 ?: Do stay-at-home parents in Texas need life insurance?

— Life Insurance Instant Quote and Apply Tool @ GetLifePolicy.com > * Quick self-service term life insurance quote. With or without medical exam.

— Call us about Auto, Home, Business, Life, or Health insurance. * Click to Call (806) 798-7800, Mon-Fri 8:30am-5pm (lunch closed Noon-1pm)

— Come see us @ our new address 4720 S Loop 289 Lubbock, TX 79414 (maps link), or get your online quote started at https://GetHettler.com